The market rally so far has been what anyone would have expected just a year back. I wouldn’t be surprised if it drags on and, the S&P 500 crosses 6,000 points, and the Nasdaq goes above 20,000 by the end of the year. However, as everyone knows, most of these gains have been due to a select few companies at the top that are reaching euphoric levels while overshadowing commonly undervalued stocks.

For example, Nvidia (NASDAQ:NVDA) became the world’s largest company by market cap for a moment. It has come down again, but I think it could regain the crown again if the rally continues.

On the other hand, many undervalued stocks have been given the bad end of the stick by Wall Street. They’ve been languishing at bargain-basement levels, and investors have ditched them to put their money where the action is. I think that makes it the best time to go bargain hunting. Many of these companies are household names with solid profitability and should bounce back once the market cycle takes a turn again. Their downside risk is also pretty low. You’d definitely want a pie of at least some of these undervalued stocks if you wish to hold for the next couple of years:

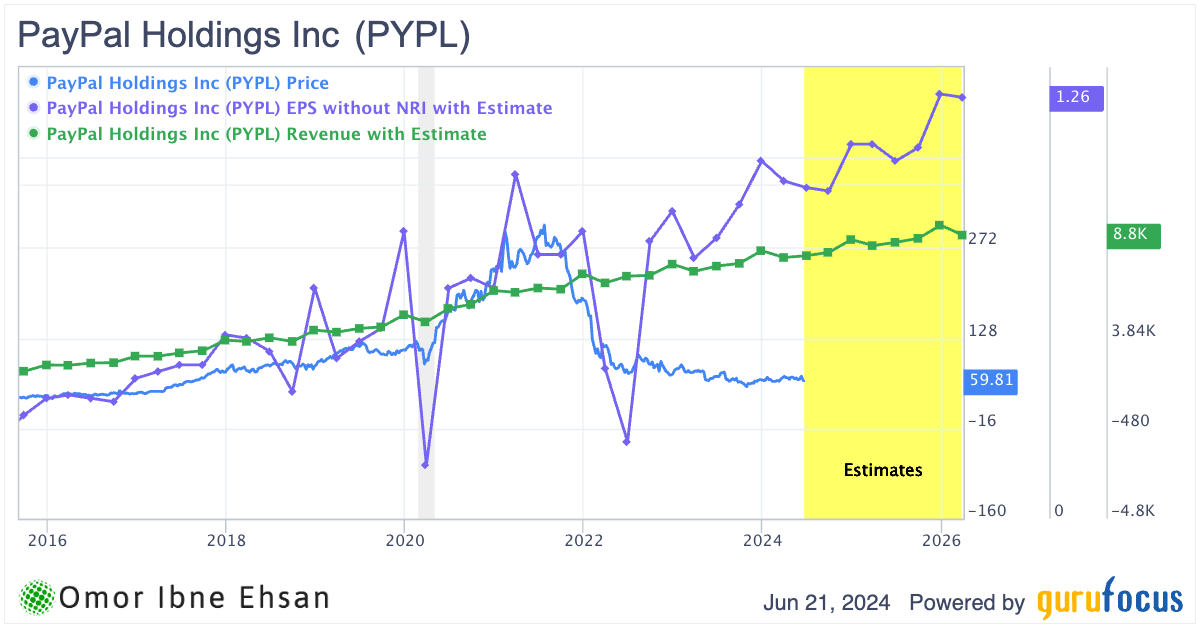

PayPal (PYPL)

PayPal (NASDAQ:PYPL) is a leading digital payment platform that enables online money transfers and purchases. The fintech sector has been battered in recent years, but I believe PayPal is poised for a major breakout. In Q1 2024, the company delivered solid 10% currency-neutral revenue growth on $404 billion in total payment volume, with transaction margin dollars growing 4% better than expected. Non-GAAP EPS surged an impressive 27% year-over-year.

Despite maintaining 8%+ annual revenue growth and low double-digit EPS growth set to accelerate to around 20% in coming years, PayPal trades at a ridiculously cheap 51% discount to its February 2020 peak. The stock is trading at a fraction of its historical earnings and sales premium.

Click to Enlarge

While user growth remains a Wall Street concern, it has turned positive on a quarterly basis. Meanwhile, PayPal has evolved into a cash cow, executing $5 billion in buybacks last year with plans for another $5 billion in 2024. It is one of the most undervalued stocks right now, and I think most analysts would agree with me.

