Impressively, BlackRock (NYSE:BLK) was founded in 1988 in New York. So, this iconic company is likely younger than many people reading this article. However, impressively, BlackRock’s total assets under management crossed $10 trillion back in 2021. This number has stayed relatively stable since. But this sort of growth has caused many to envision BlackRock as some sort of enigmatic entity that controls everything.

That’s generally a far-fetched view of the company, but I do think BlackRock’s buying activity is important for other reasons. For retail investors, it may be worth considering which stocks this company is buying. Doing so may allow certain investors to replicate parts of BlackRock’s broader investing strategy.

Larger institutional investors tend to have a significant resource advantage, and BlackRock has certainly advanced this idea. The company has been behind many notable changes in the stock market, such as ESG investing. As such, following in BlackRock’s footsteps could lead to outsized gains relative to those investing in passive index funds, if you believe the institutional money manager’s process works.

Here are seven growth stocks to consider I think fits the bill. That’s because each of these seven companies are ones Blackrock bought more of in the first quarter.

Microsoft (MSFT)

Microsoft (NASDAQ:MSFT) doesn’t really need an introduction. I believe Microsoft’s strong Q3 results highlight why it remains one of the most compelling long-term investments in the tech sector, if not the best. The company reported record revenue of $61.86 billion this past quarter, up an impressive 17% year-over-year. These results were driven by the continued strength of its Microsoft Cloud platform, which surpassed $35 billion in sales.

Microsoft is firing on all cylinders. Its Azure cloud infrastructure is taking market share, and the company is making significant strides in advancing the artificial intelligence revolution via partnerships with OpenAI and others.

The white-collar sector already can’t get enough of Microsoft’s productivity products, and with Microsoft Copilot adding more appeal, I expect these AI tailwinds to further propel Microsoft’s growth. While the stock isn’t cheap at 32-times forward earnings, Microsoft’s indispensable role in the global economy and its fortress-like competitive advantages make it a core holding for any growth portfolio. It’s no surprise that BlackRock is betting big on Microsoft’s long-term potential.

Confluent (CFLT)

Confluent (NASDAQ:CFLT) provides a data streaming platform based on Apache Kafka. The company is riding powerful secular growth tailwinds in the real-time data processing, cloud adoption, and digital transformation areas of the economy, which should continue to see strong demand for years to come. While currently unprofitable, Confluent’s Q1 results show investors that this is a company that’s rapidly moving towards sustained profitability.

Confluent reported 25% revenue growth this past quarter, or a top line number of $217 million. This number beat estimates, with the company’s high-growth Confluent Cloud product now comprising the majority of its sales. Analysts now expect around 20%-25% top-line growth to continue for the foreseeable future. Importantly, Confluent also posted an impressive improvement in its operating margins to 22%, the fourth straight quarter of such gains. Analysts expect full-year 2024 profitability with accelerating earnings growth ahead.

With elite institutions like BlackRock buying the stock, Confluent appears well-positioned to emerge as one of the most dominant software players of this decade. This positioning has many analysts seeing juicy upside for CFLT stock.

Click to Enlarge

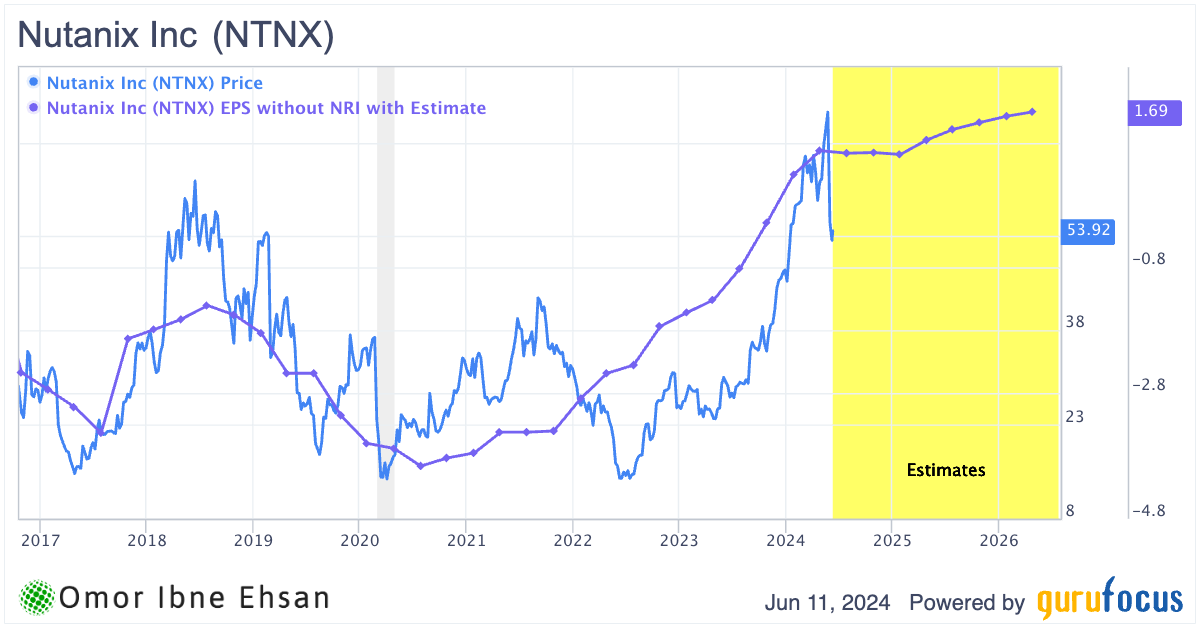

Nutanix (NTNX)

Nutanix (NASDAQ:NTNX) provides cloud computing software for businesses to manage their data centers and IT infrastructure. The company is also riding several powerful mega trends that could propel the stock significantly higher in the years ahead. In its latest quarter, Nutanix grew revenue 16.9% year-over-year to $525 million, while annual recurring revenue (ARR) surged 24% to $1.82 billion. Management highlighted steady demand as organizations prioritize digital transformation and infrastructure modernization to optimize costs. I’m of the view NTNX stock is owns that should recover alongside its improving earnings per share numbers.

