The stock market has been on a tear lately, but not all stocks are sharing in the gains. A handful of industries and outlier companies are driving the broader market rally, while many other stocks have been left behind. Wall Street has severely punished some for failing to deliver this year, resulting in a few unfairly hated stocks.

I see this as an opportunity. Stocks that are hated and trading at a discount today could be poised for a major rebound in the coming economic cycles. I believe in buying companies with staying power and long-term profitability when their shares are weak and holding them for the long run. They rarely disappoint.

The upside case is even more compelling when stocks get so depressed that the potential downside risk becomes quite limited compared to the possible upside. The stocks I will discuss today fit this profile. I think they are so beaten down that things can only get better. And if the next few quarters go right for these companies, I expect their shares could deliver oversized returns. Let’s dive in!

Pfizer (PFE)

Pfizer (NYSE:PFE) has been on a rollercoaster ride, but I believe the company is turning a corner. While saying Pfizer is among hated stocks would be an understatement due to the politicization of its COVID-19 vaccines, I see promise in the company’s pivot to other areas. Pfizer’s Q1 earnings beat expectations, with revenue of $14.88 billion surpassing estimates.

The stock surged 4% on the strong results. Analysts at Truist maintain a buy rating with a $36 price target, citing Pfizer’s new drug development. I’m optimistic about tailwinds like the company’s expansion in India to support medical innovation and progress with its once-daily weight loss pill.

With the stock bouncing off the $26 level, I believe it has found a bottom and could climb higher. Cost-cutting efforts are on track, and the company has raised its full-year profit outlook. While challenges remain as Pfizer recovers from the COVID-19 decline, I see the potential for this pharmaceutical giant to regain its footing and deliver for investors. It also has a 6.6% dividend yield to sweeten the deal.

Walt Disney (DIS)

Walt Disney (NYSE:DIS) has struggled in recent years to recapture its former magic, but the stunning success of Inside Out 2 could mark a turning point. I believe the naysayers who claim most media companies have lost their spark are right in many ways. Disney is more than just a media company; its global cultural influence has waned, and blockbuster hits have become scarce.

That all changed with the release of Inside Out 2. It has shattered box office records by becoming the first movie of 2024 to surpass $1 billion globally in just 19 days. This animated sequel is already the highest-grossing film of the year. Perhaps Disney’s Pixar studio can still deliver compelling stories that resonate with audiences worldwide.

I’m optimistic that Inside Out 2’s triumph and Disney’s ambitious plans to invest $60 billion in expanding its theme parks and cruise lines over the next decade could reinvigorate the company’s growth. Disney already exceeded expectations in Q2 2024 with adjusted earnings per share up 30% year-over-year and a raised full-year EPS growth target of 25%.

Many analysts now rate Disney stock as a strong buy due to its long-term potential, and Inside Out 2 could signal the start of a sustained recovery for this entertainment giant.