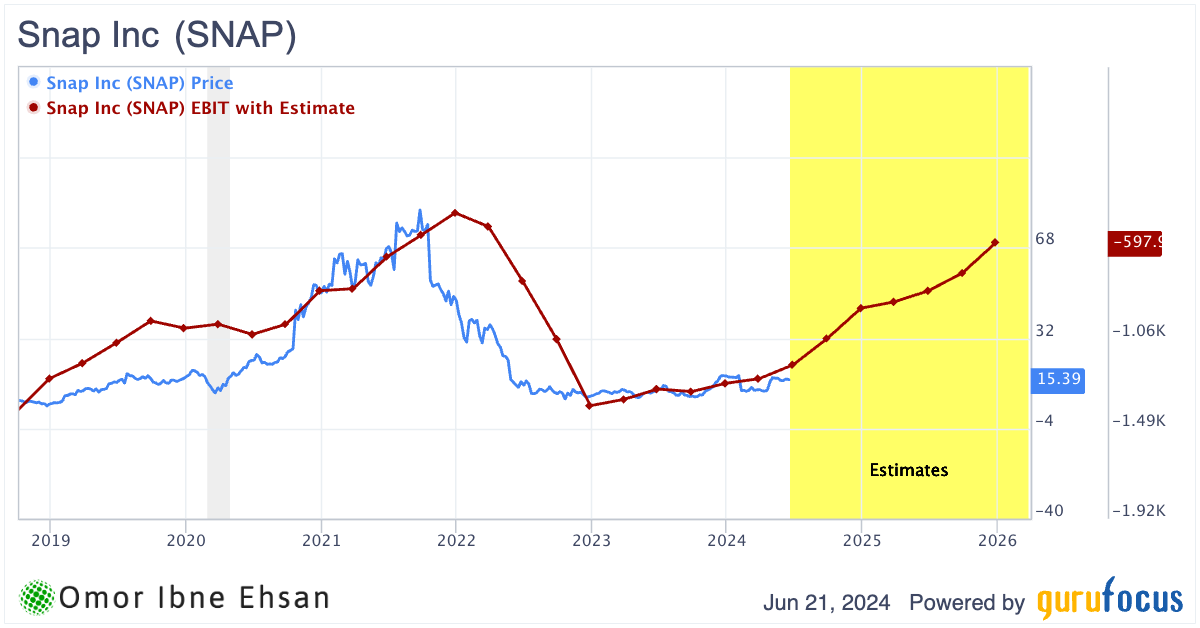

Snapchat (SNAP)

Snap Inc. (NYSE:SNAP) operates the Snapchat social media platform. The company’s Q1 results show promising signs that this beaten-down stock could be on the cusp of a major recovery. I was pounding the table on social media stocks like Meta (NASDAQ:META) back when it was trading below $100 less than two years ago. It now trades at $500-plus as of writing. I believe Snap could follow a similar trajectory, especially if a TikTok ban occurs in the U.S.

Snap’s revenue growth accelerated to an impressive 21% YOY, a significant improvement from the prior quarter’s 5% growth rate. The company also reached 422 million daily active users, up 10% from a year ago, as it continues to deepen engagement. Importantly, Snap has a huge advantage with the coveted Gen-Z demographic, reaching over 75% of 13 to 34-year-olds in more than 25 countries. EBIT is also expected to rise significantly from these tailwinds.

Click to Enlarge

If TikTok does shut down, I expect Snapchat to be a prime beneficiary as young users flock to familiar alternatives. While Snap’s ARPU has been lackluster, I anticipate this key metric will inflect higher going forward as ad demand improves and the company refines its advertising platform. With strong operating leverage, even modest ARPU gains could drive explosive profit growth.

The pieces are in place for Snap to potentially deliver a triple-digit return for investors willing to ride out the near-term volatility.

Six Flags Entertainment (SIX)

Six Flags Entertainment (NYSE:SIX) operates regional theme parks across North America. I believe this stock is significantly undervalued and poised for a major recovery in the coming years. Like many travel and leisure companies, Six Flags was forced to take on substantial debt to survive the pandemic, which has weighed heavily on its earnings due to the high 6.57% annualized interest rate.

