In a way, many investors dream about owning a tiny slice of private companies. Whether it’s the Airbnb or Uber’s of the world or the earlier versions of now-public companies. You know, companies like Facebook (NYSE:FB) or Alphabet (NASDAQ:GOOG, NASDAQ:GOOGL) that went public with low values relative to today’s prices.

Even the old buy-and-hold on the IPO would have treated investors nicely at this point.

But what if these companies were to go private again after being public for a while? Public to private companies do exist. We’ve seen it before, most notably with Dell and founder Michael Dell. The conversion comes up as CEO Elon Musk now talks about taking Tesla (NASDAQ:TSLA) private.

There are less regulations and scrutiny for private companies, while more potential reward for those who get in on the deal. In Tesla’s case, there are still plenty of question marks.

With that in mind, let’s look at several public stocks that could or should consider becoming private companies.

Public to Private Companies #1: Tesla

Click to Enlarge

Should Tesla go public to private? Bulls and bears may both have their issues with the move. Bears feel that Musk’s announcement on Twitter (NYSE:TWTR) was illegal (it’s not, provided it’s true) and bulls believe there is far more upside than $420 per share, Musk’s proposed purchase price.

In any regard, the move would make sense for Tesla as a company. For one, it gets it out of the public spotlight. Gone are the quarterly reports and SEC filings, and the deafening march of short-sellers. With almost one-third of the float sold short, Tesla is surely a contested name.

Why else should it go private? It’s got a 5% holder in Tencent, a 3% to 5% holder in the Saudi Wealth Fund and a 20% holder in Musk. That’s anywhere from 28% to 30% of the company’s stock, with the Saudi Wealth Fund currently in discussion to buy more in a privatization deal.

Don’t forget, Musk’s other company also has Fidelity and Google as investors in his SpaceX company as well. Not to mention Tesla is based in Silicon Valley, where there is no shortage of venture capitalist and investor dollars to be had.

Tesla should also be GAAP profitable and cash flow positive in Q3 and Q4, while finally churning out close to 20,000 Model 3s per month. A $420 buyout price may equate to an ~$80 billion enterprise value, but it would also lock in Tesla’s stock price above a critical convertible bond price of roughly $360, maturing in February 2019. There’s another maturation in 2021 at the same price.

So all in all, it would make plenty of sense for Tesla to do the move, provided that it can.

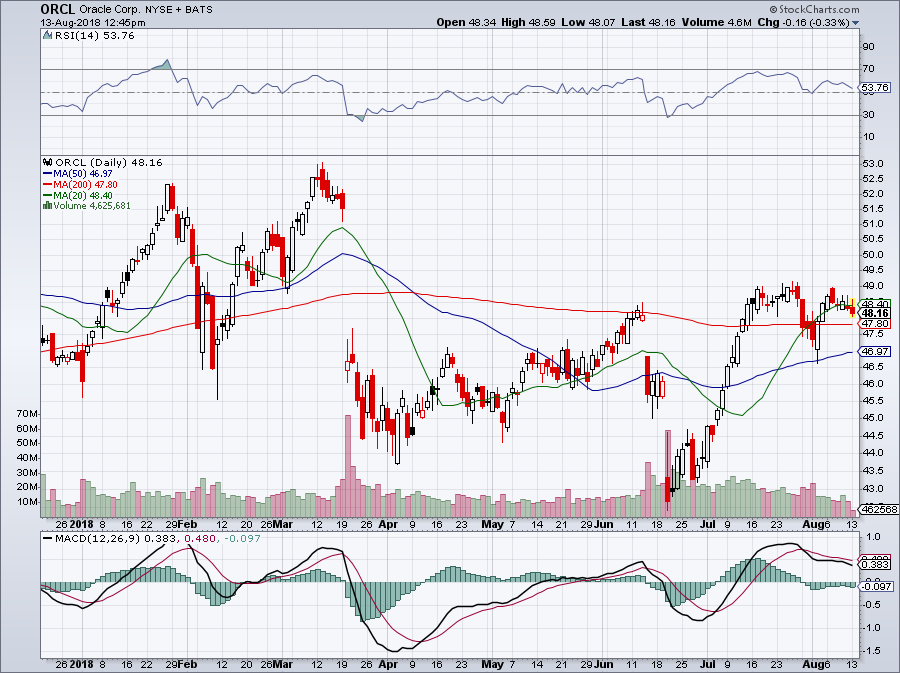

Public to Private Companies #2: Oracle

Click to Enlarge

Another company with a large co-founder is Oracle (NASDAQ:ORCL). Larry Ellison is the former CEO of Oracle and still owns a whopping stake in the company. As it stands, he owns almost 1.2 billion shares in ORCL or almost 30% of the company.

