Earnings season is upon us once more!

The big banks kicked off the season this morning with JPMorgan Chase & Co.’s (JPM), Wells Fargo Company’s (WFC) and Citigroup Inc.’s (C) first-quarter results. And Bank of America Corporation (BAC) will join the mix on Tuesday.

Now, longtime readers know that while I do look forward to every earnings season, I’m not a big fan of the “big banks”. That’s because I am an ex-banking regulator and I know they sometimes play fast and loose with their numbers.

Back in the late 1970s and early 1980s, when the yield curve was severely inverted, I used to merge two money-losing financial institutions together so they could qualify for FSLIC or FDIC insurance. Essentially, I would take the largest financial institution and merge it into the smaller one, but would re-amortize its assets (e.g., loan portfolio) to make the combined financial institution look better.

Even though I could never fix the combined financial institution’s cash flow, I helped them kick the can down the road, since an inverted yield curve is lethal for banks. In other words, I used to put lipstick on a pig. My experience scarred me for life, which is why I rarely recommend banks.

But with the big banks’ having reported first-quarter earnings this morning, I’d like to use today’s Market 360 to review their earnings numbers as well as preview what to expect from Bank of America. I’ll also share what my Portfolio Grader says about the big banks, and then I’ll tell you whether I personally think they are good buys right now. I’ll also reveal how you can find the market’s next big winners…

Reviewing the Big Banks Reports

Citigroup (C)

Citigroup beat analysts’ expectations on the top and bottom lines. For the first quarter, the bank reported earnings of $1.58 per share on revenue of $21.1 billion. This compares to earnings of $2.19 per share on revenue of $21.4 billion in the first quarter of 2023. The analyst community anticipated earnings of $1.20 per share on revenue of $20.39 billion, so Citigroup bested earnings estimates by 31.7% and revenue estimates by 3.5%.

Most important to note, however, is the growth driven by Investment Banking and Corporate Lending. Citigroup reported banking revenues of $1.7 billion, a 41.6% increase from $1.2 billion in the first quarter 2023. Investment Banking accounted for $903 million revenue, a 35% from the same quarter a year prior.

JPMorgan Chase (JPM)

For the first quarter 2024, JPM Chase posted earnings of $4.44 per share, up 8.3% from earnings of $4.10 per share a year ago. Analysts were calling for earnings of $4.15 per share, so JPM posted a 16.8% earnings miss. Revenue of $41.9 billion topped analysts’ estimates for $41.84 billion. This is up 9.4% from revenue of $38.3 billion reported in the same quarter of last year.

I should also add that shares of JPM dropped more than 5% after giving disappointing guidance on 2024 interest income. Full-year 2024 net interest income is expected to be around $90 billion, which is essentially unchanged from the previous year.

Wells Fargo (WFC)

Wells Fargo posted solid earnings for its first quarter in fiscal year 2024. Earnings of $1.20 per share beat analyst estimates for $1.09 per share. That’s an earnings beat of 10.1%. Revenue increased slightly year-over-year to $20.86 billion, compared to analysts’ expectations of $20.2 billion in revenue. So, the bank posted a 5.1% surprise. Net income of $4.6 billion slipped nearly 8% year-over-year from net income of $5.0 billion in the same quarter of last year.

Now, net interest income did slip by 8% for the quarter. Net interest income came in at $12.2 billion, compared to $13.3 billion in the same quarter a year prior. The company noted this decrease was due “to the impact of higher interest rates on funding costs, including the impact of customer migration to higher yielding deposit products, as well as lower loan balances, partially offset by higher yields on earning assets.”

Bank of America (BAC)

Now, looking ahead to Bank of America, it looks like it could be a mixed bag of results. Analysts forecast BAC to post earnings of $0.77 per share on revenue of $25.46 billion. This is down from earnings of $0.94 per share and up from revenue of $26.3 billion in the same quarter a year prior. That translates to an 18.1% year-over-year earnings decline and a 3.2% year-over-year revenue decline. Earnings estimates have fluctuated over the past three months.

Are the Banks a Buy After Earnings?