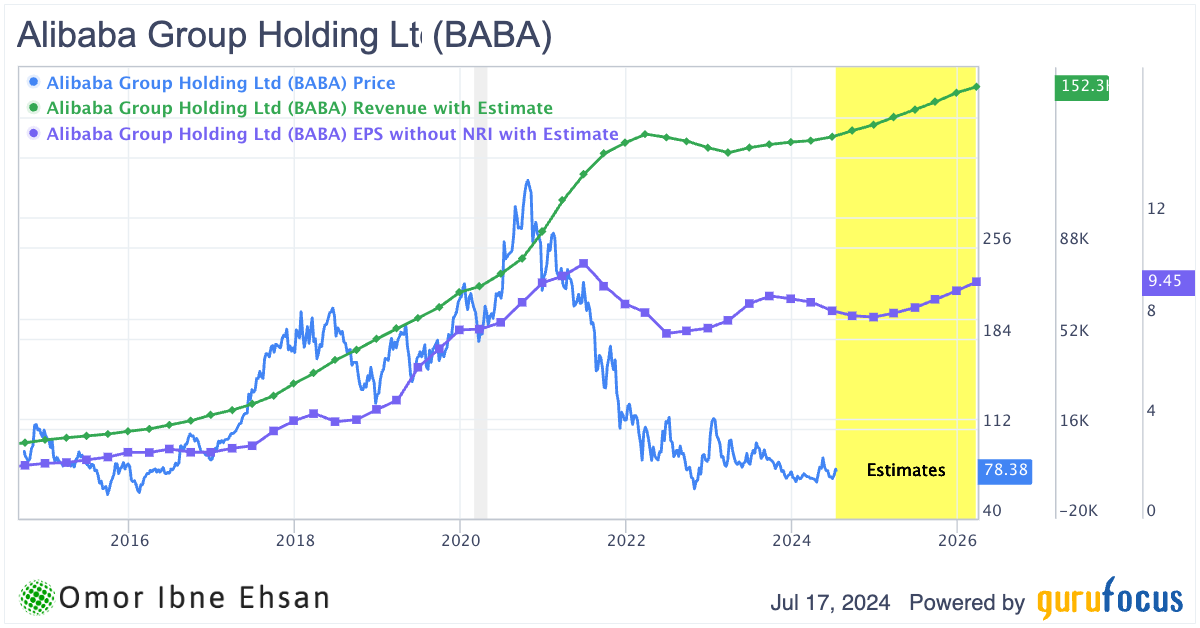

Alibaba (BABA)

Alibaba (NYSE:BABA) has faced challenges in recent years that have disappointed investors and weighed on its stock price. I believe this is largely due to the broader underperformance of the Chinese economy, which has struggled to stage a robust recovery and satisfy equity markets. However, I remain optimistic about Alibaba’s long-term prospects as the company shifts its focus to high-growth segments like cloud computing and artificial intelligence.

The Chinese government has recognized the need to stimulate economic growth, with calls for interest rate cuts on the horizon. This could provide a much-needed boost to consumer spending and benefit Alibaba’s core e-commerce business. Moreover, I see a growing preference among Chinese consumers for domestic companies, a trend that is likely to impact large enterprises in China when choosing cloud service providers. Alibaba’s cloud and AI offerings are well-positioned to capitalize on this sentiment and drive renewed growth. An expected rebound in trailing earnings could also be the catalyst that sends BABA stock higher.

Click to Enlarge

Despite a modest 5% year-to-date gain, I believe Alibaba’s stock has the potential for a significant recovery if the company continues to exceed revenue expectations. In its most recent quarterly earnings report, Alibaba surprised top-line estimates by about 1%. This could be a sign of more to come.