Oracle is no slouch when it comes to cloud and other enterprise applications. However, its valuation would have you thinking otherwise. ORCL stock trades at just 14 times this year’s earnings, which are set to grow ~7.5% year-over-year. Next year, analysts expect an acceleration to 8%.

While one could make a case for Oracle going private, it may not seem all that likely. Ellison would need to feel Oracle would be better run as a private company or that the market is unfairly valuing the entity.

Otherwise, I imagine he’s content collecting the 76 cent-per-share annual dividend on his 1.2 billion share stake and waiting for his principal to appreciate.

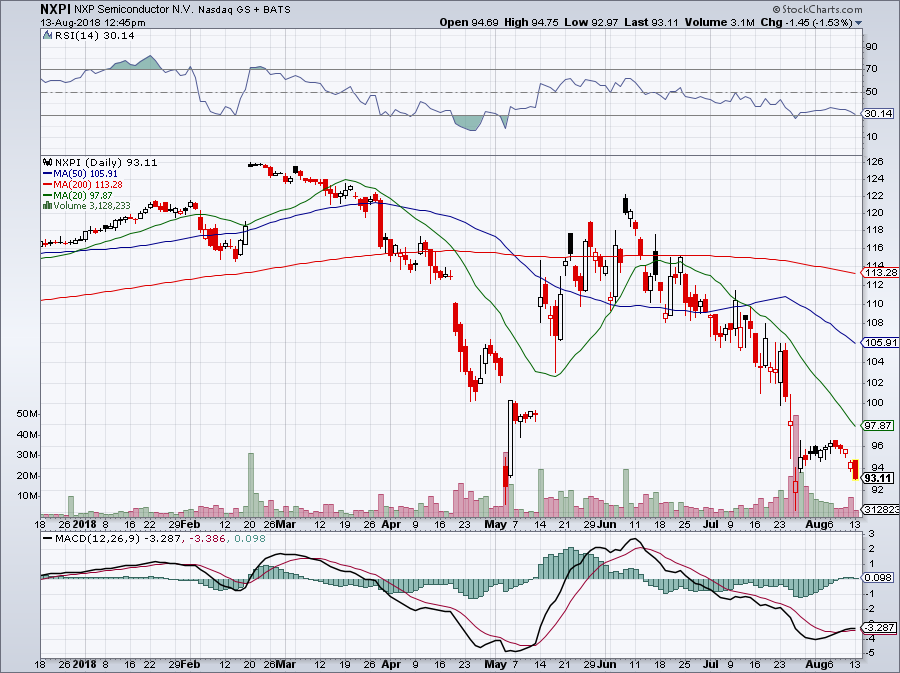

Public to Private Companies #3: NXP Semiconductors

Click to Enlarge

Remember when we all thought Qualcomm (NASDAQ:QCOM) would buy NXP Semiconductors (NASDAQ:NXPI) for almost two years? The two first agreed on a takeout at $110, but so much time had elapsed before finding approval that the bid was revised up to $127.50.

China was the lone power to refuse the deal (not by deciding to deny it, but instead by not making any ruling at all). That meant Qualcomm’s window to purchase NXPI passed. The company paid its $2 billion breakup fee and is moving on; the saga is over.

That may be true between Qualcomm and NXP, but the latter has shown a willingness to sell and it wouldn’t be surprising if it happened with another party.

The semiconductor company has a low valuation — just 14 times this year’s earnings and just 12 times next year’s estimates — and is positioning itself in front of a number of catalysts. As such, analysts expect strong growth in 2019.

It makes high-quality products in growth markets where it can benefit from accelerating demand in the future. That makes NXP an attractive target, even if it means a few buyers teaming up together to take it private.

