Paysafe (NYSE:PSFE) begins trading on the New York Stock Exchange on March 31 as its SPAC merger with Foley Transimene Acquisition Corp II (BFT) was set to close on Mar. 30. I believe that PSFE stock is worth between $19.46 and $23.53 based on my assessment of its value using comp analysis. This represents potential gains of 30% to 57% from the March 29 price at $15 per share.

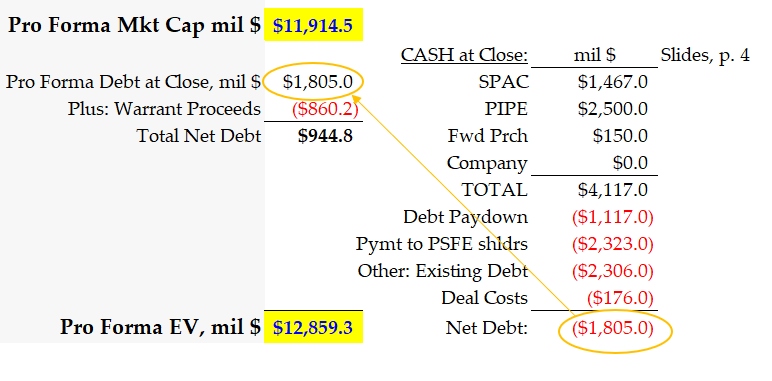

Most of my analysis of PSFE stock’s value is based on the company’s updated slide presentation, which is on their IR website. This helps me see that at $15 the company will have a pro forma market capitalization of $11.9 billion.

Keep in mind that I am including with this market cap the 74.8 million warrants which are presently in-the-money, as their exercise price is $11.50. This is well below the $15 market price so I assume they will be exercised.

Click to Enlarge

Next, I include the warrant proceeds ($860 million) in the calculation of the company’s enterprise value (EV). You can see this calculation in the table at the right.

Note that I calculate that Paysafe stock will actually end up with net debt (after cash proceeds) of about $944 million. This must be added to the market cap to end up with the EV calculation.

What Paysafe Is Worth

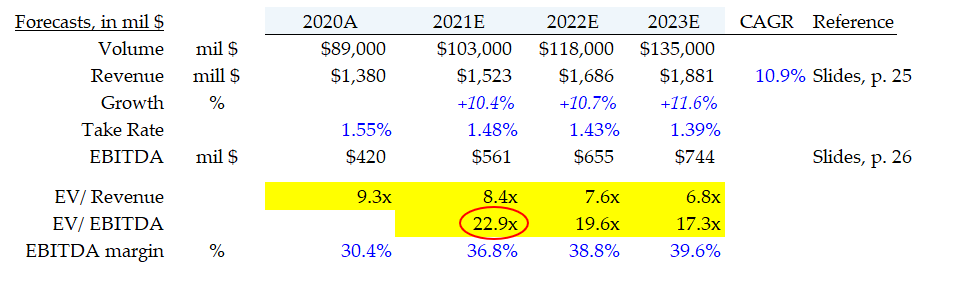

Fortunately, Paysafe allows us to see their own internal projections for several key financial items. For example, they project out their transaction volume, revenue and adjusted EBITDA (earnings before interest, taxes, depreciation, and amortization) over the next several years.

Click to Enlarge

These can be seen on the presentation pages 25 and 26. The table above shows these forecasts and our analysis.

The table shows our calculations of Paysafe’s take rate, its EV-to-sales multiple, EV-to-EBITDA ratio and its EBITDA margins. These will be useful when we compare Paysafe’s performance forecast with its comparable peers.

Notice that Paysafe has a very high EBITDA margin of around 37%. Compare this to PayPal, which has a 19% EBITDA margin. I wrote about this in my earlier article on Paysafe. Note also that Paysafe has a 1.48% take rate (i.e., the amount of revenue it makes from total transaction volume). This is actually somewhat lower than PayPal, which is closer to 2.0%.