However, several key indicators give me confidence that Six Flags is on the cusp of a resurgence. Pass sales remain strong, with both units and average pass prices showing solid double-digit increases over last year. Group sales are also outperforming expectations, surpassing last year’s numbers by over 20% and approaching pre-pandemic levels. Additionally, in-park spending continues to grow, with a 5% increase in spending per capita.

As interest rates eventually come down, I expect Six Flags’ earnings potential to be unleashed. The company’s focus on premiumization and reinventing the customer journey through digital transformation should drive profitable growth. With the stock remaining depressed, I believe now is an opportune time to invest before the market recognizes Six Flags’ cash cow potential. I wouldn’t be surprised to see EPS comfortably double within the next three to four years.

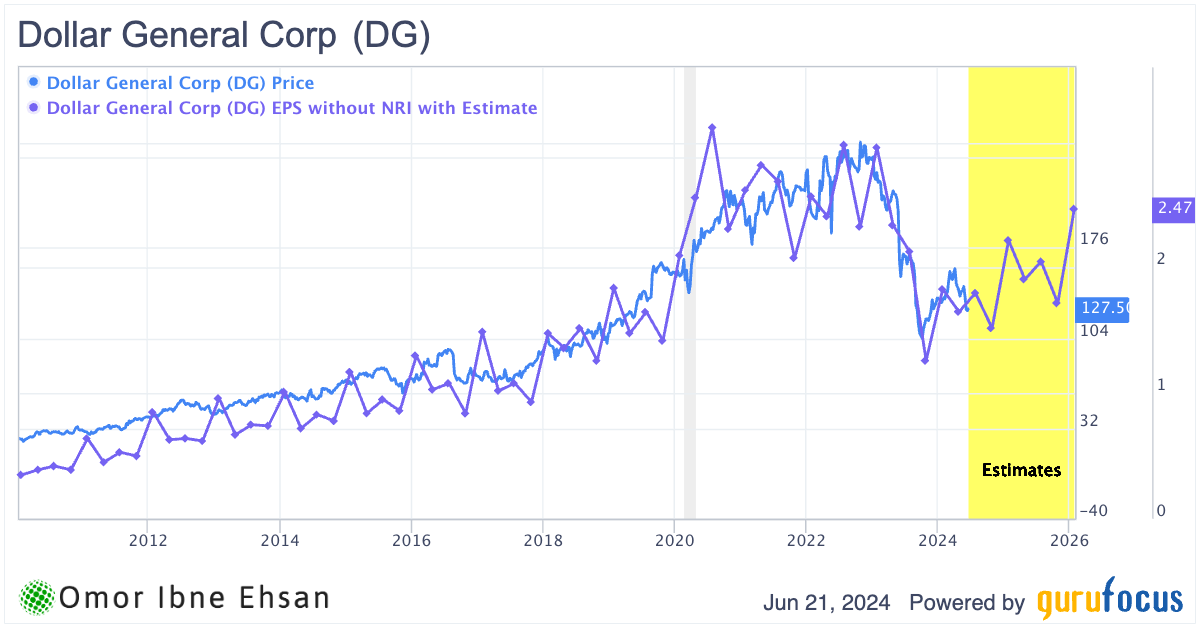

Dollar General (DG)

Dollar General (NYSE:DG) operates a chain of discount retail stores across the United States. Despite delivering solid Q1 results that beat expectations on both the top and bottom lines, DG stock has been unable to stage a sustained recovery amid the broader retail sector’s ongoing struggles. I believe the biggest culprit holding back DG shares is the persistently high interest rate environment, which continues to weigh on consumer spending and sentiment.

However, when I look at Dollar General’s long-term positioning, I see a company that is poised to benefit from some of the most powerful megatrends reshaping the retail landscape. Dollar General is uniquely positioned to capitalize on the growing demand for affordable shopping, especially in rural areas.

Furthermore, as consumers increasingly prioritize value in economic uncertainty, I believe Dollar General’s business model will prove more resilient than many of its peers. I think now is an excellent time for patient investors to scoop up DG shares before the inevitable recovery takes hold. Profitable, well-established household names like Dollar General rarely disappoint in the long run.

Click to Enlarge

I expect EPS growth to drive the stock toward the $200 level by early 2026.

