Last week, Rosenblatt Securities analyst Kenneth Hill suggested the pricing of Paypal Holdings (NASDAQ:PYPL) is more palatable than payments rival Square (NYSE:SQ), and as such makes it the easier name of the two to own. His point was well taken. But, he may be looking past a key argument in owning SQ stock over PayPal shares.

That is, Square is growing much, much faster.

That certainly doesn’t make it a safer play. Indeed, Square stock is undeniably the riskier holding of the two payments middlemen. From a risk-vs-reward perspective, though, there’s a clear place for Square shares in some portfolios.

The rich irony is, the day after Hill made the call, Square reminded the market of why — if forced to choose — investors should choose SQ stock over PayPal.

What He Said

“While both names have a little hair on them after Q2’s update, we see PYPL as a steady and strong grower, all at a reasonable price, forming the basis for our Buy rating,” explained Rosenblatt’s Hill, when simultaneously initiating coverage of both PYPL and SQ stock last week. He added

“the longer-term outlook for the firm looks as healthy as ever.”

And, perhaps it does.

Comparing and contrasting Square and PayPal is a textbook definition comparing apples and oranges. The former is a relative newcomer and should sport a loftier earnings-based valuation. The former is a more mature company, with less potential to penetrate a market it already dominates. PYPL stock shouldn’t command the same kinds of valuations.

It’s a reality most investors have admittedly lost sight of over the course of the past 12 months. SQ stock is down 18% since August of 2018, while PayPal has advanced more than 20%. A couple of different quarterly shortfalls proved problematic.

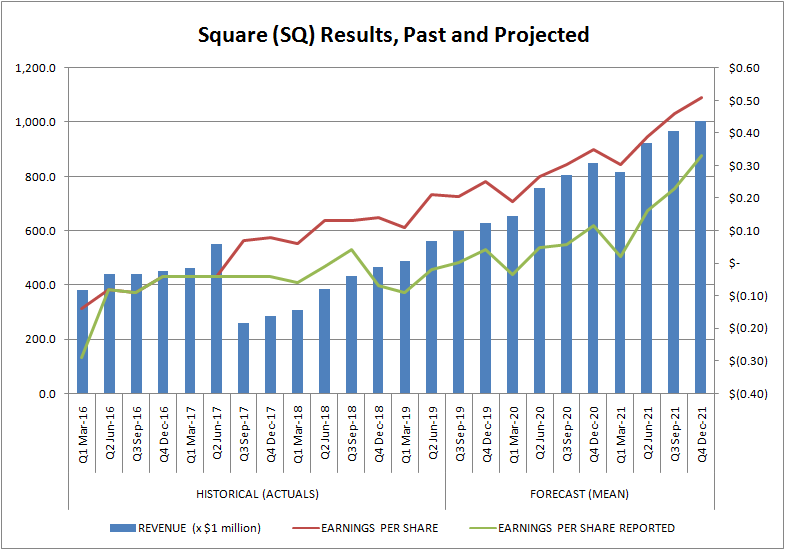

Take a closer look though. It’s the expectations that may have been unreasonable, to the point of being unfair. Square hasn’t failed to produces revenue growth of at least 30% in any quarter in more than two years. That’s a pace most other companies would envy.

Click to Enlarge

It’s also still booking GAAP losses, but those losses are shrinking rapidly. Real net income is in sight. By 2021, Square is expected to be producing real, GAAP profits.

And that’s the boat Rosenblatt’s Hill may be about to miss.

It’s All Relative

Hill said Square is trading at about 56 times his 2020 (operating) EPS projection, implying expected profits on the order of $1.12 per share. That’s in line with the consensus for next year.

Square is still a story stock, though. It’s not about the absolute valuation. It’s about the relative valuation, or more specifically, the earnings trajectory. That’s where SQ stock truly starts to shine, and justify its rich price. Next year’s likely $1.12 per share of non-GAAP earnings? That’s 45% better than this year’s projected 77 cents, which is 64% better than last year’s 47 cents per share.

PayPal is only growing its bottom line at about half that pace.

Clearly there’s no guarantee the market will continue to give Square a pass on the valuation front, just as there’s no guarantee it will be able to report the 2020 numbers analysts are collectively modeling.

On the other hand, given that July’s downloads of Square’s Cash App once again broke records, it’s clear Square is doing something right. Indeed, Instinet analyst Dan Dolev reports that Square’s payment app continues to spur more downloads than PayPal’s equivalent app, despite PayPal’s dominating lead in the payment space.

Maybe it’s not so dominant after all.

Bottom Line for Square Stock

Don’t misread the message. Square stock may hold more potential for reward, but that comes packed with more risk. PayPal is a known quantity, making it relatively easy to handicap. Square is the newcomer. Consumers love it, but it’s a work in progress.

The current valuation of SQ stock, however, reflects the balance of that risk and reward. And, at a frothy-but-not-outrageous 56x next year’s likely earnings for a company growing the top and bottom line between 40% and 60% in any given quarter, its recent weakness has priced Square stock fairly.

While it’s obviously not a name for grandma’s retirement portfolio, neither it is a name that must be avoided at all costs.

Ironically, it could be a name to own side by side with PayPal in a portfolio, serving as a double-barreled bet on the inevitable growth of the digital payments business.

As of this writing, James Brumley did not hold a position in any of the aforementioned securities. You can learn more about him at his website jamesbrumley.com, or follow him on Twitter, at @jbrumley.