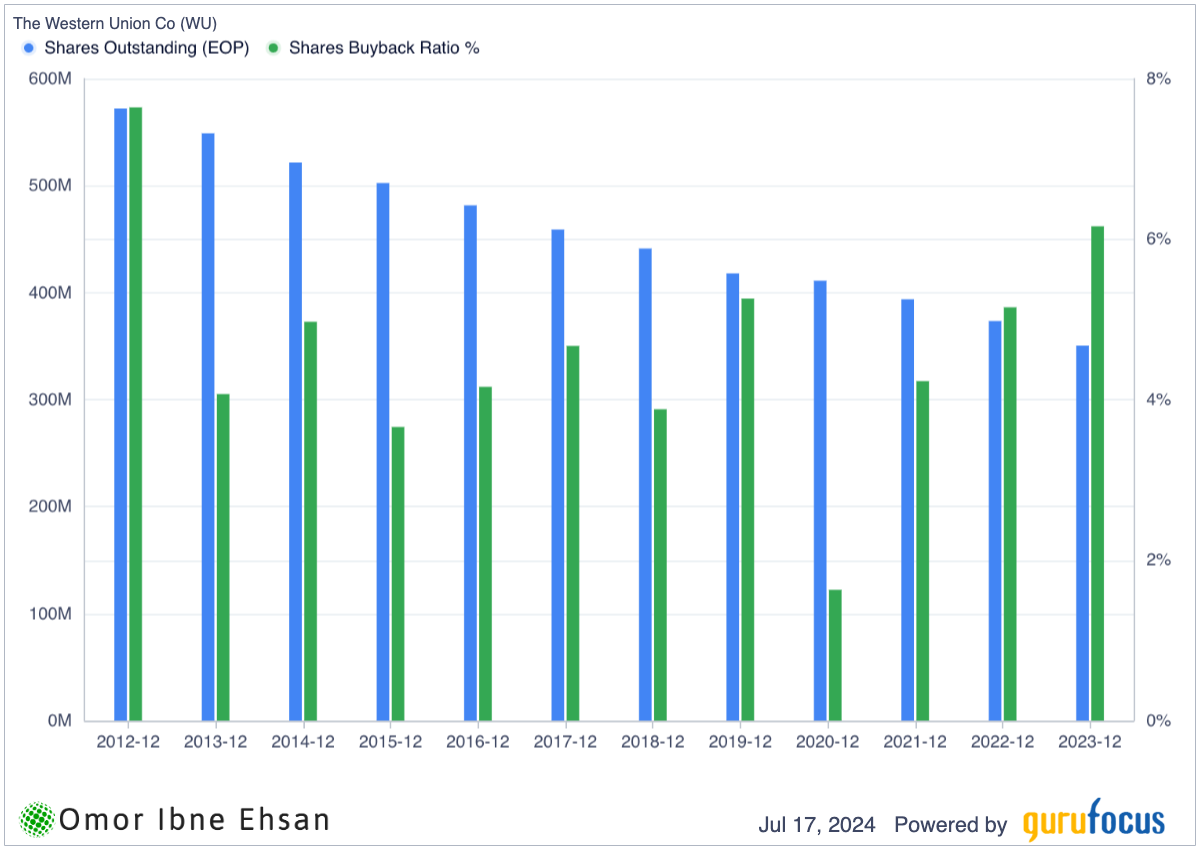

Western Union (WU)

Western Union (NYSE:WU) has struggled in the post-pandemic era, with its stock down 54% from the pre-pandemic peak. I believe the company could see a significant recovery in the long run as transaction volumes rise following anticipated interest rate cuts. Western Union reported Q1 2024 revenue of $1.05 billion, up 3% year-over-year on an adjusted basis, with branded digital transactions growing an impressive 13%.

The company is profitable but is saddled with $2.54 billion in debt that carries high-interest expenses in the current rate environment. Moreover, increased migration into the U.S. has not yet translated into meaningfully improved financial results for Western Union. However, I expect we’ll see a sustained recovery take hold once the Federal Reserve pivots to rate cuts, likely within the next few quarters.

Meanwhile, investors can collect a hefty 7.46% dividend yield while waiting for the turnaround to play out. The buyback record is also one of the best I’ve seen so far.

Click to Enlarge

Of the eight analysts covering the stock, none have a buy rating – but I think they’ll turn more positive as fundamentals improve.

Intel (INTC)

Intel (NASDAQ:INTC) has been struggling to keep up with its competitors in the semiconductor industry, missing out on the recent rally and seeing its stock price remain stagnant over the past year. I believe this presents a good buying opportunity for long-term investors, as the current pessimism surrounding the company seems excessive. Intel’s financials are improving, with revenue growth turning positive and profitability on the horizon.

The chipmaker is also making significant investments in AI chips and has managed to defend its CPU market share against AMD’s (NASDAQ:AMD) advances. If Intel can maintain its execution, I think the stock has a good chance of recovering. There’s also a possibility that if the AI hype cools down and startups face funding challenges, they may turn to Intel for more affordable AI chip solutions.

The road ahead isn’t easy, but I believe Intel’s recent progress in key growth areas like AI positions it well for a comeback in the next four quarters.

Lithium Americas (LAC)

Lithium Americas (NYSE:LAC) has been making steady progress on its Thacker Pass project in Nevada despite a challenging market environment for lithium in recent quarters. Just a couple of years ago, lithium was one of the most hyped commodities, but prices have crashed as EV demand slowed and automakers focused more on hybrids than pure electrics.