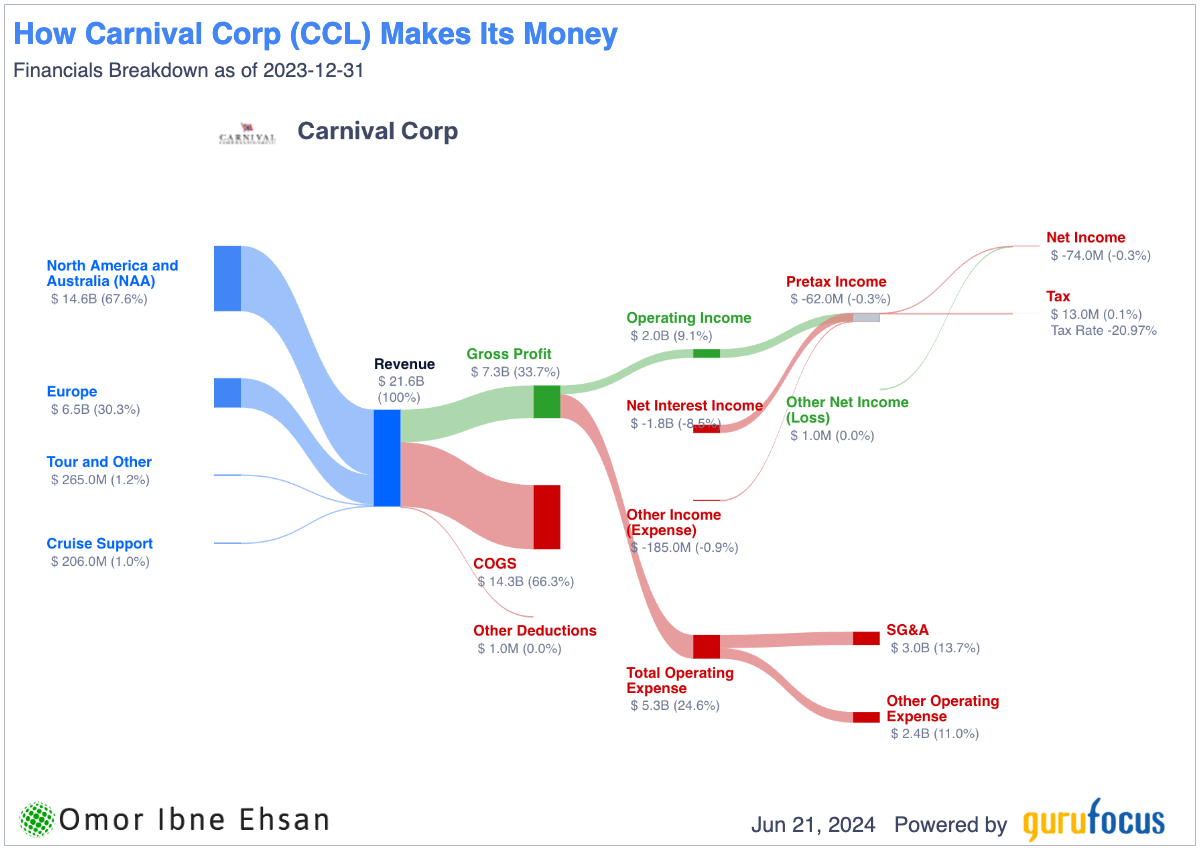

Carnival (CCL)

Carnival (NYSE:CCL) operates the world’s largest cruise line. I believe Carnival stock will have a major recovery in the coming years. The company reported record revenues, bookings, and customer deposits in Q1 2024, with yields increasing over 17% YOY. Carnival is seeing strong demand and pricing across all core markets and quarters.

Management highlighted that they are capturing more new guests than ever, in addition to their growing base of repeat cruisers. This broad-based demand should drive sustainable revenue growth. At the same time, Carnival has prepaid significant debt, which will reduce its interest expense burden going forward. Rate cuts should help significantly since interest expenses ate away 90% of operating income last year.

Click to Enlarge

I see powerful demographic tailwinds at Carnival’s back. The growing population of retirees in Florida and other coastal states represents a huge addressable market for cruising. As these headwinds converge with Carnival’s strengthening fundamentals, I believe the stock offers a rare opportunity for triple-digit gains in the years ahead. For long-term investors, Carnival looks like a once-in-a-generation buying opportunity at these still-depressed levels.

