If you cover hundreds of publicly traded companies over the years, you’re bound to get some wrong. That’s just the nature of the beast. I’m learning that lesson the hard way with Alibaba Group Holding Ltd (NYSE:BABA). Year-to-date, BABA stock earned its status as one of the hottest tickets on Wall Street, gaining a meteoric 56%.

To top it off, shares closed up more than 13% last Thursday when Alibaba announced an exceptionally optimistic forecast.

As InvestorPlace contributor Dana Blankenhorn wrote, the Chinese giant “surprised analysts at its investor day by predicting revenue growth of 45%-49% this year, implying total revenues of $34.3 billion.”

I’m sure, though, that analysts weren’t that surprised. The consensus for BABA stock is extremely bullish. According to Yahoo Finance, 17 pegged Alibaba as a “strong buy,” while 21 analysts see it as a standard “buy.” That leaves two other analysts of the 40 that cover BABA, and they’re on the sidelines. At the risk of triggering a “Captain Obvious” joke, no one is bearish.

With overwhelming support for BABA stock, does this cause me to change my mind? It does, but only with a heavy caveat. I believe that those who buy Alibaba shares now are gambling against the fundamentals. They’re hoping that there will be enough bag-holders before these fundamentals close the door.

Ignoring Challenges Surrounding BABA stock

When I hear market commentators discuss Alibaba stock, I’m left wondering why few, if any, ask basic questions.

The first question, in my opinion, is fairly obvious — isn’t Alibaba a perfect candidate for a contrarian trade? The company soared to all-time highs completely based on the company’s own words. It hasn’t had a noticeable correction since December of last year. Finally, the biggest red flag is the fact that nobody is hitting the sell button.

The second question should be more obvious, but it’s not. China is a communist country. Communists are shady. So why are we giving out a “capitalist pass” to Alibaba?

InvestorPlace contributor Lawrence Meyers really hit home the concerns that American investors should have, but are refusing to acknowledge. Financial scandals have recently impacted Chinese companies, including Alibaba. More worrisome to me is the accusation that the Chinese government may have “overcooked” their GDP figures by as much as a 20% margin.

I’m not sure why this isn’t bothering more analysts. GDP growth represents one of the key arguments favoring BABA stock. The idea is that companies like Amazon.com, Inc. (NASDAQ:AMZN) or

Apple Inc. (NASDAQ:AAPL) are centered in the saturated and stagnant U.S. market. In contrast, China’s booming growth and massive workforce will launch not only BABA, but regional competitors like Baidu Inc (ADR) (NASDAQ:BIDU) and JD.Com Inc(ADR) (NASDAQ:JD).

I admit that it’s a strong thesis, but only if the supporting data is accurate. Although he may have received a lot of flak for it, I appreciate Mr. Meyers’ pointed words. He stated that “Fraud is simply a way of life in China, and that is the primary reason I have no interest in Alibaba.”

The Broader Fundamentals Make No Sense

Finally, I have a third question. For a country that is obsessed with “fake news,” why aren’t we prodding BABA’s recent guidance? Specifically, I would like to know what justifies this sudden burst of enthusiasm.

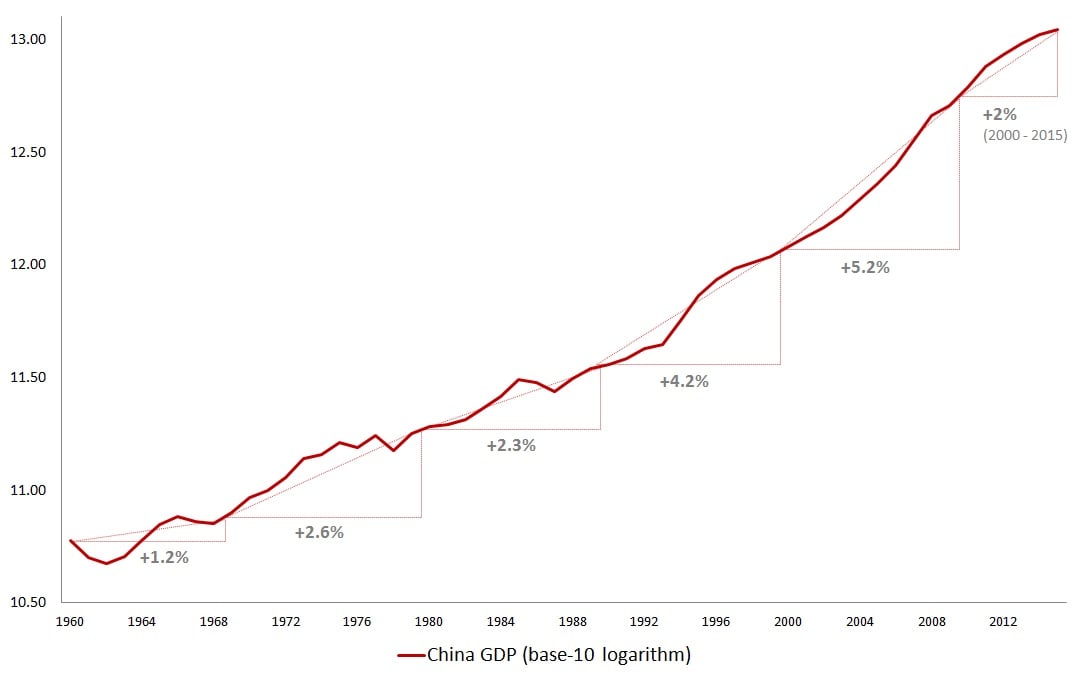

A cursory look at China’s GDP confirms that the economy is steadily slowing.

Click to Enlarge

Visually, you can see that the best years for China was during the 1990s and 2000s. In the current decade, Chinese GDP is stabilizing. Some may argue that it’s maturing, similar to the S-curve theory.

Whatever the case may be, the GDP figure needs to expand, and quite dramatically. China has four-times our population. If Alibaba wants to compete with Amazon on level terms, the country needs to have four-times our economy.

That’s not going to happen. Despite the numerical advantage, Chinese GDP per capita is well off our own and those from developed nations. An earth-shattering paradigm shift would need to occur before the company’s ambitious goals are realized.

Until then, I’m staying on the sidelines. I can still grow to like BABA stock, but I’m definitely not going to pay a premium for it. The fundamentals just don’t justify extreme exuberance.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.