When Advanced Micro Devices, Inc. (NASDAQ:AMD) beat earnings and revenue estimates in late July, a lot of investors were expecting a rally. It did rally, but only for one day — literally. After hitting new 52-week highs in the next session, AMD stock suddenly hit reverse and is down almost 20% since.

So, what should investors do with AMD?

The company has strong fundamentals (more on that in a second), but AMD stock looks even better as a trade candidate.

Trading AMD Stock

Click to Enlarge

So what exactly makes AMD a buy right here? Let’s turn to the charts.

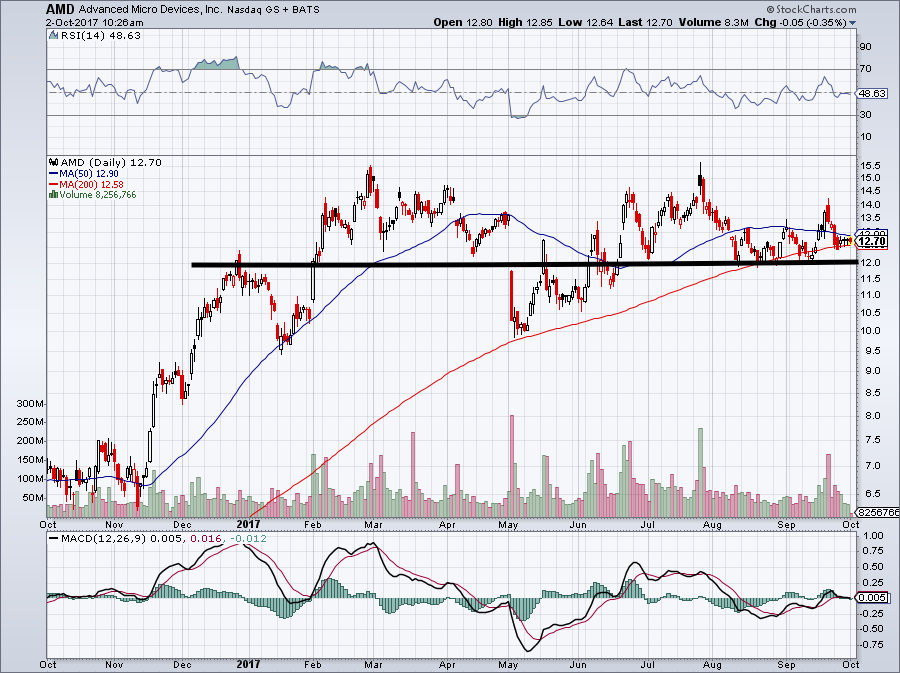

After its post-earnings boom and bust, AMD stock has been trading in a relatively tight range, particularly over the past two months.

Looking at the chart, $12 has been an important level over the last year or so. It’s been both support and resistance, most recently serving as the former. There’s also the 200-day moving average just below the current price of $12.75 (as of Friday’s close). That has held up as support to some degree as well.

So, what’s the trade?

I advocate buying shares near current levels and using a stop-loss just below the 200-day moving average or the $12 level. Each has pros and cons. A 200-day moving average stop-loss minimizes losses, but could also trigger on even the smallest of dips. This could push traders out of the trade too early.

Setting the stop-loss below $12, on the other hand, allows for losses of about 6.3% — larger than some investors may be comfortable with. On the plus side, though, this level has held up well in the past (at least on a closing stock price basis) and allows investors the chance to stay long for a higher rebound.

On the upside, I’m targeting $14, where AMD stock fell sharply just a few trading sessions ago. Shares temporarily jumped to these levels after news regarding its new infotainment business with Tesla Inc (NASDAQ:TSLA).

Target #2 is $15.50, which has offered stiff resistance in 2017. We have about 6% downside on a stop-loss. There’s more than 10% upside for target #1 and more than 22% upside should we hit target #2. Not bad.

What About Investing in AMD?

Investors can use the same principals as the trader. No one likes to lose 20%, 30% or more of their money, even if the fundamentals story is good.

Last quarter, the company had its first positive operating income since the fourth quarter of calendar year 2014. Its total debt stands at $1.375 billion, down over 30% from where it stood just 18 months prior at year-end 2015. Operating cash flow (OCF) was positive at year-end 2016, standing at $90 million, its best result since 2013. While OCF is negative year-to-date, that’s typical for AMD’s seasonality. It should make up ground in this regard in the second half.

Sorry for the numbers blitz here; what I’m basically getting at is that AMD is doing much better!

Going forward, analysts expect AMD’s momentum to continue. Forecasts call for 18.1% sales growth this year and another 12.3% in fiscal 2018. Given that AMD has only missed revenue estimates once in two years, perhaps these estimates aren’t high enough. Earnings estimates call for 170% growth this year and 210% growth next year.

Gross margins have been declining over the years, as AMD has had to resort to being price competitive. This has driven market share and revenue higher at the expense of margins. However, with its new high-end Vega lineup

, the hope is that margins will expand going forward. That’s one catalyst fueling earnings growth, despite just modest revenue growth.

Final Thoughts on AMD

Is Advanced Micro Devices perfect? Of course not. AMD stock trades at 41 times forward earnings estimates, so it’s certainly not a “cheap” stock by classic measures.

However, we tackled this issue in the past. On a sales basis, AMD is cheaper than Intel Corporation (NYSE:INTC) and vastly cheaper than Nvidia Corporation (NASDAQ:NVDA).

This doesn’t mean the industry is cheap, but at least AMD isn’t the most expensive. It should continue taking market share and boosting its operating results. That’s good news for investors. AMD stock has a compelling risk/reward profile, allowing investors and traders to partake in solid upside while limiting their downside.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell held long bull call spreads in NVDA.