United Airlines (UAL)

United Airlines (NASDAQ:UAL) is a major U.S. airline providing air transportation services. The company could soar as the travel industry recovers, buoyed by strong pent-up demand and the easing of pandemic restrictions. United’s Q1 results show the resilience of its United Next strategy, with the airline delivering meaningful YOY margin improvement despite facing significant aircraft delivery delays from Boeing (NYSE:BA). United ended up asking some pilots to take unpaid leave, often for months!

Management stated they would have been profitable for the quarter if not for the Boeing MAX 9 groundings. Plus, United is seeing positive booking momentum across all customer segments. While the Boeing delays are driving temporarily higher costs this year, United’s adept cost management is helping offset most of those headwinds.

It is targeting a full-year EPS target of $9 to $11. Thus, I believe the stock trades undervalued at these levels. As United pays down debt and capitalizes on the travel resurgence, I expect the stock to make a strong comeback in the coming years.

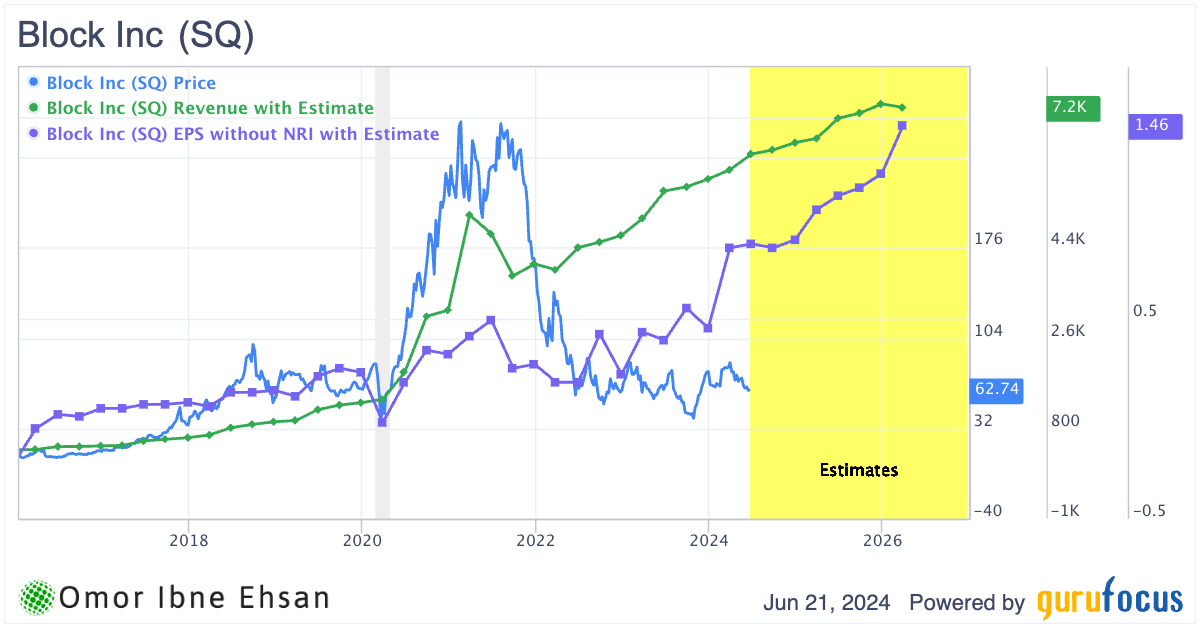

Block (SQ)

Block (NYSE:SQ) provides mobile payment solutions and financial services for businesses and consumers. The company has faced challenges along with the broader fintech sector, but I believe it now stands poised for a resurgence that could propel its stock to triple-digit gains beyond other undervalued stocks.

In Q1 2024, Block delivered impressive results with EPS of 84 cents, beating estimates by 12 cents, and revenue growing 19.38% year-over-year to $5.96 billion, surpassing expectations by $138 million.

While Block was previously unprofitable like many high-growth fintechs, it has pivoted profitability. The company is now expanding margins, with analysts projecting EPS to double over the next four years, complemented by robust 12% annual revenue growth.

Click to Enlarge

I believe it remains among significantly undervalued stocks relative to its long-term earnings power. If the company executes on these growth projections, shares are unlikely to remain muted for long.

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.