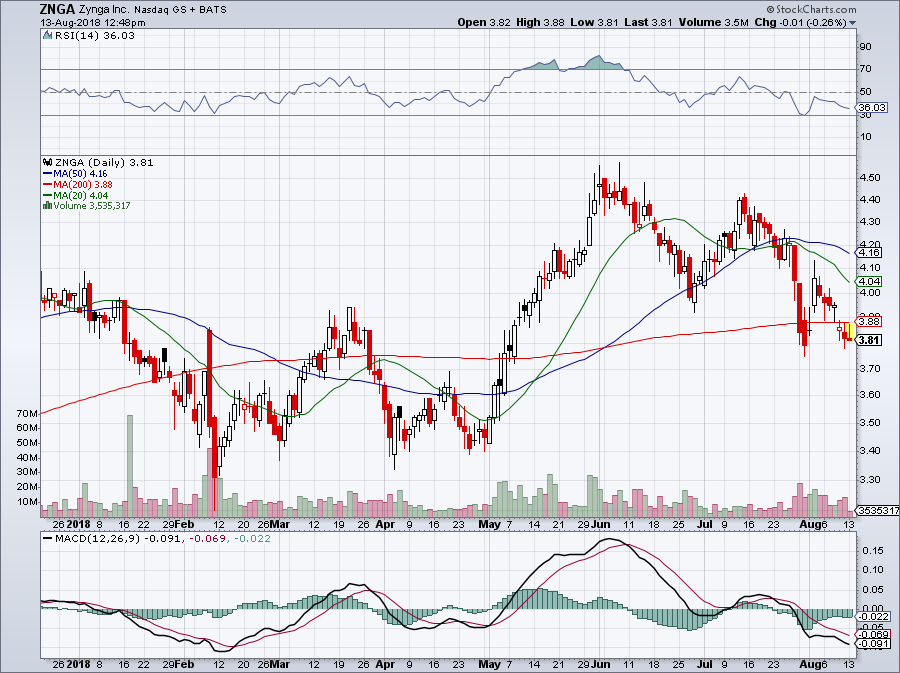

Public to Private Companies #4: Zynga

Click to Enlarge

A bit more controversial, but it’s all about what the C-suite sees for Zynga (NASDAQ:ZNGA

) and its future.

The company is expected to grow sales by 13% this year and next year, while analysts expect earnings to grow 67% and 27% in 2018 and 2019, respectively. Further, Zynga has $400 million in cash, no debt and a $3.6 billion market cap. It’s also operating and free cash flow positive.

As regulators appear to be loosening their stance on online gambling and sports gambling, Zynga could be a big-time winner. Its mobile apps and poker games would be a simple transition, a great situation for Zynga’s potential future. While that may not be great for all people to have easy access to, it’s a direction we could be going in.

If management or an outside party sees that value ahead of time, they may try to take ZNGA off the board.

