Typically, earnings season is an opportunity to showcase how a company has improved over the last 90 days. Under the cloud of the novel coronavirus, this season is universally regarded as a mitigation centerpiece. But will Southwest Airlines (NYSE:LUV) have enough meat on the table to not convince investors to run for cover? Unfortunately, I have my doubts, which is why you should be extra careful with LUV stock.

Bluntly, if you don’t have any money to lose, don’t spend it on the markets right now, and especially don’t spend it on LUV stock. Representing one of the hardest-hit industries amid the pandemic, Southwest Airlines has multiple viability questions. Obviously, multiple state lockdowns have made traveling a tricky affair. But even if various governments didn’t get involved, you have the fact that people just don’t want to fly.

We’ll briefly go over the numbers for the upcoming first quarter of 2020, but it’s almost a pointless exercise. For earnings per share, covering analysts are forecasting a range between a loss of $1.10 up to 55 cents. Consensus comes in at a loss of 40 cents.

On the revenue front, analysts forecast between $4.1 billion to $5.3 billion, with consensus at $4.7 billion. In the year-ago quarter, top-line sales hit $5.1 billion.

Perhaps the biggest metric that everyone will focus on, though, is the company’s load factor. Last year, the load factor averaged 83.5%. Over the last three months, it averaged 83.6%. This indicates consistent profitability regarding paying customers.

But how far that load factor drops will likely determine the near-term trajectory of LUV stock. I don’t like gambling on big unknowns, which is why I’m sitting this out.

Long-Term View for LUV Stock Turbulent at Best

However, don’t take my pensiveness as a guarantee that LUV stock will tumble following earnings. Because of the devastation to the travel industry, we all know that the load factor will be terrible for Southwest, along with competitors like United Airlines (NASDAQ:UAL) and Delta Air Lines (NYSE:

DAL).

Yet if more paying passengers filled Southwest’s seats than expected, then Wall Street may interpret that as a positive sign that shares can rally due to pent-up demand. What that “magic” percentage mark is, though, is a mystery, along with the actual interpretation.

As I said, personally, I find the nearer-term picture for LUV stock has too many variables. But what about the longer-term view?

Here, I’m emphatic: you need to stay away from airliners until we understand the true nature of our post-coronavirus economy.

Click to Enlarge

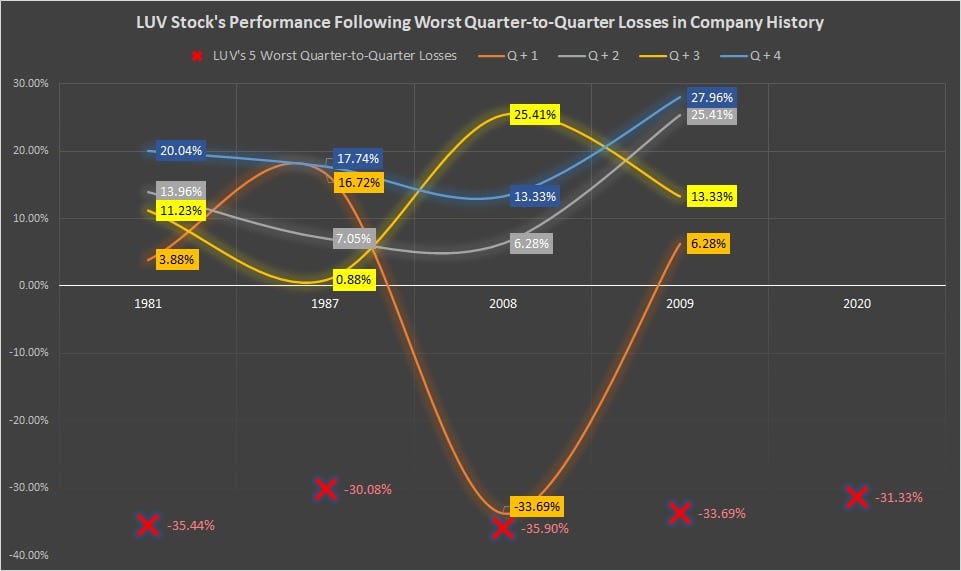

Currently, we’re on pace to suffer over a 31% loss in the second calendar quarter. And this is among the five worst performances of Southwest Airlines stock on a sequential quarter-to-quarter basis in company history.

