After reporting a solid quarter in January, Advanced Micro Devices, Inc. (NASDSAQ:AMD) left its doubters in the dust as it was ripping higher. After hitting nearly $14 in late-January though, AMD stock was below $11 just a few days later.

What the heck happened?

Well, the PowerShares QQQ Trust, Series 1 (ETF) (NASDAQ:QQQ) took a dive, crumbling about 10% in 10 days time. It hit some of the market’s best stocks and there’s no way to know for certain whether the selling is over with. But after a good quarter, where does that leave Advanced Micro Devices stock?

If you don’t own it already, it’s one that should be on your watchlist.

Breaking Down AMD Stock

On Jan. 30, AMD beat on earnings per share and revenue expectations, growing sales 33% year over year. Management’s outlook calls for first-quarter sales of $1.5 billion to $1.6 billion, far ahead of analysts’ estimates calling for $1.25 billion. A change in accounting could be responsible for the wide difference in expectations, though.

Another big positive was AMD’s computing and graphic business, which saw sales climb 60% YOY. We know based on comments from Nvidia Corporation (NASDAQ:NVDA) that demand in this segment remains robust.

It’s very clear that AMD’s management, led by CEO Lisa Su, is making all the right moves. There’s a clear path to profitability, reducing debt, growing sales and boosting margins. In fact, those are some of the reasons Argus analyst Jim Kelleher recently slapped a “buy” rating on the stock. His $18 price target suggests more than 50% upside from current levels.

And isn’t that exactly what we want — a company that’s figured out how to harness growth, while cutting down its debt and boosting margins? Overall revenue for 2017 jumped 25%, while analysts are looking for another 18% increase in 2018. They also expect earnings to more than double from 17 cents per share to 39 cents per share in fiscal 2018. In 2019, forecasts call for EPS of 54 cents.

Valuing Advanced Micro Devices Stock

AMD stock isn’t as expensive or toxic as some investors have made it out to be. As of the most recent quarter, AMD had cut its long-term debt by 7.7% YOY, or by $110 million, down to $1.35 billion.

I have made the case several times over the past year that

AMD stock is cheap vs. its peers on a price-to-sales (P/S) basis. That remains true today. Advanced Micro Devices stock trades at just 2.1 times its trailing twelve months of sales. NVDA stock trades at 14.5 times trailing sales, although its earnings valuation isn’t as bad. Intel Corporation (NASDAQ:INTC) trades at 3.3 times sales. So, AMD is attractive on this metric.

But more impressive is that AMD stock trades at 30 times this year’s earnings and just 22 times 2019 estimates. While this may seem like an expensive stock, consider that this is drastically less expensive than just a year or two ago. Further, it’s more in-line with its peers. NVDA and Intel trade at 37 and 12.6 times this year’s earnings, respectively.

Admittedly, NVDA will likely blow through estimates and commands a higher valuation because of its higher quality business. Intel stock is drastically cheaper on an earnings basis because it’s only forecast to grow earnings 2.3% this year. AMD’s 130% growth is quite impressive and at sub-$12, I don’t have much of a reason to bet against it.

Trading AMD

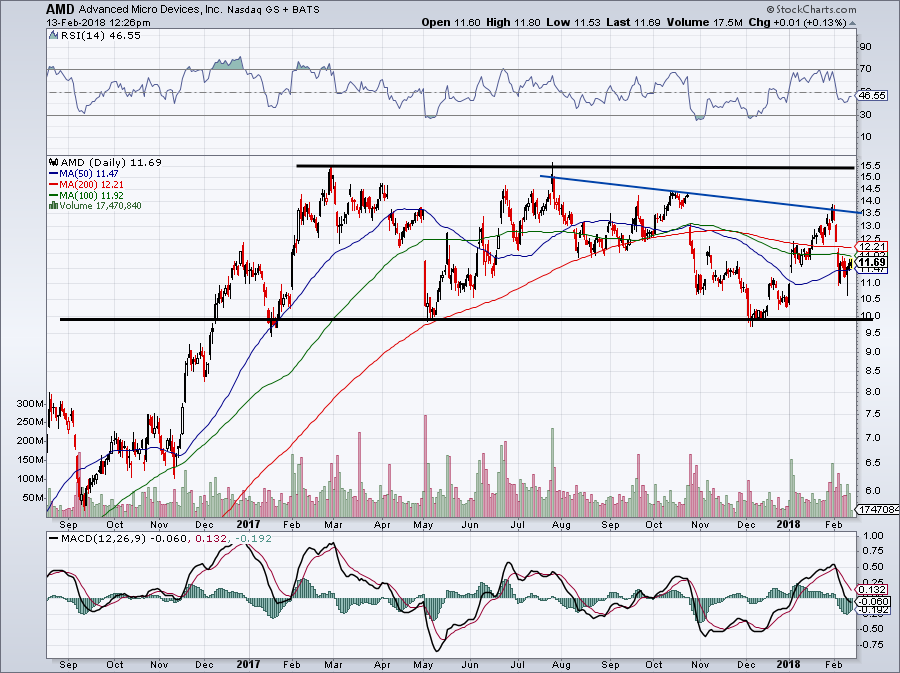

If I had a bone to pick with AMD, it would come on the charts. While it broke below $11 last week, it was only because the markets were being hammered by a strong bout of volatility. I would love for a harder drilling to occur, but perhaps that ship has sailed.

Click to Enlarge

Consolidating in the mid- to high-$11s is anything but bearish. Still, I would have loved a chance to buy AMD stock at $10. You can see long-term channel support is there, while resistance stands at $15. There is a smaller resistance trend-line (in blue) around $13.50.

Even if that comes into play, we’re still talking about 15% upside from current levels. A rally to $15 resistance is good for almost 30% upside. While a pullback toward $10 would be disappointing for longs, consider buying rather than selling.

The secular trends still favor AMD’s business.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell did not hold a position in any of the aforementioned securities.