By the time you read this, oil services outfit Schlumberger Limited. (NYSE:SLB) may have already posted fourth quarter numbers. Likewise, SLB stock is apt to be moving in a big way — for better or worse — in response to the highly anticipated announcement.

Today’s expected report come as oil prices have rallied 50% since June and the current WTI price just shy of $64 per barrel. Translation: The oil business is profitable again for most players.

Before jumping to any conclusions — good or bad — it may be worth digesting the idea that the Q4 numbers from Schlumberger will still tell us very little about the company’s likely future.

The good news is that future looks bright IF explorers and producers don’t make the same mistake they made in 2007 and again in 2013.

Hesitant Explorers?

The short version of a long story: The oil and gas industry isn’t all that disciplined. When crude prices rise, explorers tend to get overzealous, establishing production capacity that leads to a glut.

In their defense, it’s a tricky business. It can take months between deciding to establish a new well, or rig, and beginning production of oil that goes to refineries. If too many explorers are doing that at the same time — calling on names like Halliburton Company (NYSE:HAL) and SLB to help do so — the end result is a huge supply of oil we can’t use.

This happened in 2014, when oil prices held above $100 per barrel for more than two years. Assuming (erroneously) that was the new norm, producers went into overdrive. By 2015 we were sitting on a then-record-breaking stockpile of crude we couldn’t burn fast enough.

The takeaway: They never saw it coming.

The reactionary slowdown in exploration and production, in the meantime, has been brutal for oil services players. SLB stock is down almost 30% from its mid-2014 peak, even with the 22% gain from November 2017 lows. Schlumberger stock is hardly unique in that regard, though.

But are things different now? Indeed they are.

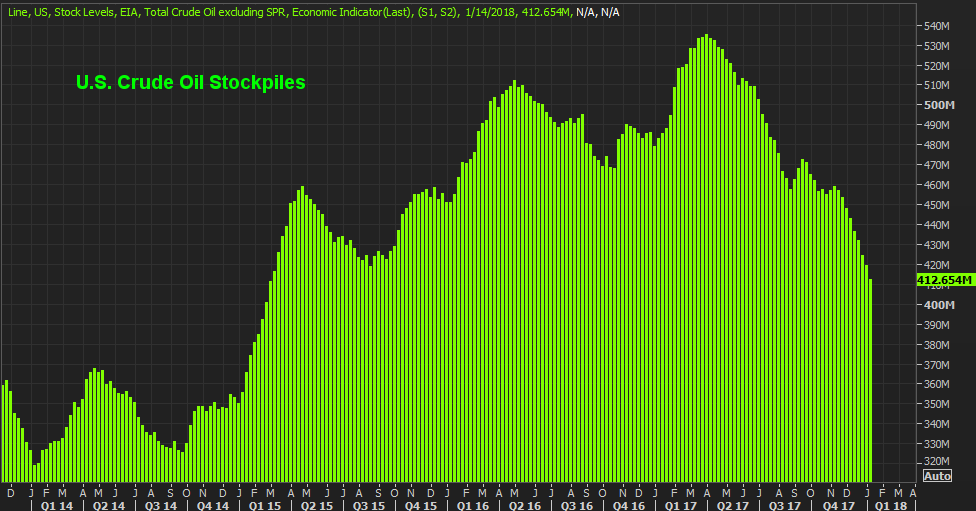

On Thursday, the Energy Information Administration reported the nation’s stockpile of oil fell another 6.9 million barrels last week. At 413 million barrels, America’s stockpile is down 22% from last April, and it’s still in a steep downtrend. That’s against a backdrop of crude prices at multi-year highs, and superficially speaking is bullish for all energy stocks.

We’ve seen this sort of situation before, however… in 2007 and 2014. Both times it ended badly, with oil prices being crushed.

Click to Enlarge

Granted, we’re nowhere near the extremes we were at then. Then, WTI crude prices were in excess of $100 per barrel. And, the nation’s stockpiles have never fallen as fast for as long as they’re falling now. Even OPEC is sticking with its plans to curb global supplies by keeping a lid on the cartel’s output. That translates into a tight, and tightening, supply.