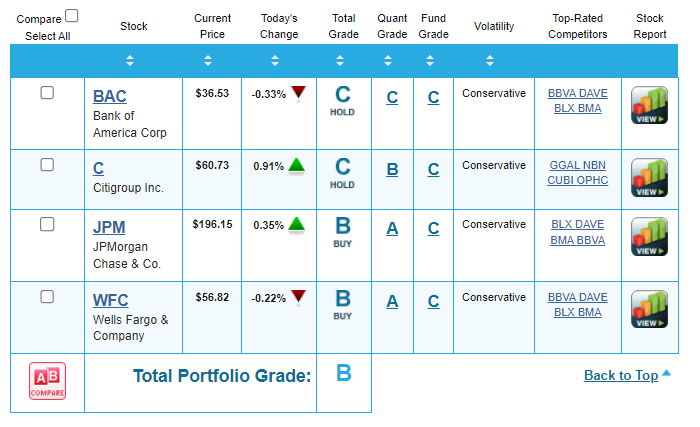

Now, let’s take a look at what my Portfolio Grader tool has to say for these stocks:

According to Portfolio Grader, Citigroup and Bank of America both receive a Total Grade of “C.” That makes them a “Hold.” JP Morgan Chase and Wells Fargo, on the other hand, receive a Total Grade of “B,” making them a “Buy.”

Now, would I personally recommend buying any of these stocks?

In a word: No.

While the banks may post strong earnings, the inverted yield curve will remain a problem for them.

An inverted yield curve occurs when short-term interest rates rise above long-term rates. This can happen when investors anticipate an economic slowdown or a recession. Investors seek safety by buying bonds with a longer duration, which pushes their yields down. Eventually, enough buying pressure occurs that the longer-duration bonds yield less than those with a shorter duration.

In simple terms, banks hope to earn a higher rate of return from lending activities, so they need higher long-term rates. An inverted yield curve squeezes banks’ net interest margins because they earn less from their lending activities.

It is also important to note that net interest income is a critical measure for many banks. It measures the difference between what banks earn on their assets and pay out on their deposits. All three banks reported a drop in net interest income from the fourth quarter to the first quarter. It was down 4% at JPMorgan, 4% at Wells Fargo, and 2% at Citigroup.

The Market’s Next Game-Changing Trend…

Instead, I think the best bet for your money remains in fundamentally superior stocks that are poised for growth in any market environment.

These are the kinds of investments we look for every day at Growth Investor. And it’s also why I just gave a special presentation about the next disruptive wave of innovation that’s set to change the world…

Just recently, engineers at Google fed a math problem into a new type of computer. This problem is so complex that it would take the world’s best supercomputer 10,000 years to solve. But this new computer figured it out in less than four minutes.

The implications of this breakthrough are massive. Very soon, a flood of investment is going to pour into this corner of the market as companies scramble to gain access to this technology.

And I’ve found one tiny company that’s set to bring this revolutionary approach to computing to the masses.

Some experts predict it could be the next NVIDIA Corporation (NVDA). That’s because in the same way NVIDIA’s chips provided the backbone for A.I., this tiny Maryland company is going to provide the backbone for something called “QaaS.”

Now, over at Growth Investor, we’ve had NVDA in our High-Growth Buy List since May 2019. And since then, we’re sitting on a gain of nearly 2,000% – and I think we’ll see a lot more when it’s all said and done.

Get the details on this innovative technology – and how it could impact your portfolio – here.

(Already a Growth Investor subscriber? Click here to log in to the members-only website now.)

Sincerely,

Louis Navellier

Editor, Market 360

P.S. A quiet move was just made in Washington, D.C. that even the most in-the-know money managers, investors and political pundits probably aren’t aware of…

And it’s all coming to a head on May 1st – a critical date that could cause stock market chaos for everyday investors and even potentially change the course of this election cycle.

That’s why I recently sat down to deliver an urgent warning to investors in my critical election shock summit. Go here to view it now…

The Editor hereby discloses that as of the date of this email, the Editor, directly or indirectly, owns the following securities that are the subject of the commentary, analysis, opinions, advice, or recommendations in, or which are otherwise mentioned in, the essay set forth below:

NVIDIA Corporation (NVDA)