With the “Magic Kingdom” ready to launch its grand opening in Shanghai next week, a lot is riding on Walt Disney Co (DIS).

Enthusiasm is rampant in China, with reports of scalpers pushing up opening day ticket prices by upward of four times their official value. At the same time, DIS stock investors have been hit with volatility due to under-performing business units.

Enthusiasm is rampant in China, with reports of scalpers pushing up opening day ticket prices by upward of four times their official value. At the same time, DIS stock investors have been hit with volatility due to under-performing business units.

So far this year, Disney stock remains underwater … will the Shanghai opening and other items in their pipeline be enough to overcome critical challenges?

On the public relations front, management is hitting the notes that Disney stock investors want to hear. CEO Bob Iger has been all smiles as he prepares for the massive inroad into the Chinese entertainment sector.

Iger stressed the long-term outlook for Disney in terms of global market expansion, noting that he wasn’t overly concerned about China’s economic slowdown. He later backed up his bullishness, proclaiming that movies under the Disney brand will be produced in China within a year’s time. According to Bloomberg, the Asian powerhouse will soon be the biggest film market.

The courting of the Chinese movie industry is a desperately needed move — especially from the point of view of DIS stock. What has some investors sitting on the sidelines is that relative to the global media industry, Disney stock has a slightly higher premium against trailing earnings. To add to those fears, sales growth over the past ten years is mediocre at 5%. Taking into account the effects of inflation over the decade, that’s not much justification for DIS stock to continue its upward trek.

ESPN — which Disney owns 80% of — is a further exclamation mark toward the revenue problem. (InvestorPlace’s Lior Alkalay succinctly lays out the reason why ESPN has been a headache for anyone with significant exposure to Disney stock.) As media consumption rapidly moves toward direct program streaming as opposed to bundled cable packages, ESPN has reported a worrying drop in subscribers. Additionally, professional sporting rights have only gotten costlier, posing margin pressures for DIS stock.

Click to Enlarge

While acknowledging various growth challenges, many analysts are reluctant to dismiss DIS altogether. Strength in the brand and management team, especially Iger, is enough of a reason not to throw in the towel, according to CNBC contributor, Steve Weiss.

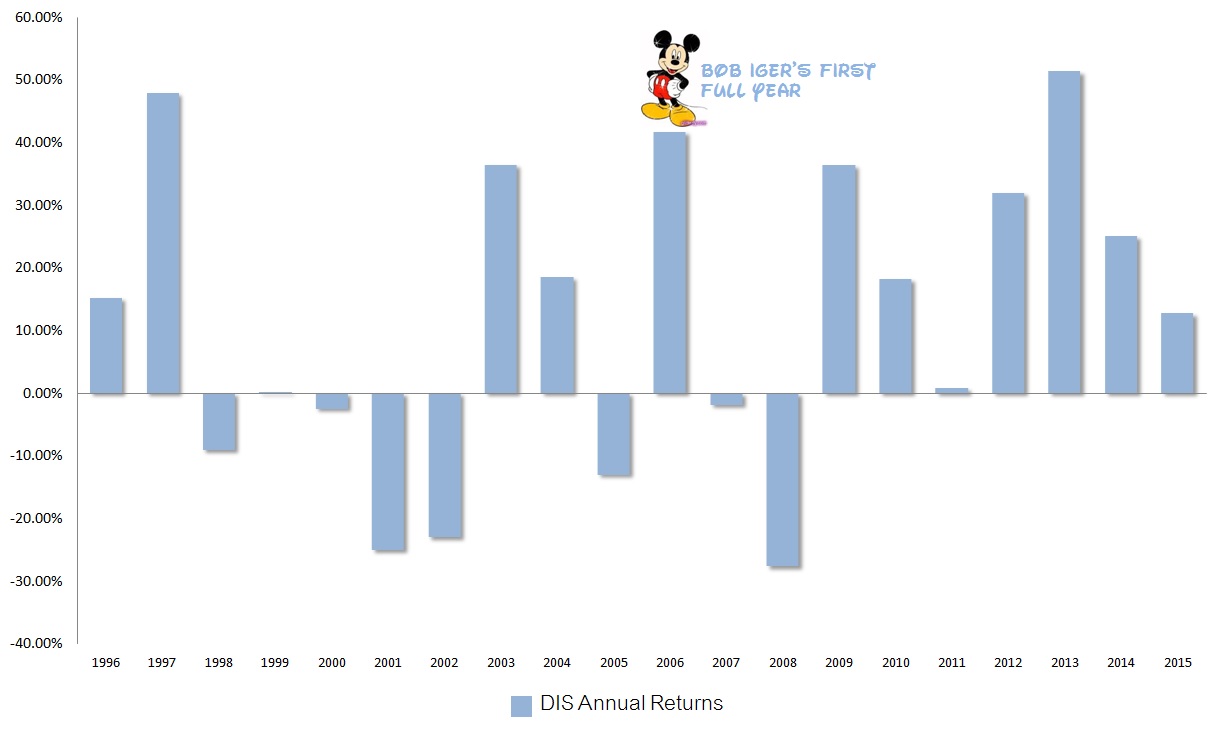

Since taking over the helm, DIS stock has seen a 260% increase in market valuation. Not only that, Iger righted a ship that was badly damaged from both internal and external turmoil.

