The stock market has been stellar so far in 2024. The S&P 500 and Nasdaq have hit fresh all-time highs, but volatility could creep back in as rate cuts take effect. This may seem counter-intuitive. But historically speaking, recessions and downturns have aligned with the Federal Reserve initiating rate cuts.

Yet, despite the near-term uncertainty, I remain optimistic about the market’s prospects over the mid-to-long term. Why? History has shown repeatedly that a well-diversified portfolio of high-quality companies can weather any storm and deliver solid returns.

In fact, some of the best-performing stocks of the past decade were those that investors simply bought and held. That’s why I think it’s worth looking into a diversified basket of stocks that could keep performing well going forward. Let’s explore seven such stocks to buy that may fit the bill.

Berkshire Hathaway (BRK-A, BRK-B)

Berkshire Hathaway (NYSE:BRK-A, NYSE:BRK-B) continues to be a darling of Wall Street. Analysts are issuing strong buy ratings on the company’s more affordable Class B shares. They see the stock as undervalued at current levels, with an average price target 15% above the current trading price. I tend to agree that owning Berkshire Hathaway is like having a diversified portfolio all on its own.

The company holds a wide array of businesses, from insurers to the BNSF railway. This allows Buffett to nimbly shift capital from lagging industries to those with more promise. With the company’s cash hoard expected to top $200 billion by quarter-end, the Oracle of Omaha has immense flexibility to capitalize on opportunities.

Also, Berkshire Hathaway benefits from some key economic tailwinds. Its energy and utility operations provide steady cash flows, while its insurers are well-positioned in an environment of rising interest rates. And with the U.S. economy still expanding, the firm’s industrial and consumer businesses have a favorable backdrop.

While Buffett’s advancing age may concern some investors, the iconic investor shows no signs of slowing down. He’s built a company that can endure for the long haul and has a succession plan in place. For those seeking a “set it and forget it” type of investment, Berkshire Hathaway remains a compelling choice.

Amazon.com (AMZN)

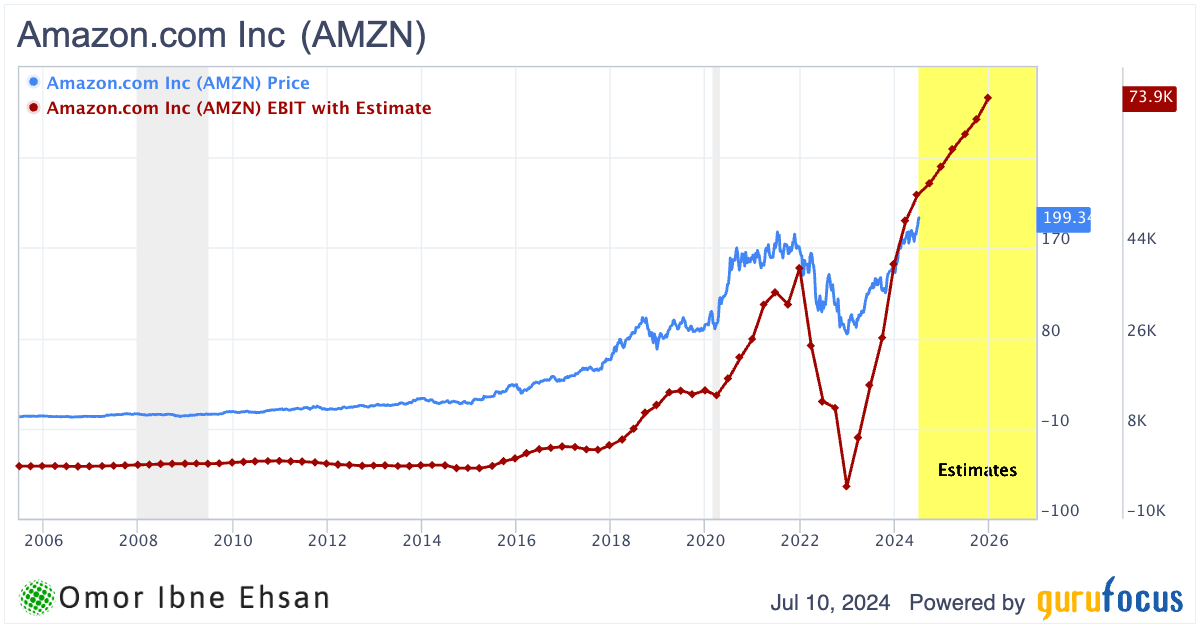

This e-commerce and cloud computing giant is riding several powerful megatrends that I believe position it extremely well for continued growth in the years ahead.