During these awful quarters, LUV has quickly bounced back over the next four quarters. Even during the Great Recession, LUV has shown resilience.

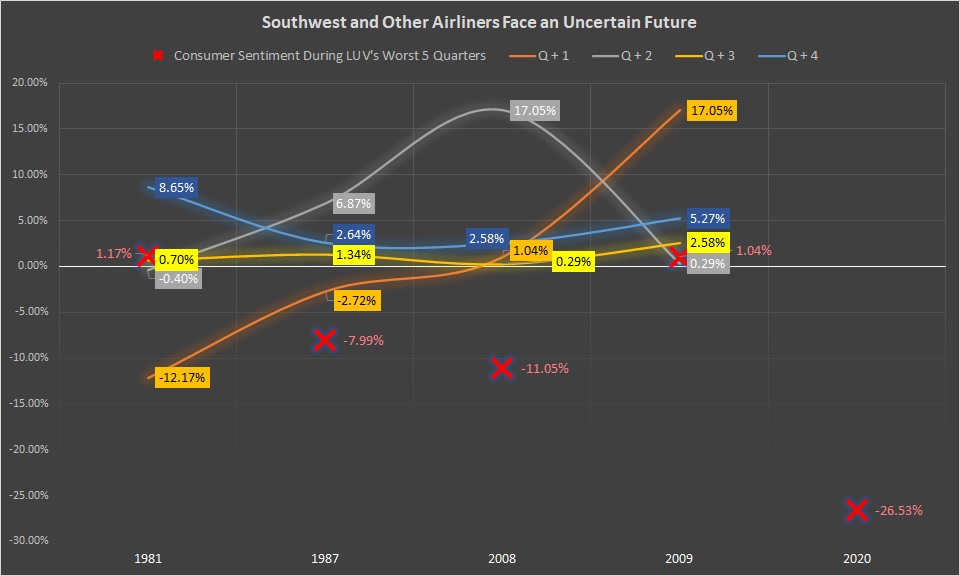

But this coronavirus-led deflation is different. That’s because during the prior four worst quarters for LUV, the quarterly loss in the consumer sentiment index averaged only 4.2%, with the worst being an 11% loss in consumer sentiment in 2008.

Click to Enlarge

At present, this index is on pace for a 26.5% loss.

The sheer magnitude of confidence loss in the consumer economy cannot be ignored. This is one of the reasons why I’m extremely skeptical about a quick recovery in the sector. Honestly, I believe that most investors have not fully appreciated the devastation we’re up against.

All Signs Point to Sell

While I would like to think that our American exceptionalism will carry us through this mess, mere patriotism doesn’t generate demand. That was the problem with the oil price war between Saudi Arabia and Russia. In the end, it was mere posturing.

You can cut supply to zero and it just wouldn’t matter. No one is buying. And that means no one is driving, flying, boating or any number of activities that involve fossil fuels.

That’s the real message behind the May contract for West Texas Intermediate dropping below zero: you couldn’t pay money to have someone take your oil. And in some way, airliners can’t pay to put passengers in their seats, not with demand cratering to health concerns.

Even without those fears, LUV stock would still be a mess. With more than 22 million Americans unemployed and many more millions to follow, who the flip is flying these days? Where would these passengers go and more importantly, why?

Until airliners can address these fundamental questions of demand, I would stay far away from this sector.

A former senior business analyst for Sony Electronics, Josh Enomoto has helped broker major contracts with Fortune Global 500 companies. Over the past several years, he has delivered unique, critical insights for the investment markets, as well as various other industries including legal, construction management, and healthcare. As of this writing, he did not hold a position in any of the aforementioned securities.