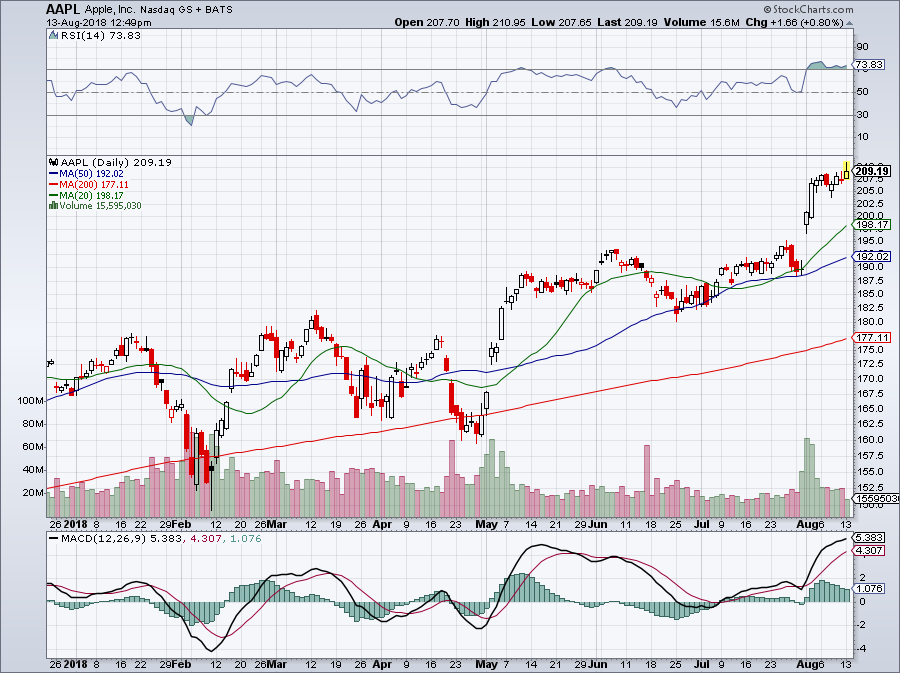

Public to Private Companies #5: Apple

Click to Enlarge

In a way, it’s like Apple (NASDAQ:AAPL) has already decided it wants to be on the list of private companies. It doesn’t make splashy M&A purchases, rakes in billions of dollars in profit each quarter and has massive free-cash flow.

Warren Buffett’s Berkshire Hathaway (NYSE:BRK.A, NYSE:BRK.B) is a huge buyer of Apple too. The Oracle of Omaha continues to gobble up millions of shares, buying over 75 million in the first quarter of 2018. It’s now his largest position and given that Berkshire has more than $100 billion to invest, Buffett may just keep going where he feels most comfortable.

One reason he likes Apple? Its buyback, which is like a silent, unannounced go-private move. After mopping up billions in stock already, in May the tech giant announced a $100 billion repurchase plan.

That was fueled by the new tax system, but I wouldn’t be surprised to see Apple buy back at least $100 billion each year going forward. Keep in mind, it just hit a $1 trillion market cap — not that InvestorPlace readers should be surprised. Even at today’s valuation, Apple’s still buying back 10% of the float. On a deep correction, it’s an even larger percentage.

As that buyback continues, the company will eventually retire a bulk of the stock, driving shares higher and higher. It’s like an unofficial privatization bid.

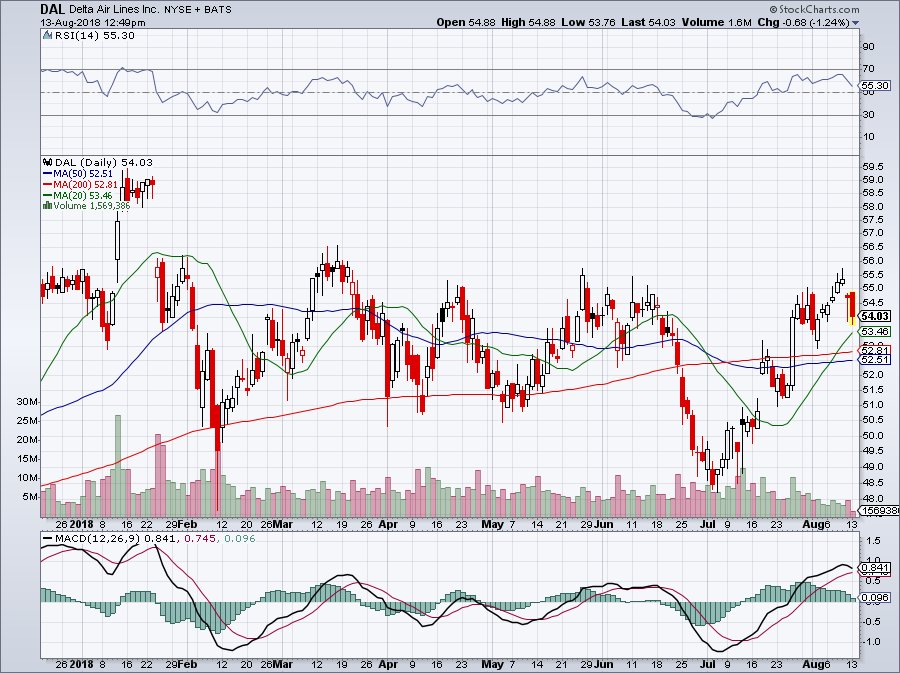

Public to Private Companies #6: Delta

Click to Enlarge

Another Buffett favorite, Delta has some great-looking business fundamentals. Delta Air Lines (NYSE:DAL) kicks off a ton of free-cash flow, has very good growth and comes at a low valuation.

