AI Is Lighting a Fire Under the Company We Should Start Calling “Big Green”

I’m optimistic about the company’s potential for further upward movement.

By

Eric Fry, Editor, Fry's Investment Report

Apr 4, 2024, 3:30 pm EDT

Source: Laborant / Shutterstock.com

Hello, Reader.

“Big Blue” has been the nickname for International Business Machines Corp. (IBM) since the 1980s. The sobriquet might have come from the blue tint on the company’s early computer displays. It could very well also be from IBM’s deep blue logo.

Either way, it might be time for a nickname update, as “Big Blue” is rapidly becoming “Big Green.” The stock has jumped 50% since I recommended it to the subscribers of Fry’s Investment Report one year ago. That performance is well ahead of the 30% gain the S&P 500 delivered over the same timeframe.

According to IBM CEO Arvind Krishna, the stock’s outperformance can be indirectly attributed to the company’s recent workforce changes – especially as it makes strides in artificial intelligence automation. As it is, the 112-year-old tech company has substantially reduced roles this year to free up resources for further AI advancements.

This shift not only redefines IBM’s internal structure, but also signals a broader impact on the business landscape.

I’m optimistic about the company’s potential for further upward movement. So, in today’s Smart Money, let’s dive into how IBM is becoming “Big Green.”

And we’ll consider whether the company a good “Buy” ahead of its upcoming earnings report…

What’s Bringing in the Green

The company is set to release its first-quarter earnings report for fiscal year 2024 in two weeks. The analyst community expects earnings of $1.59 per share and revenue of $14.6 billion.

These estimates come on the heels of the exceptionally strong fourth quarter and full-year earnings that IBM reported in January. Here’s what’s bringing in the green…

IBM’s software and consulting offerings are attracting strong demand. Both parts of the business appear to be fueling the other, as enterprises rush to implement AI solutions across increasingly complex computing architectures.

In effect, IBM’s consulting operations are like Best Buy’s “Geek Squad.”

Those Geek Squads can do everything from educating customers to repairing laptops to coming to your home to install and connect “smart devices” like TVs, PCs, and/or cameras. The Geek Squad provides as much, or as little, technological assistance as each customer desires.

IBM Consulting operates in a similar way. Because of this worldwide capability, IBM is ideally equipped to help businesses and other enterprises transition to a complex “multimodal” AI world.

As CEO Krishna stated on the company’s fourth-quarter earnings call…

We believe AI will be multimodal, with our clients leveraging a combination of models – IBM’s, open-source, their own proprietary models, and those of other companies. Flexibility of deployment is key. Simply put, we meet clients where they are and allow clients to deploy AI models across multiple environments…

[Therefore], we continue to believe our Consulting business will be an early beneficiary of AI. We are the only provider today that offers both the [AI] technology stack with our WatsonX platform, and consulting services for deploying and managing generative AI. The early work for clients around data architecture, security and governance is critical and hard, and we think consulting expertise is going to be crucial here…

We are the only technology company with a consulting business at scale. This unique integrated value proposition helps our clients implement digital transformations and generative AI solutions.

Importantly, the cloud businesses of Amazon.com Inc. (AMZN) and Microsoft Corp. (MSFT) are providing about 40% of IBM’s consulting business, and that percentage is growing rapidly. Therefore, IBM stands to benefit directly from the ongoing growth of Amazon’s AWS and Microsoft’s Azure.

Thanks to IBM’s rapidly growing software and consulting offerings, those two divisions now account for 75% of IBM’s revenue base – up from about 55% in 2020.

Significant Upside Potential

I recommended IBM in April 2023 to my Fry’s Investment Reportsubscribers. In my recommendation, I wrote the following…

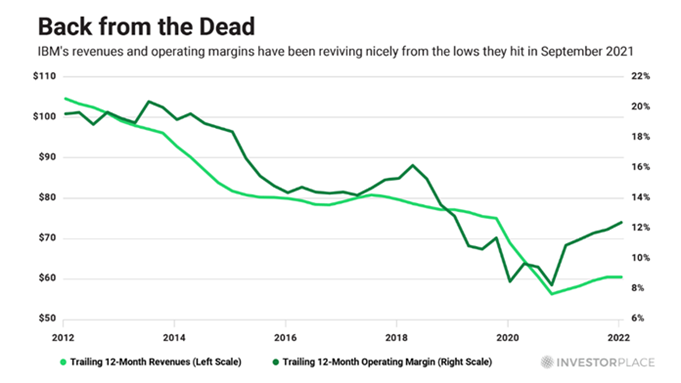

The below chart tells you almost everything you need to know about the “new” IBM…

The iconic computer company’s revenues and operating margins are no longer tumbling. They are rising once again.

After hitting a 30-year low in Sept. 2021, IBM’s revenues and margins have been making a noticeable recovery. These favorable financial trends do not prove IBM has embarked on a new growth trend, but they do support that thesis…

Because IBM’s fast-growing AI and hybrid cloud businesses will power most of its growth, future earnings reports could contain a few upside surprises.

I’m pleased to report that that exact forecast has come to pass. Because IBM’s revenue has continued moving higher, while its operating margins have rocketed from 12% at the time of my “Buy” recommendation to 21.5% in the most recent quarter, the company delivered a significant upside earnings surprise when it announced results on January 24.

The stock soared nearly 10% the following day… and hasn’t looked back since.

So, I believe IBM still offers significant upside potential.

Regards,

Eric Fry

P.S. We’ve reached a crossroads moment.

The labor landscape is rapidly changing as AI diffuses into other industries. And it’s going to create explosive opportunities for investors.