If you’ve been one of the people looking for tech stocks to buy in the past two years, you’re likely quite happy with your portfolio’s performance. I wrote an article in late 2022 titled “25 Tech Stocks to Buy Before They Take Off in 2023.” Almost all of these tech stocks have been standout performers, even more so than I would have expected back then.

Of course, we are at the cusp of an inflection point since the Federal Reserve will likely cut rates in the months ahead. However, there is still time for the market to perform well and keep rewarding shareholders. The tech-heavy Nasdaq has delivered 70.6% in gains since Dec. 31, 2022. We’re just six months into 2024, and it has already gained 21%, being just under 18,000. Thus, 20,000 by the end of the year isn’t a stretch if the rally continues. If you think that is the case, look at the following stocks.

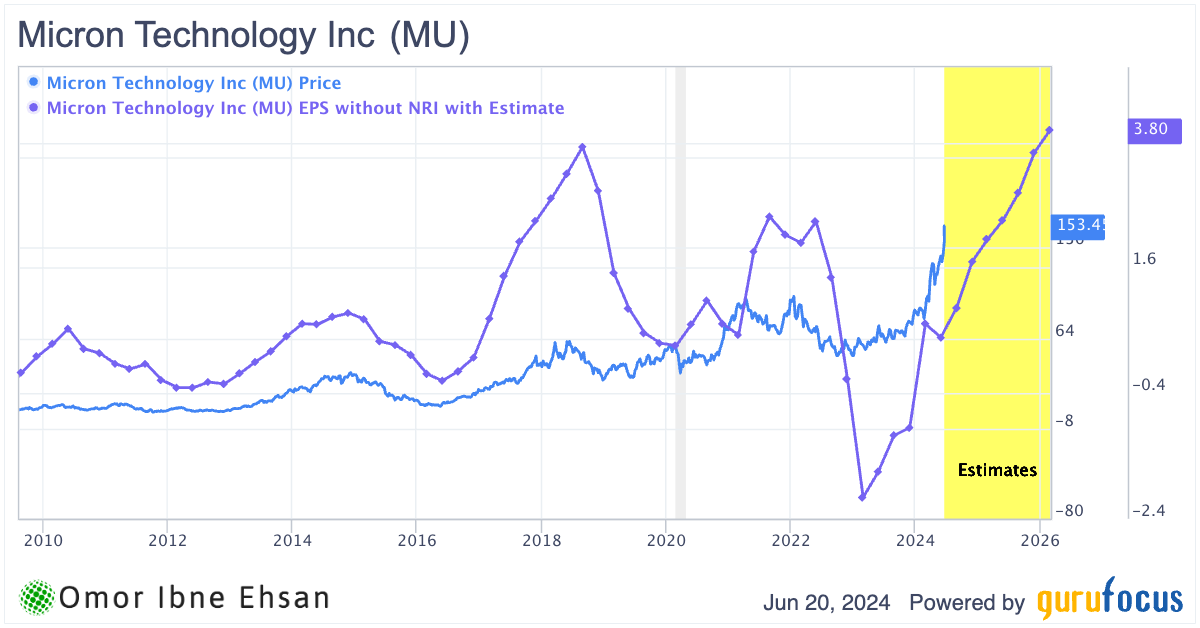

Micron Technology (MU)

Micron Technology (NASDAQ:MU) makes memory and storage solutions. The company is well-positioned to benefit from the artificial intelligence (AI) and data storage megatrends that are propelling the tech sector higher. In its latest earnings report, Micron crushed expectations. Revenue of $5.82 billion was up a staggering 57.7% year-over-year (YOY), and EPS of 42 cents beat estimates by 66 cents.

The company had AI server demand drive rapid growth in key products like HBM, DDR5 memory and data center SSDs. This is creating a positive ripple effect on pricing across MU’s entire portfolio. Micron Technology now expects DRAM and NAND prices to keep rising throughout 2024, potentially leading to record sales and much higher profits in fiscal 2025. It has over 90% of its NAND output on 176 and 232-layer nodes.

Therefore, analysts expect around 60% sales growth this year, along with EPS reaching $9 next year and $11.6 in 2026. This means investors pay just 13 times 2026 forward earnings, which is much cheaper than most other AI stocks. I think MU stock will keep climbing as long as the broader market cooperates.

Click to Enlarge

But remember, the stock has been getting ahead of estimates, so it could underperform greatly if the Nasdaq doesn’t perform well.

