The price of oil has been slowly moving up. Oil and gas stocks are rising as well, especially those that pay dividends. The economy is slowly improving as the novel coronavirus slowly loses its strength. In addition, the prospects for an effective and widely available vaccine are improving. This has helped improve overall economic growth prospects.

I wanted to find five oil and gas stocks that can afford to pay their dividends based on expected earnings and cash flow. These five stocks have sufficient earnings and/or cash flow to maintain their present dividend, making their present dividend yield very secure.

You get the best of both economic scenarios. If the economy continues to improve, these companies will make more money over the next year, pushing up their price. Even if it takes longer than expected, these stocks pay a decent dividend yield that helps patient investors.

- Diamondback Energy (NASDAQ:FANG)

- EOG Resources (NYSE:EOG)

- Pioneer Natural Resources (NYSE:PXD)

- Cabot Oil and Gas (NYSE:COG)

- Phillips 66 (NYSE:PSX)

Let’s dive in and look at these five oil and gas stocks.

Diamondback Energy (FANG)

Market Capitalization: $7.02 billion

Click to Enlarge

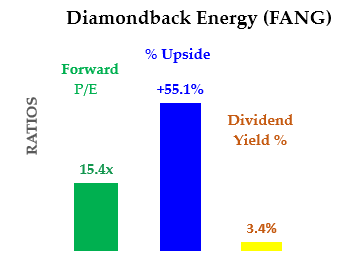

Diamondback Energy (FANG) is a Permian Basin oil and gas producer in West Texas. Unlike most oil and gas companies, Diamondback will likely make a profit this year on an adjusted basis. Since the price of oil and gas has been moving up in Q3, its earnings are likely to improve.

Seeking Alpha‘s earnings estimate for this year is $2.58 and $3.16 per share next year. This more than covers the company’s $1.50 dividend per share.

Moreover, the CEO said the company will generate free cash flow during the second half and in 2021. This assumes oil prices stay at the current level. In fact, they have started to rise.

Moreover, the CEO said the board had decided to maintain the current dividend given their current outlook.

Click to Enlarge

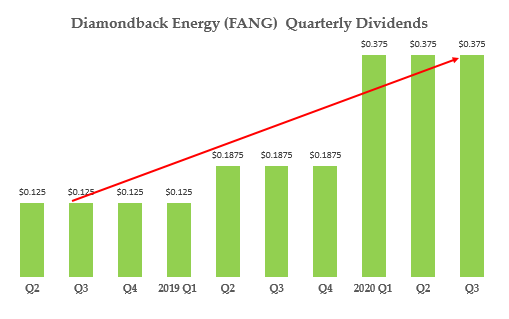

Based on this I believe that FANG stock is worth significantly more than its present price. The company has consistently paid higher dividends, as can be seen in the table at the right.

This is based on my three-fold valuation analysis method, which I have used in other articles. For example, based on its historical dividend yield of 0.5%, it’s worth five times more. Even at a yield of 2%, it is worth 65% more.

I also use a historical P/E method and a comp P/E method. Both of these show that the stock is worth 24% and 75% more respectively. On average, its target price using these three methods is $69.12. That represents a potential gain of 55% over today’s price of $44.58.

EOG Resources (EOG)

Market Capitalization: $26.8 billion

Click to Enlarge

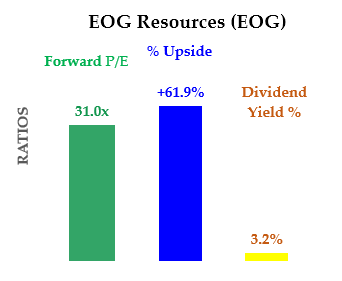

EOG is a natural gas producer along with oil in the U.S., Canada, China, the U.K., and offshore Trinidad. In 2019, total net proved natural gas reserves were 5.4 trillion cubic feet equivalent, and net proved crude oil and natural gas liquids reserves were 5,023 million barrels.

