Delta (NYSE:DAL) stock has been on a roller-coaster ride over the past few months thanks to the novel coronavirus pandemic sending unprecedented shock-waves across the global air travel industry.

First, DAL stock tanked from $60 to below $20 on the idea that the pandemic was going to depress global air traffic for a long time. Then, DAL stock rebounded with vigor to nearly $40, as the U.S. economy reopened and air traffic trends meaningfully improved in May. Then, the stock gave back a big chunk of those gains, and dropped back below $30, as a second wave of Covid-19 has started to emerge across various states in the U.S.

After all that volatility, what comes next for Delta stock?

Some choppiness over the next weeks, followed by another leg higher in the stock, mostly because of near-term fears regarding a second wave, which are slightly overstated.

However, they will pass.

When they do, air traffic trends will continue to improve. Delta’s numbers will continue to get better. And DAL stock will continue to recover.

As such, I say purchase the June dip in DAL stock. Today’s second wave fears won’t derail the economic recovery. So long as they don’t, Delta stock will get back into recovery mode soon.

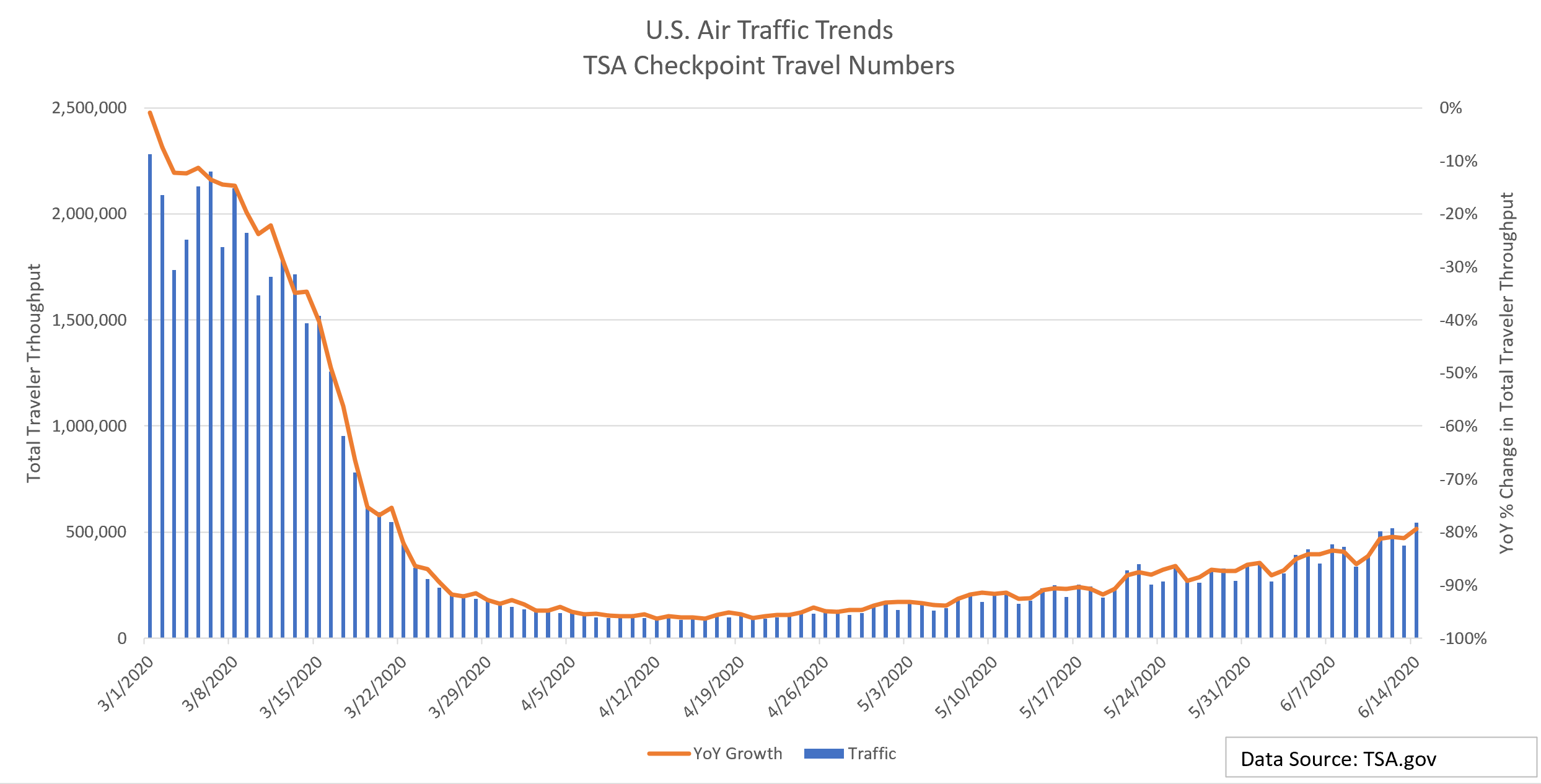

Air Traffic Trends Are Improving

Over the past few months, U.S. air traffic trends have meaningfully improved, and this improvement will persist for the foreseeable future.

That is, from its mid-April lows to today, TSA recorded total traveler throughput at airports has risen more than 500%. Sure, total traveler throughput is still down 79% year-over-year as of mid-June. But that’s up from 90%+ declines throughout April and May, and represents the first time that the year-over-year decline has been less than 80% since March 21.

Click to Enlarge

In other words, Americans are starting to fly again.

The big risk, of course, is that the emergence of a second wave kills this recovery.

But it won’t. We’ve learned a lot about this virus since March. The more we’ve learned, the more we’ve discovered that the fatality rate of Covid-19 isn’t all that high, and actually not too far off from the seasonal flu’s death rate

. As the science has shifted from “it’s the Black Plague” to “it’s like the flu on steroids”, consumer behavior has shifted too, from, “we should stay inside at all costs” to “we can live our regular lives, with certain restrictions, to appropriately manage risks”.

Naturally, this consumer behavior shift lays the groundwork for travel resumption. According to a recent Overseas Leisure Group survey, about three-fourths of Americans are already planning their next vacation.