Click to Enlarge

Just bear in mind the lag time between rising (or falling) oil prices and the decision to ramp-up (or reel-in) production in the past. The industry’s explorers and producers certainly are, and they may still be hesitant to make the same mistake a third time in just a little over a decade. Instead, they seem to be keeping something of a lid on making major investments in their capacity, fearing falling into the same trap they fell into in 2014 and as far back as 2007.

The Bull Case for Oil Production

That’s the pessimistic point of view anyway. Not everyone sees the same risk… at least not right away.

Evercore ISI analyst James West is one of the optimists. He recently noted “The international and offshore markets are awakening. We continue to believe the large-cap diversified service providers will prove to be the structural winners this cycle.”

Susquehanna Financial Group analyst Charles Minervino believes global drilling activity could rise on the order of 7% this year. Minervino went on to explain “Many U.S. services companies have put more pressure pumping fleets back to work, hired personnel and gotten past the startup costs to make 2018 a very profitable year in oilfield services.”

Both outlooks bode well for SLB stock, though the benefits of such an improvement aren’t likely to show up in the numbers just yet.

Spending related to capacity expansion took a toll on Schlumberger’s bottom line early last year. Yet, as Bloomberg’s David Wethe pointed out yesterday, explorers weren’t exactly chomping at the bit to tap into Schlumberger’s or Halliburton’s rebuilt capacities during the second half of 2017… despite the soaring price of oil. It’s a tacit hint the industry is gun-shy, having learned from the past about the pitfalls of overproduction, and how quickly the industry can get in over its head without anyone realizing it.

Bottom Line for SLB Stock

Here’s the rub for current and would-be owners of SLB stock: On one hand oil prices are on the rise while inventory levels are dropping. On the other, drillers and explorers — still licking their wounds from the 2014/2015 implosion — either can’t or just won’t make major investments in their infrastructure. If we’re at the “as good as it gets” level for this cycle, that’s a problem simply because where Schlumberger is isn’t all that compelling, from a fiscal perspective.

Today’s report should be a relatively strong one, to be clear. Take it with a grain of salt, though. It’s a comparison to the last quarter of 2016, when most of the E&P sliver of the energy sector had doubts that the budding rebound in oil prices would last. Though capital outlays have modestly improved in the meantime, benefiting Schlumberger, it’s not clear if explorers or drillers are committed to spending a lot more in 2018 than they did in 2017.

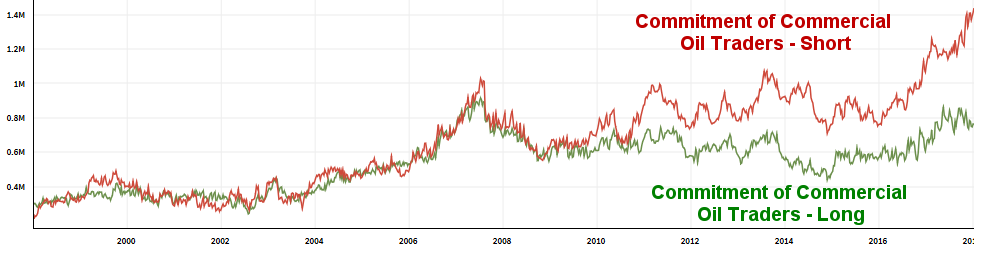

And for what it’s worth, commercial oil traders who use oil futures not to speculate but to hedge against volatility and wild price have never held as many short/bearish positions on crude as they do now.

They’re also suspiciously not sitting on a lot of bullish positions. With much more at stake than the average trader, and access to a wealth of data on the matter, all investors would be wise to wonder that that set of professionals knows that you don’t.

Click to Enlarge

This morning’s report might shed some light on the situation; Just consider the source. This matter has been far from decided.

As of this writing, James Brumley did not hold a position in any of the aforementioned securities. You can follow him on Twitter, at @jbrumley.