However, I don’t think it’s all doom and gloom for Lithium Americas. The company reported it had $147 million in cash at the end of Q1 2024 and subsequently raised another $263 million. It also received a conditional $2.26 billion loan commitment from the U.S. Department of Energy. Analysts still have an average price target of $6.2 on the stock, well above current levels around $3.

If interest rates come down fast, EV sales could rebound, perhaps not to boom-time highs but enough to lift lithium prices and stocks like LAC.

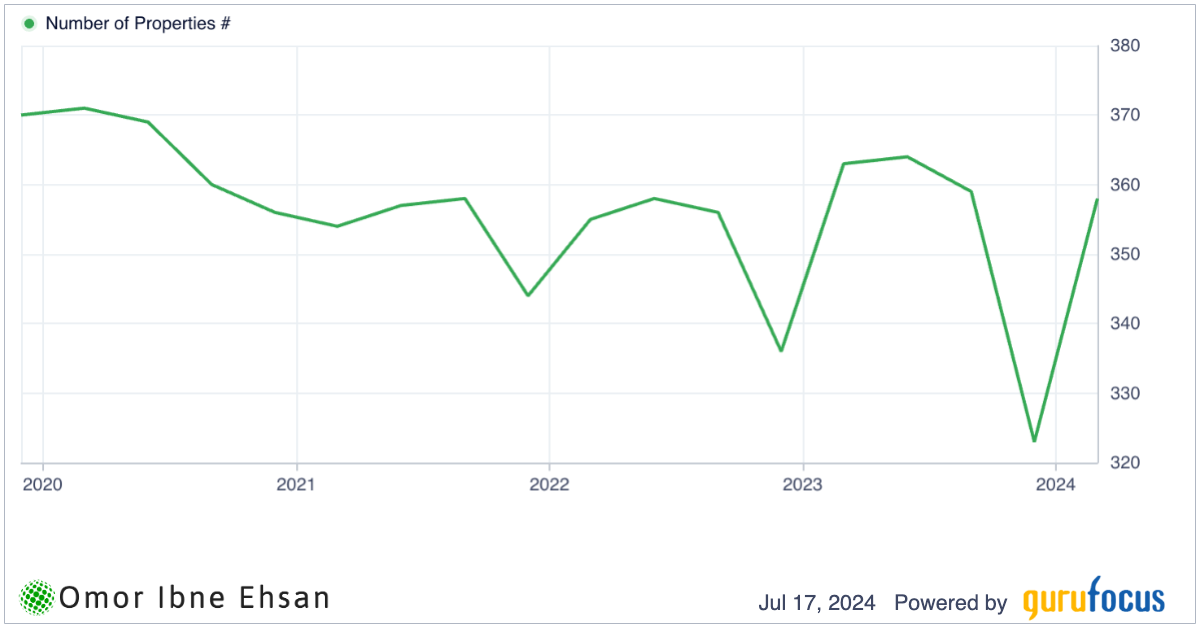

EPR Properties (EPR)

EPR Properties (NYSE:EPR) has faced challenges in recent years, with its stock price still down nearly 50% from pre-pandemic highs. REITs overall have corrected significantly, and there’s plenty of pessimism around real estate. No one knows for sure how the sector will perform going forward, but I’m optimistic it can hold up better than the 2008 crash. Smaller family sizes and soaring migration into the U.S. provide tailwinds. Plus, most REITs are already trading at depressed valuations, so further downside seems limited. EPR’s juicy 7.76% dividend yield also pays investors well to wait for a recovery.

In Q1 2024, EPR beat on both the top and bottom lines. FFO of 75 cents per share surpassed estimates by 13 cents, while revenue of $167.23 million beat by $18 million. Management also affirmed full-year FFO guidance of $4.76-$4.96 per share. The property numbers have been a bit volatile, but they are no longer declining as fast once you average it out.

Click to Enlarge

The company continues to make progress in diversifying away from movie theaters into other experiential real estate. Thus, I believe the market is overly discounting EPR’s prospects.

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

On the date of publication, the responsible editor did not have (either directly or indirectly) any positions in the securities mentioned in this article.