Click to Enlarge

Recently, Nutanix scored a major win with a Fortune 50 financials company looking to automate its database deployment using Nutanix’s cloud platform. Another Fortune 500 consumer goods provider decided to standardize its back-end on Nutanix’s software stack and swap out a competitor’s footprint.

I believe Nutanix’s best-in-class platform positions the company at the center of the hybrid multi-cloud and data center automation revolutions. With shares already up 81.5% over the past year, I wouldn’t be surprised to see this momentum continue as more large enterprises turn to Nutanix to maximize their IT efficiency in this digital age.

Pure Storage (PSTG)

Notice a trend here? I definitely do. Blackrock is betting massively on data center companies. Pure Storage (NYSE:PSTG) provides data storage hardware and software solutions. The company is also among those on this list that delivered strong Q1 results, with revenue growing 17.7% year-over-year to $693 million, beating estimates by $13 million. Pure Storage is seeing early success in capturing AI-related opportunities across high-performance computing, enterprise inference engines and upgrading enterprise storage to eliminate data silos. I believe the hyper-growth upside AI provides is a major tailwind that could propel PSTG stock much higher. And notably, subscriptions have been driving most of the growth here:

Click to Enlarge

The company’s management team recently highlighted a key platform win with a managed service provider specializing in AI infrastructure, demonstrating Pure Storage’s differentiated offerings. The company’s unified Purity platform simplifies data management across on-premises and cloud environments, which is crucial for enterprises looking to use AI. As more companies jump aboard, and the company continues to diversify its client base, investors stand to benefit from increased cash flow stability.

With PSTG shares already up 83% over the past year, some may think this rally may be overdone. However, I think this is a stock that could see its momentum continue, as long as the company sustains its robust growth trajectory.

Amazon (AMZN)

Amazon (NASDAQ:AMZN) dominates the high-growth e-commerce and cloud computing sectors. I believe this tech titan is morphing into an AI and data powerhouse, resulting in a stock that continues to make new highs. In Q1, Amazon delivered an impressive 13% revenue growth (ex-FX) to $143.3 billion. The company’s operating income also skyrocketed 221% to $15.3 billion, as Amazon’s efficiency efforts are clearly paying off.

In the world of mega-cap cloud players, AWS remains the undisputed leader. Amazon Cloud Services now provide the lion’s share of Amazon’s profits. And with generative AI tools already used by over 100,000 sellers, Amazon is harnessing cutting-edge tech to enhance its ecosystem.

I expect key tailwinds like the continued shift to online shopping, AWS’s dominance, and emerging AI innovations to provide long-term capital appreciation to patient investors. While consumers are cautious (trading down in this uncertain economy), Amazon’s everyday low prices and ultra-fast delivery are clearly resonating with a loyal clientele.

As long as the macro picture improves (or at least cooperates), I believe Amazon will command a premium valuation – maybe even a higher multiple. In my view, this is an evergreen stock to buy and hold long-term.

Pinterest (PINS)

Pinterest (NYSE:PINS) operates a visual discovery engine for finding ideas like recipes, home and style inspiration, and more. While some may consider Pinterest a fading social media platform, the company’s latest results paint a different picture. In Q1, Pinterest achieved its highest user and revenue growth since 2021, with global monthly active users (MAUs) surpassing 500 million for the first time. Specifically, this metric grew to 518 million monthly users, up 12% year-over-year. Revenue also impressed, growing 23% to $740 million, nearly doubling the growth rate from the previous quarter.

I believe several mega trends could propel Pinterest higher in the coming years. The continued shift to digital advertising plays to Pinterest’s strengths, as its visual format and user intent make it an attractive platform for brands. The company’s focus on AI-driven improvements to content relevance and curation is deepening user engagement. And with Pinterest’s earnings per share and revenue expected to double over the next five years, Pinterest’s growth story seems far from over.

While primarily popular with women, Pinterest’s expanding user base and reaccelerating ad revenue suggest it may be an under-appreciated growth opportunity that’s just hitting its stride. BlackRock is in, and I am too.

Healthpeak Properties (DOC)

Healthpeak Properties (NYSE:DOC) is a healthcare REIT that owns and develops real estate serving the healthcare industry. While the stock has struggled to regain its 2013 peak, I believe there are compelling reasons BlackRock is still interested in this company. In Q1, Healthpeak delivered revenue of $600.81 million, beating estimates and translating into impressive 15.65% year-over-year growth. Management also raised full-year 2024 earnings guidance by 2 cents at its midpoint.

Healthpeak’s recent merger seems to be a major positive catalyst, with the integration exceeding expectations. Healthpeak has already successfully internalized its property management business, acquiring 17 million square feet of profitable real estate to add to its growing portfolio. With plans to pursue additional deals, I believe significant growth is certainly possible from here. Over the next year, the company’s EBIT should inflect higher, pushing DOC stock up.

Click to Enlarge

And while investors wait for DOC stock to recover, Healthpeak’s 6.2% dividend yield should provide more than enough incentive to keep holding. I don’t think this is a real estate company that’s posted to slash its dividend anytime soon, as the company’s payout ratio and dividend yield metrics are reasonable (and have stabilized quite a bit).

Click to Enlarge

Analysts also expect robust 22.4% sales growth this year and 5%-plus annual earnings per share growth starting next year. Along with the other names on this list, I can see why BlackRock likes this name.

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.