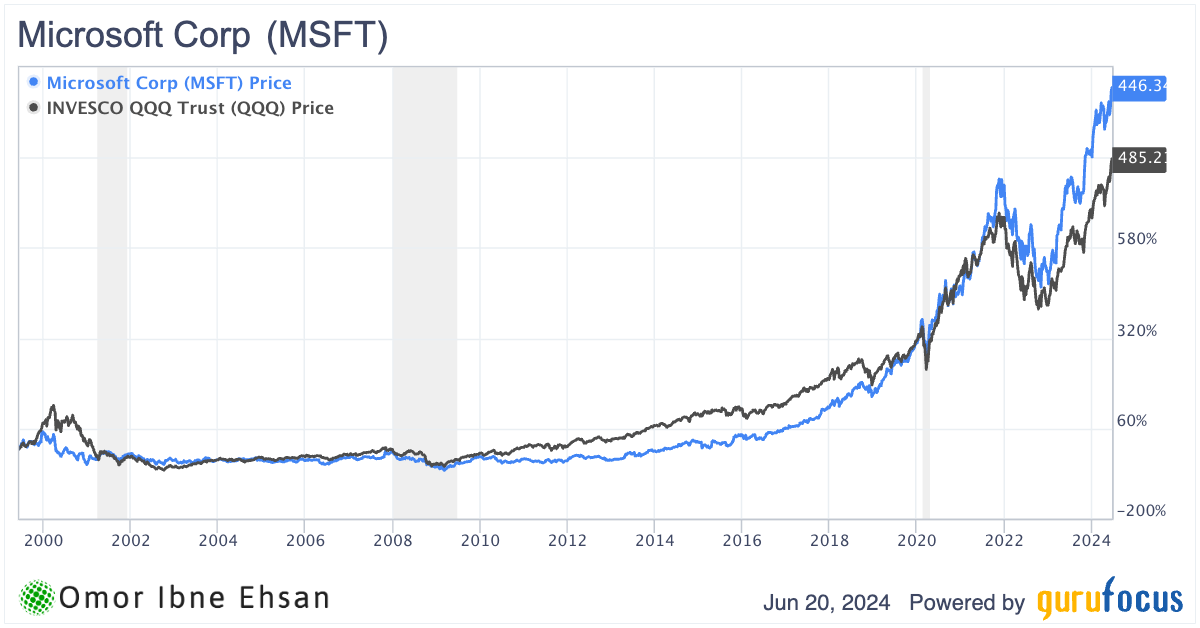

Microsoft (MSFT)

Microsoft (NASDAQ:MSFT) posted impressive Q3 results, with revenue growing 17% to $61.86 billion and EPS beating estimates by 10 cents. The company may be poised to benefit from major AI tailwinds that could propel its stock past $550 if the Nasdaq reaches 20,000.

Furthermore, Microsoft’s Azure cloud platform is taking market share. And, its OpenAI partnership has over 65% of the Fortune 500 users using Azure OpenAI Service already. Copilot AI is driving a new era of productivity across Microsoft’s apps. The company’s software moat remains unassailable. In fact, it’s hard to imagine offices functioning without Windows, Office and Teams.

With revenue accelerating as customers migrate to Azure and its early lead in AI, Microsoft deserves its premium valuation. The stock has surged 32% in the past year. But many see more upside ahead as Microsoft’s AI innovations and cloud leadership compound its advantages.

Click to Enlarge

If growth sustains at this pace, MSFT breaking $550 looks very achievable in a Nasdaq 20,000 scenario.

KLA Corp (KLAC)

KLA Corporation (NASDAQ:KLAC) provides process control and yield management solutions for the semiconductor industry. The firm is well-positioned to benefit from the powerful megatrends driving the tech sector, such as AI, 5G and IoT.

With its hands in many critical hardware segments, KLA Corp. is riding multiple tailwinds that could propel its growth. While the company’s revenue declined 2.99% YOY to $2.36 billion, it still beat estimates by $38.51 million. Also, KLAC delivered an impressive EPS of $5.26, exceeding expectations by 20 cents.

Although the firm’s growth has moderated recently, I think the company’s consistent ability to surpass Wall Street projections bodes well for its future prospects. As the semiconductor industry continues to boom, driven by insatiable demand for cutting-edge chips, KLAC is poised to thrive. If it maintains its momentum and the Nasdaq soars past 20,000, I wouldn’t be surprised to see the stock catapult beyond the $1,000 mark.

It is a very compelling opportunity to tap into multiple tech megatrends through a single, well-executing company.

American Express Company (AXP)

A company doesn’t have to be in the Nasdaq to benefit from its tailwinds. American Express (NYSE:AXP) is a global financial services company best known for its credit card products and services. The company reported strong Q1 of 2024 results, with revenues up 11% YOY to $15.8 billion and EPS surging 39% to $3.33.