First off, Amazon’s (NASDAQ:AMZN) investment in artificial intelligence (AI) startup Anthropic is already paying major dividends. Anthropic’s latest model, Claude 3.5, is outperforming OpenAI’s new GPT-4o on most benchmarks.

Secondly, Amazon Web Services (AWS) continues to dominate the cloud infrastructure market with a 17% revenue jump. As more companies shift workloads to the cloud, including AI applications, AWS provides a strong and stable growth engine for Amazon.

Amazon’s stock does trade at a steep premium, but I believe this is justified given the company’s tremendous growth prospects that extend far beyond e-commerce. Multiple analysts have raised price targets, with Jefferies seeing an 18%-plus upside.

Yes, Amazon is an expensive stock. But I think it’s worth paying up for a company with such a wide moat. Other “Magnificent 7” stocks have soared past their 2021 peaks, but AMZN trades around $199 compared to the $186 peak in 2021.

Click to Enlarge

Therefore, operating income should lead to more upside if they materialize as expected.

Alphabet (GOOG, GOOGL)

Despite concerns about AI, Google’s search dominance remains rock solid. The latest data from Statista shows Google still commands over 82% of the global search market share. Bing barely made a dent. It makes sense that Alphabet (NASDAQ:GOOG, NASDAQ:GOOGL) has done so well, as Wall Street realizes the bear thesis has been wrong.

Google now has its own powerful AI called Gemini that it’s integrating into Search. This should help expand the types of queries Google can handle and improve user satisfaction. Plus, YouTube has been making aggressive moves to boost ad revenue. It is the world’s second most visited site. And cracking down on ad blockers was a smart decision that will likely pay big dividends. Analysts seem to agree, with the majority rating Alphabet’s stock a strong buy.

Consider these tailwinds, along with Google Cloud’s strong 28% growth and the company’s leadership in mobile with Android. Thus, the future looks very bright for Alphabet. The stock has already surged 36% year-to-date (YTD), but I wouldn’t be surprised to see it go much higher as these AI investments and YouTube changes bear fruit.

Visa (V)

Visa (NYSE:V) continues to ride the megatrend of the global shift from cash to digital payments, which has years of runway ahead. The company delivered another strong quarter, with revenue up 10% and EPS growing 20%. Key business drivers like payments volume, cross-border transactions and processed transactions all showed relative stability and growth.

I’m optimistic about Visa’s future prospects. The pandemic accelerated the war on cash, and much of that behavior change has persisted even as economies reopened. Visa is well-positioned to capture the $20+ trillion opportunity to convert cash, checks and domestic network transactions to its network, especially in emerging markets. Contactless payments, e-commerce and value-added services provide additional levers for growth.

Analysts remain bullish on the stock, with 19 buy ratings and a $317 average price target, implying 19% upside. Visa benefits from powerful network effects. The more merchants that accept Visa, the more consumers want a Visa card, creating a virtuous cycle. This has enabled remarkably consistent and profitable growth for a company of Visa’s immense scale.

Additionally, Visa’s business model can thrive in any economic environment. In a strong economy, payment volumes rise. When interest rates are high, Visa earns more on credit balances. However, in a weaker economy with low rates, consumers tend to borrow and transact more on credit, so Visa still wins. It’s a great way to gain exposure to the financial sector while sidestepping many of the risks.

McDonald’s (MCD)

McDonald’s (NYSE:MCD) stock has had a rough start to 2024, down over 17% YTD amid broader market volatility. However, the recent weakness presents a compelling buying opportunity for long-term investors.