This isn’t a matter of cheerleading analysts. In the ten years leading up to Iger’s takeover, DIS stock averaged under 5% for annual returns. Since his first full year as CEO, Iger raised that average to 19%, nearly quadrupling the previous expectations for Disney stock. Having done so much for the company, there’s every reason to trust Iger’s direction with Shanghai Disneyland and his global ambitions.

Whether it pays off for DIS stock buyers — especially for the newcomers — remains to be seen. On the positive side, DIS shares are historically sound. Going back to just a few years after its initial public offering, Disney stock has returned on average 18% every year. From an immediate timing perspective, there are advantages as well. On a year-over-year basis, DIS performs noticeably better in the second half of the year as compared to the first.

Click to Enlarge

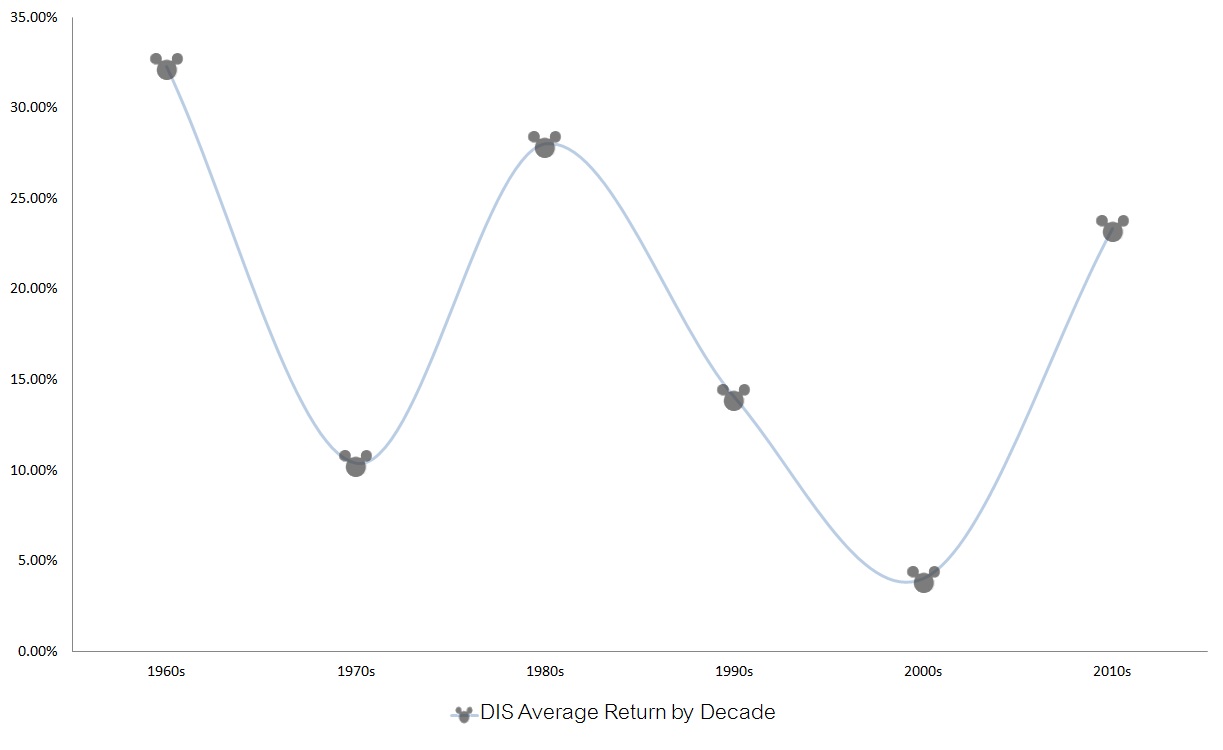

Primarily, when we look at DIS stock from a decade-to-decade framework, the data, while a matter of interpretation, isn’t necessarily encouraging.

Yes, Disney stock has a very distinct sinusoidal pattern that stems from its consistency. But, the pattern is negatively tilted. If we use history as our guide, we have a few good years remaining before things start to go awry.

That’s not a green light to jump on DIS stock today. There have been 10 times in the company’s history that DIS fell negative YoY in both the first and second quarter.

Of those occurrences, seven have resulted in the following third and fourth quarters also reporting YoY losses. And what about 2016? You guessed it — Q1’s $96.54 clocks in at 4% below the year-ago quarter’s $100.30, and Q2 is on pace to fall by nearly 8%.

The approach to DIS stock will largely hinge on personal expectations, and as a support beam, it does its job spectacularly well. DIS will provide more good years than bad. Iger’s track record and exciting expansion into China will see to that.

But Disney stock will likely disappoint if treated as the cornerstone of growth. There are fundamental headwinds that can potentially play spoiler. This is confirmed through broad technical performance, which has become progressively softer.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.