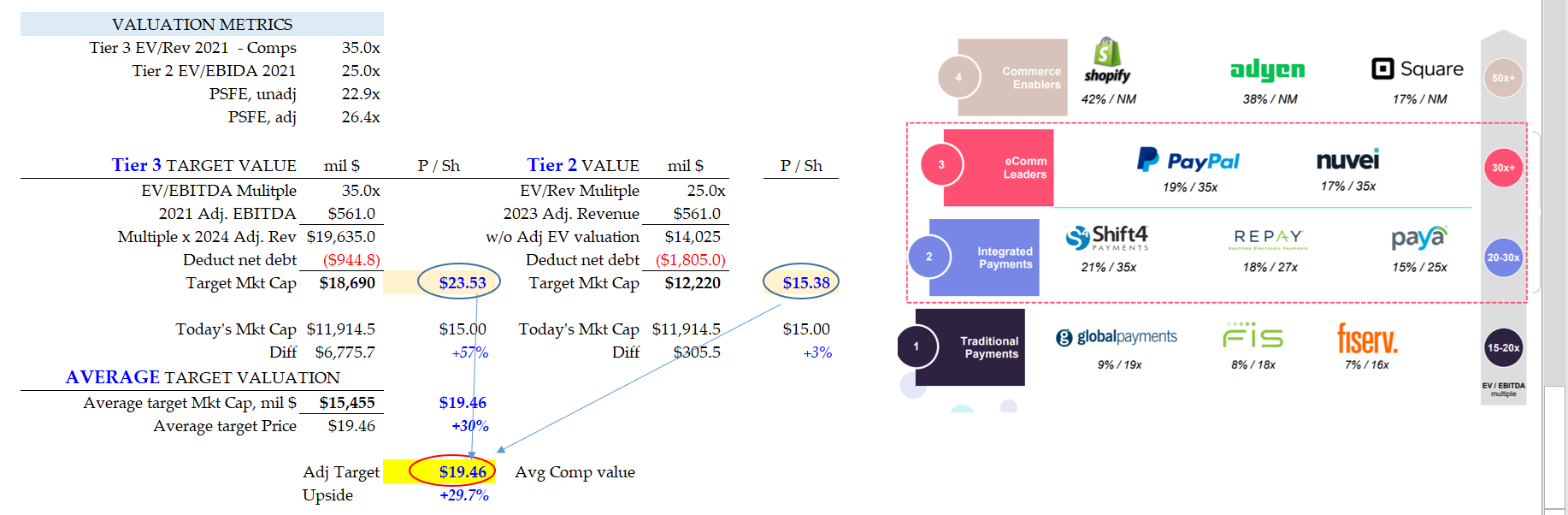

Nevertheless, on page 32 of the Paysafe slide deck

, we see some comp valuations of its peers. For example, PayPal (NASDAQ:PYPL) trades at 35 times EV-to-EBITDA. This is much higher than Paysafe’s 23 EV-to-EBITDA multiple at $15 per share. Another similar company Nuvei Corp. (OTCMKTS:NUVCF) has an equally high 35 times EV-to-EBITDA multiple. This implies that PSFE stock is worth a good deal more.

You can see this in the valuation table I have put together along with slide 32 of the Paysafe deck below.

Click to Enlarge

Using tier 3 of the slide deck, PSFE stock has an implied target value of $23.53 per share. This uses the 35 EV-to-EBITDA multiple and then deducts the net debt to derive the equity value.

Tier 2 from the table uses an average of 25 times EV-to-EBITDA multiple. The implied equity value is $15.38 per share.

An average of both tiers shows that the average target price is $19.46, or about 30% above today’s price.

What to Do With PSFE Stock

You can see that PSFE stock is worth somewhere between its average of $19.46 (+30%) and the tier 2 value of $23.53 (+57%).

I suspect that once Paysafe is trading on its own after the SPAC merger has closed, more analysts will begin covering the stock. They will likely point out these same value discrepancies as I have. That will act as a catalyst for the stock to reach its target values.

Therefore, now might be a good time for value-oriented investors to take a position in PSFE stock.

On the date of publication, Mark R. Hake did not hold a long or short position in any of the securities in this article.

Mark Hake writes about personal finance on mrhake.medium.com and runs the Total Yield Value Guide which you can review here.