McDonald’s is benefiting from its affordable fast food, drive-thru convenience and digital ordering. The company’s scale advantages and strong brand allow it to weather economic downturns better than its peers.

In fact, McDonald’s tends to outperform during recessions as cash-strapped consumers trade down to lower-priced options. The company grew earnings by double-digits annually during the Great Recession. More recently, McDonald’s held up relatively well during the Covid-19 pandemic thanks to its drive-thru lanes and delivery partnerships. Its franchised restaurant count actually grew in 2020.

Click to Enlarge

If you’re looking for exposure to the restaurant industry, McDonald’s is the cream of the crop. Analysts seem to agree, with firms like JPMorgan (NYSE:JPM) and Bank of America (NYSE:BAC) recently reiterating their bullish ratings on the stock. While near-term headwinds remain, McDonald’s entrenched popularity and recession-resistant business model make it a compelling long haul. Don’t be surprised to see the Golden Arches shine bright once again.

Antero Midstream (AM)

Antero Midstream (NYSE:AM) is riding high on the tailwinds of a shifting global energy landscape. The company recently reported strong first-quarter 2024 results, with double-digit growth in EBITDA and free cash flow. Also, AM placed a new compressor station into service to support future throughput growth in the liquids-rich Marcellus Shale.

Further, Antero Midstream is well-positioned to benefit from Europe’s move away from Russian gas. The E.U. has dramatically reduced its reliance on Russia, with the U.S. emerging as its top liquified natural gas supplier. Even if the war were to end, I expect these sanctions to persist. Moreover, Europe will likely prioritize energy security even if sanctions are not in place. Additionally, natural gas prices have rebounded significantly.

With a 6.12% dividend yield, Antero Midstream should give you more than enough income. The stock has climbed nearly 28% over the past year, too.

Chubb (CB)

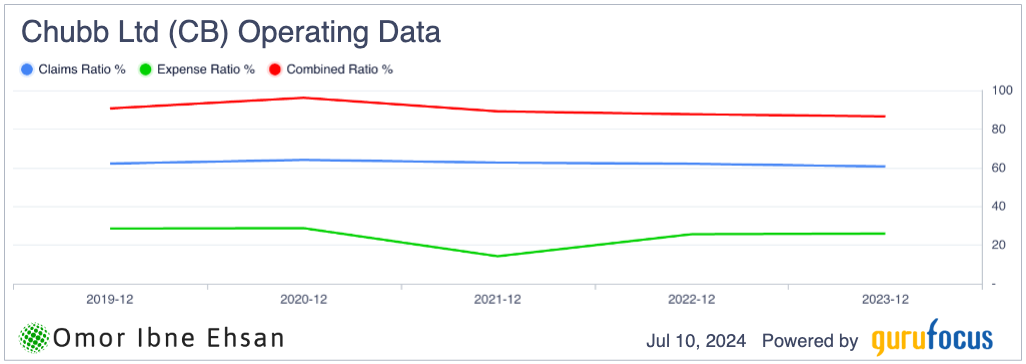

Notably, the insurance industry is one of the most consistent and stable sectors. And within this space, Chubb (NYSE:CB) is one of the best bets you can make. The company has been growing at an impressive clip. Over the past year alone, Chubb stock has climbed nearly 35%.

In Q1 of 2024, Chubb reported strong earnings, with core operating income up over 20% to $2.2 billion and EPS surging nearly 23%. Also, Chubb is smartly leaning into growth areas like cyber insurance and climate risk mitigation, which could eventually become major businesses. The profitability is solid due to its combined ratio of 86.5%. Within insurance, a combined ratio below 100% translates to an underwriting profit.

Click to Enlarge

Analysts are bullish on Chubb’s prospects. The stock has nearly a dozen buy ratings, and its average price target implies decent upside from current levels. Notably, Warren Buffett’s Berkshire Hathaway has built a multi-billion dollar stake in Chubb. All things considered, it is the best stock you can buy right now in the insurance industry.

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

On the date of publication, the responsible editor did not have (either directly or indirectly) any positions in the securities mentioned in this article.