Usually, it’s not a good thing when the first adjective that comes to mind about a particular investment is “boring.” That descriptor conjures up images of retirement homes, bingo games, and amateur golf tourneys that frequently go over par. It’s the exact opposite of what you want to sell if you were an up-and-coming stockbroker. But AT&T Inc. (NYSE:T) is that rare animal that wears boredom well.

First and foremost, when discussing T stock, we have to acknowledge the AT&T and Time Warner Inc (NYSE:TWX) merger.

As InvestorPlace’s Lawrence Meyers notes, it’s a done deal. TWX shareholders have approved the merger, which makes T stock compelling again. He further stated that “in a matter of two years, AT&T stock has gone from moribund telecom play with a great dividend to a media powerhouse with a great dividend.”

Then there’s the matter of T’s acquisition of DirecTV. Regularly squaring off against rival DISH Network Corp (NASDAQ:DISH), DirecTV delivers better content, particularly if you’re a sports fan. As a side note, DISH is off more than 22% from its highs of 2014. T stock, in sharp contrast, is just a few cents short of its all-time high (on an adjusted basis).

But this brings us to an important question. Is T stock still worth buying at these elevated levels? Just a few years ago, AT&T was something more appropriate for “widows and orphans,” according to Meyers. No one — even those with deep pockets — wants to be caught holding the bag.

T Stock Is Built Like a Tank

Fortunately, I don’t think it’s possible to hold the bag on AT&T. Of course, you never say never — I’ve been burnt before with premature ramblings. I certainly don’t want to repeat the mistakes of occasionally misguided youth. But a select group of companies do exist that are too big and frankly, too boring to fail.

It’s often said that when people flip the switch on, they expect to see light. When that doesn’t happen, as in the case of power outages, people go a little crazy. Extend the blackout for a prolonged period of time, and you will have a major crisis on your hands. It’s cynical, but that’s why utility companies will always be in business. You can be grossly negligent like Tohoku Electric Power Co., Inc. (Japan) (OTCMKTS:TEPCY) and still get away with it.

The same analogy can be carried over to the telecommunications industry. People need their internet, and access to other digital devices. No internet and no TV is tantamount to a powder keg ready to burst. And AT&T has gotten so big that it’s probably not possible for it to totally implode into oblivion. That’s one reason why T stock is largely considered worry-free investing.

The other reason is that AT&T is unlikely to become irrelevant. InvestorPlace feature writer James Brumley states that the company “is already capable of delivering broadband to millions of houses and businesses across the nation, and it’s also capable of providing 4G wireless (soon to be 5G wireless) from coast to coast.” Even with this advantage, AT&T is nearing implementation of its AirGig technology — essentially, internet through electric utility lines.

So no, bag-holding on the fundamentals is definitely not a concern.

AT&T Stock: The Trend Is Your Friend

Of course, investment profits and losses are realized via the markets. It doesn’t matter how great the fundamentals are if the technicals won’t follow suit. Naturally, buying near all-time highs will cause any investor to take a step back before pulling the trigger.

However, T stock is bolstered by a number of attributes that makes it distinct from other opportunities. First, outside of rare exceptions, AT&T stock does not incur devastating, double-digit volatility. Aside from 2001, 2002 and 2008, the average down years measures only 6.7%. Chances are, if you pick T stock at an inopportune moment, you should recover fairly quickly.

Click to Enlarge

The second factor favoring AT&T stock is its upward bias. During the first quarter, returns for T stock are poor, averaging losses of 0.4% from the start of January to March end. Things pick up over the next three quarters, returning slightly over 13% so far.

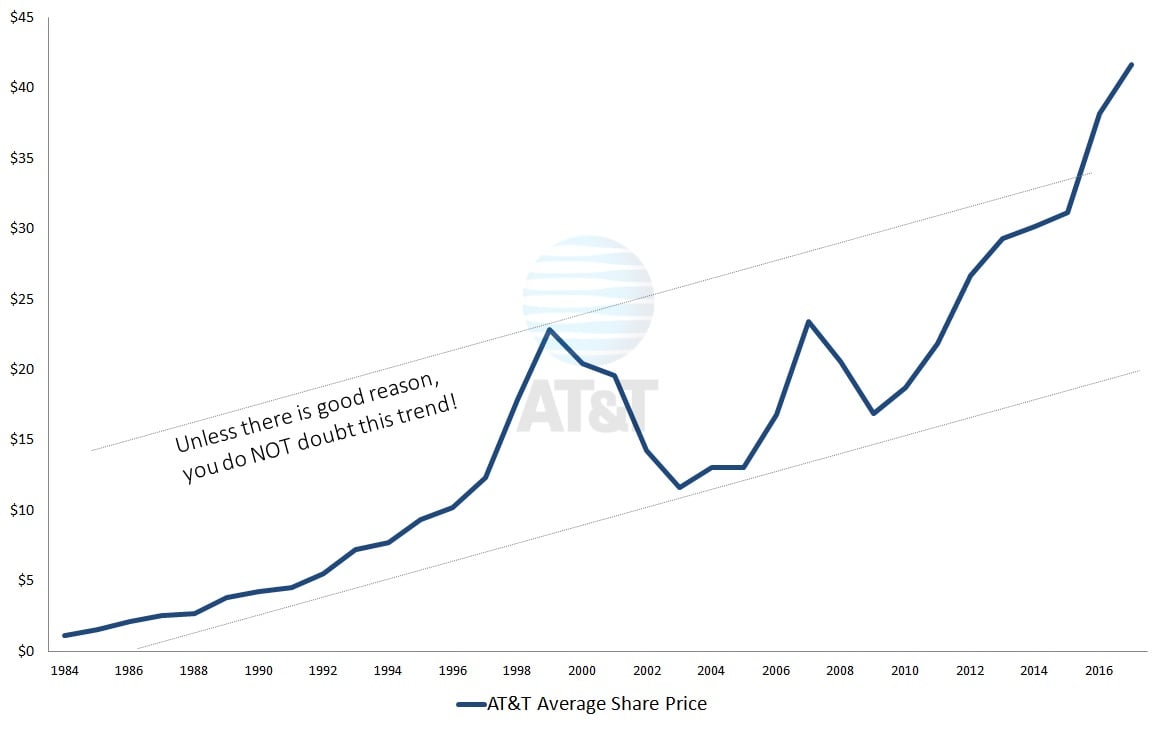

Finally, you just have to trust the long-term trend for T stock. And that’s really no step of faith. Since 1984, only two pronounced periods of bearishness are evident: the collapse of the tech bubble, and the Great Recession. Since we’re not going to suffer through macro-level pessimism all the time, AT&T stock is as reliable as a benchmark index fund.

Buying any company at all-time highs is never preferable. But holding onto preference could stymie profitability. T stock isn’t the flavor of the week. It’s built for the long-term, and for that purpose, AT&T has few genuine competitors.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.