Since then things have turned down. Last quarter the company lost 23 cents per share. Analysts still expect EOG Resources to make 61 cents per share this year and $1.69 in 2021. That more than covers its $1.50 dividend per share.

During the most recent conference call, management indicated that it could cover its capex and dividend requirements with $40 oil.

Click to Enlarge

The company has already lowered its expenses and capital expenditures, as well as increased its production volume.

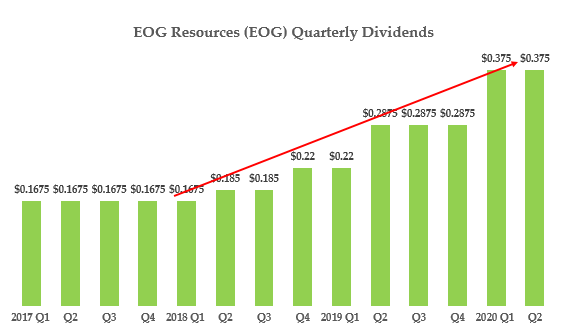

Moreover, as the table at the right shows, the company has consistently increased its dividend over time. I would expect that to continue next year.

Based on my analysis of the stock, it is worth $76.76 per share. This represents a potential gain of 62% over today’s price. This is based on my three-fold methodology of historical yield, P/E, and comp P/E ratios.

The historical dividend yield alone of 1.03%, compared to its present 3.2% yield, makes it worth over 200% more than today’s price of $47.42 per share. The average of all three methods is $76.76, a 62% upside.

Pioneer National Resources (PXD)

Market Capitalization: $17.6 billion

Click to Enlarge

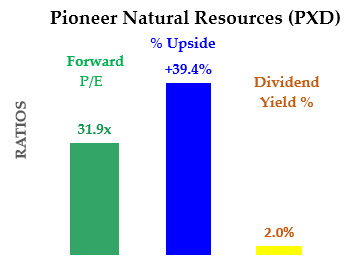

Pioneer Natural Resources is a U.S. oil and gas producer. Analysts expect the company to make $1.60 this year and $3.60 per share next year.

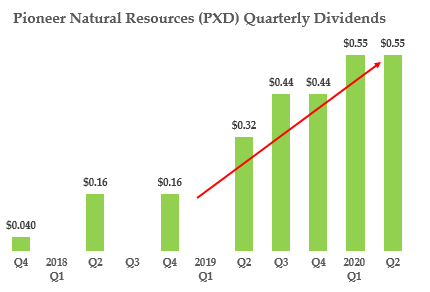

That more than covers its $2.20 per share annual dividends, paid quarterly at 55 cents per share. In fact, the company announced during its quarterly presentation that it would pay both a base dividend and a variable dividend.

The variable portion of the dividend is based on the price of oil. The first variable dividend will be paid out in 2022, based on the price of Brent oil staying above $45 in 2021. The company will not use its FCF to buy back shares, but will use that money to pay this extra dividend.

Based on my analysis, the stock is worth considerably more than its present price.

Click to Enlarge

For example, based on its historical dividend yield of 0.87%, PXD stock is undervalued compared to its present yield of about 2%. That implies a potential gain of 130%.

In addition, as the table at the right shows, the company has been consistently raising its dividend per share over the past several years.

The other portions of the company’s value are its historical P/E which is 39 times vs. its present 31 times P/E. Lastly, the company’s comps imply that it is worth 35% less than it is today.

The average of all three of the methods shows that PXD stock is worth $153.26 per share, or 39% more than the present price of $109.94.

Cabot Oil and Gas (COG)

Market Capitalization: $8 billion

Click to Enlarge

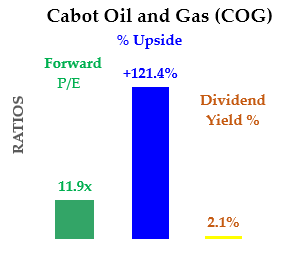

Cabot Oil and Gas produces oil and gas primarily in Appalachia, east and south Texas, and Oklahoma. Analysts forecast that the company will make 54 cents per share this year and $1.63 per share next year.