American Express is poised to benefit from the ongoing shift toward digital payments. As one of Warren Buffett’s favorite holdings, AXP has a proven track record of delivering consistent growth through economic cycles.

With the company reaffirming its full-year guidance for 9-11% revenue growth and $12.65-$13.15 EPS, AXP’s premium customer base and spending-centric business model position it well for upside in a bullish market. Analysts project around 9% annual revenue growth and 15% annual EPS growth going forward. If the Nasdaq rallies to 20,000, I wouldn’t be surprised to see AXP’s valuation cross $270.

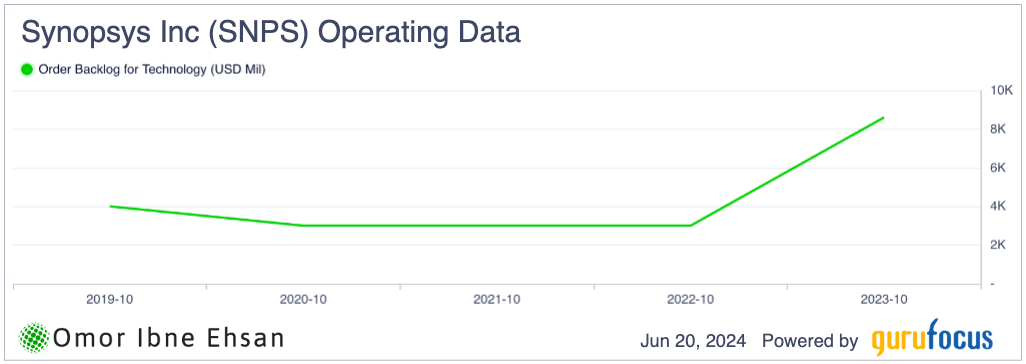

Synopsys (SNPS)

Synopsys (NASDAQ:SNPS) provides software and IP used to design and verify advanced semiconductors and electronic systems. In Q2, Synopsys delivered strong results, with revenue up 15% YOY to $1.45 billion and non-GAAP EPS jumping 26%.

I believe Synopsys is well-positioned to benefit from the booming semiconductor industry. With the Nasdaq potentially reaching 20,000 in 2024, Synopsys should have ample room for further upside despite already gaining over 42% in the past year. While the growth may seem mediocre relative to the valuation, Synopsys has been one of the most consistent compounders over the past decade. Also, the backlog growth is very impressive.

Click to Enlarge

Management raised full-year revenue and EPS guidance. And, they provided an update on the pending Ansys (NASDAQ:ANSS) acquisition, which should expand Synopsys’ TAM and capabilities. As long as the Nasdaq keeps climbing, expect Wall Street to continue rewarding this dependable semiconductor stock.

Lam Research (LRCX)

Lam Research (NASDAQ:LRCX) is a leading semiconductor equipment manufacturer. The company delivered strong Q3 of 2024 results, with revenues, profitability and EPS all exceeding guidance. The company sees WFE spending in the low to mid $90 billion range for 2024, driven by robust DRAM demand and domestic China investment.

I believe Lam Research is perfectly positioned to ride the unstoppable AI and semiconductor boom. Generative AI’s transformative use cases are set to deliver trillions in economic benefits, requiring massive chip manufacturing investments. LRCX’s expertise in accelerating tech advancement while reducing fab costs make it a top beneficiary.

The stock has skyrocketed 77% over the past year, breaking $1,000. With a 10-for-1 stock split coming in October and a $10 billion buyback, LRCX could become even more attractive to investors. If the Nasdaq continues its march toward 20,000, Lam Research may be a star performer.

Cadence Design Systems (CDNS)

Cadence Design Systems (NASDAQ:CDNS) provides software, hardware and services for electronic design automation. The company reported solid Q1 results, with revenue of $1.01 billion and EPS of $1.17, beating estimates by 4 cents. Management raised full-year guidance on the back of a record $6 billion backlog.

CDNS is well-positioned to benefit from the AI super cycle. The company’s Cadence.AI portfolio is delivering solutions that accelerate chip and system development. Customers like Intel (NASDAQ:INTC), Broadcom (NASDAQ:AVGO) and Qualcomm (NASDAQ:QCOM) are already seeing remarkable productivity gains.

Moreover, the stock has been a consistent outperformer. However, I think the expanding total addressable market leaves ample room for further upside. As more companies rush to automate processes and integrate software, Cadence’s best-in-class solutions should see robust demand.

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.