In the short-term, there can be currency fluctuations, “route wars” and periods of economic uncertainty. But the bottom line is simple: people need to get from point A to point B and through the air is one main way. The airline industry is in a period of secular growth and that bodes well for high-quality companies.

Delta doesn’t have an Elon Musk per se, but that wouldn’t stop a few funds and groups from putting together a privatization bid.

Current revenue estimates call for 7.5% growth this year and 4.5% growth next year. Even better though is the expectation for earnings, which calls for 13% growth this year and 18.5% next year. That shows that margins are expanding, while management has already said it’s committed to returning a plentiful amount of capital to investors. Best of all, shares trade at just under 10 times earnings.

Not long ago we put the four largest U.S. airlines up against each other and concluded that Delta was the top pick.

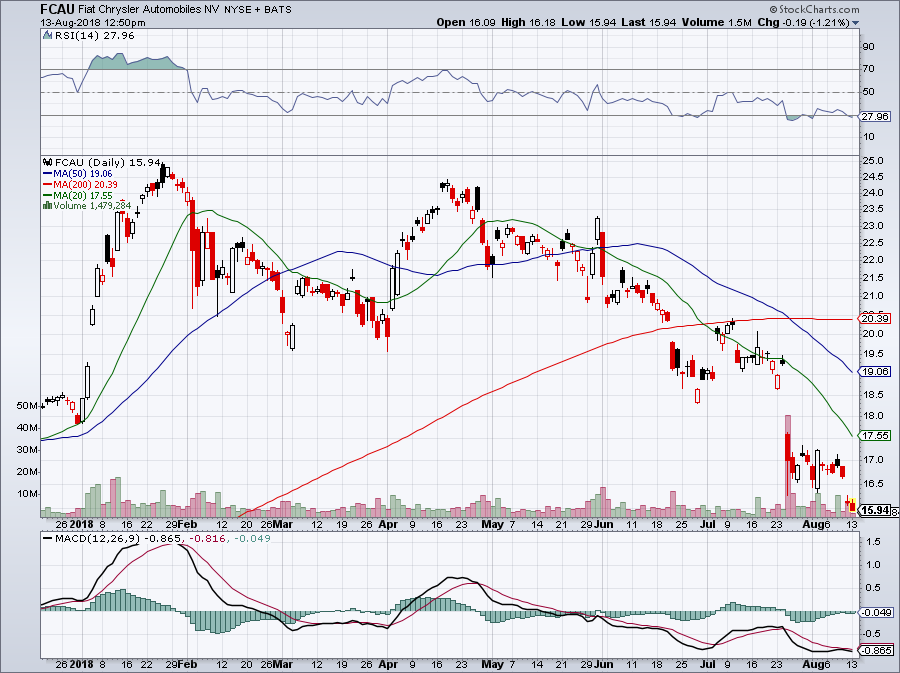

Public to Private Companies #7: Fiat Chrysler

Click to Enlarge

There were a lot of names vying for this last spot. One of them was General Motors (NYSE:GM), given its low valuation and solid profitability. But it would be unlikely for the automaker to go back to the private markets.

Perhaps too then, it would be unlikely for Fiat Chrysler (NYSE:FCAU) to do so too. But clearly the market is not valuing the company appropriately. Shares were under pressure before legendary auto CEO Sergio Marchionne suddenly passed away a few weeks ago. Since then, FCAU and Ferrari (NYSE:RACE) have been under pressure.

Ferrari still carries a premium multiple, but FCAU trades at a disrespectful 4.4 times this year’s earnings. Based on 2019 estimates, shares trade at about 4 times earnings. And no, business is not in free-fall. Analysts expect positive revenue and earnings growth this year and next year. That’s more than GM and Ford Motor (NYSE:F) can say, both of which have higher valuations, (although both pay out dividends too).

Fiat may have a tough quarter or two without Marchionne, but its valuation is ridiculous. While the new management may not be eager for a deal, Marchionne had pushed for one in the past. Given this valuation, perhaps shareholders will push for one too. Or at least a spinoff strategy for some of its brands. Remember, Ferrari was a FCAU spinoff in the past.

Even 6 times 2019 earnings puts shares up near $24, almost 50% above current levels. If outside investors don’t see that, I don’t know what they find attractive.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell is long GM, NXPI and AAPL.