That puts the stock on a very cheap 12 times earnings multiple for next year. Moreover, this earnings level also more than covers its quarterly 10 cents per share dividend (40 cents annually).

It also gives COG stock a 2% dividend yield. This is significantly higher than its historical 1.08% dividend yield over the past four years, as calculated by Seeking Alpha. That alone represents a potential upside for COG stock of 91%.

The company indicated in its recent conference call that it fully expects to cover both its capex program and its dividend with expected 2020 cash flow.

Moreover, Cabot Oil and Gas has consistently paid its quarterly dividend, as the table at the right shows.

Click to Enlarge

In addition, the company said it would consider paying special dividends and/or buying back stock. These are additional ways management said it will return capital to shareholders.

Based on my analysis, COG stock is worth 121% more than the present price. My target price is $42.84 per share, compared to its present price of $19.35.

Even if it takes three years for that to occur, it would represent a compound average annual return of 30.2%. That is a significant ROI for most investors.

Phillips 66 (PSX)

Market Capitalization: $27.3 billion

Click to Enlarge

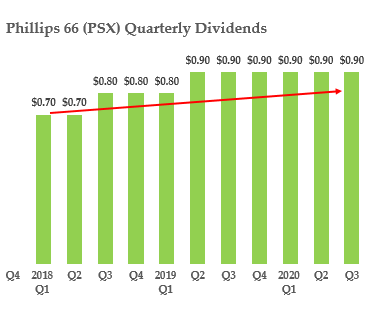

Phillips 66 is a downstream and midstream company that owns or has stakes in 13 refineries. It was spun off from ConocoPhillips to its shareholders in April 2012. Right now the company pays a 90 cents quarterly dividend, or $3.60 per share annually. At today’s price of $62.63 per share, PSX stock has an ample 5.75% dividend yield.

This high yield is more than covered by the company’s expected earnings by next year. For example, analysts expect it to make $1.10 this year and $5.10 per share in 2021.

The company made a point in its conference call to state that its operating cash flow of $764 million and returned $394 million to shareholders through dividends.

Phillips 66 management said its second half capex spending will be “significantly less” than in its first half. It implied that through this measure and $2 billion in senior notes that it issued, that both the dividend and its buyback program will be affordable.

The company has consistently paid its quarterly dividend, as can be seen in the table at the right. However, it has also not raised the dividend in six quarters.

Based on my valuation method, I believe PSX stock is worth over double its present price. For example, its historical dividend yield has been 3.25%, rather than its present 5.75%. That implies that the stock is worth 75% more.

The average of all three valuation methods derives a target price of $128.47. This represents a gain of 105% over today’s price of $62.63 per share. Over three years that would be a 27% average annual return.

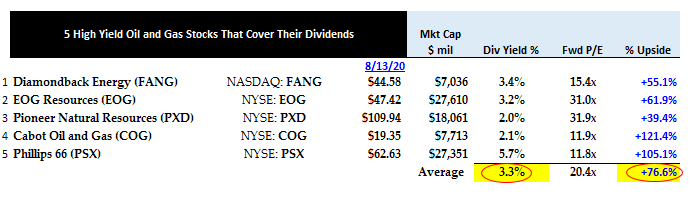

Summary of Oil and Gas Stocks That Can Afford Their Dividends

The table below shows that the summary of these five oil and gas stocks results in an average 3.3% dividend yield and an average 20 times forward earnings.

Click to Enlarge

Moreover, these stocks have an average upside of 76% potential upside. There is no time frame under which I assume the oil and gas stocks will rise to these target prices.

But, on average, if it took three years, the annual return would be 20.9% annually. If you include the annual yield and assume that the dividends per share rise, the total return would be over 24% annually. That would be a quite a sufficient ROI for most investors of oil and gas stocks.

As of this writing, Mark Hake, CFA does not hold a position in any of the aforementioned securities. He runs the Total Yield Value Guide which you can review here.