As such, a second wave won’t derail the airline industry’s recovery. Sure, it may slow the recovery to an extent. But, between now and the end of the year, air traffic trends will significantly improve.

As they do, DAL stock will roar higher.

Delta Stock Is Too Cheap

By my numbers, Delta stock is simply too cheap to ignore here.

Yes, I understand that the company’s profit margins will never be as high as they were in 2019 because the airline operator is going to have to spend an arm and a leg on routine, intensive cleaning. I also understand that the company’s share repurchase program will be significantly limited, taking away a huge driver of earnings per share growth for this company.

Still, even after considering those things, DAL stock is just too cheap here and now.

My base case is for Delta’s revenues to get wiped out in 2020, recover strongly in 2021, and return to 2019 levels by 2022. That would imply $47 billion in 2022 sales. Pre-tax profit margins will similarly get killed in 2020, recover strongly in 2021, and hit steady state levels by 2022, with those steady state levels being below 2019 levels. In 2019, pre-tax profit margins were north of 13%. I see them hovering around 10% going forward.

Assuming so, you’re talking about $4.7 billion in pre-tax profits in 2022. Taking out 23% for taxes and assuming a 630 million diluted share count (roughly equivalent to today’s share count), that equates to about $5.75 in earnings per share. Based on a historically-normal 8-times forward earnings multiple, that implies a 2021 price target for DAL stock of over $45.

Shares trade hands below $30 today.

Bottom Line on DAL Stock

So long as air traffic trends continue to improve and fully recover by 2022, Delta stock is significantly undervalued here, even after factoring in the reality that profit margins will be permanently depressed and buybacks are a thing of the past.

As such, if — like me — you believe that consumers are ready to travel again, then buying DAL stock on June weakness related to “second wave” fears is the smart move.

Luke Lango is a Markets Analyst for InvestorPlace. He has been professionally analyzing stocks for several years, previously working at various hedge funds and currently running his own investment fund in San Diego. A Caltech graduate, Luke has consistently been rated one of the world’s top stock pickers by various other analysts and platforms, and has developed a reputation for leveraging his technology background to identify growth stocks that deliver outstanding returns. Luke is also the founder of Fantastic, a social discovery company backed by an LA-based internet venture firm. As of this writing, he did not hold a position in any of the aforementioned securities.