Are you starting to get nervous about the frothy stock market and thinking about taking some profits off the table? You’re not alone. With the economy flashing warning signs and many high-flying tech names coming back down to earth, it might be time to consider shifting some of your portfolio into recession-resistant stocks.

Last week was a bloodbath for many market darlings, and fear is still gripping investors. Frankly, I believe this fear is justified. Unemployment is ticking up, job growth is slowing and the Federal Reserve looks poised to start cutting interest rates soon. Historically, rate cuts have often been a precursor to recessions.

Even the Oracle of Omaha Warren Buffett has been aggressively selling tech stocks lately. When Buffett starts battening down the hatches, it’s worth paying attention.

Economic indicators like the inverted yield curve and the Sahm rule, which have reliably predicted past recessions, are flashing red. Thus, consider rotating some of your profits into recession-resistant stocks, such as these seven.

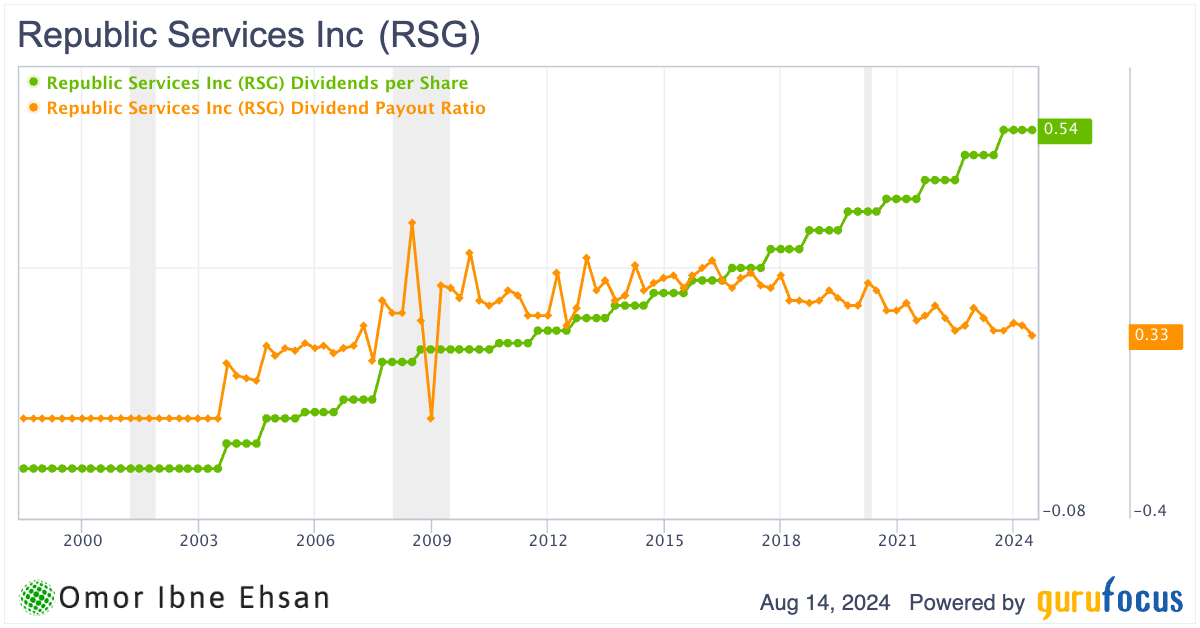

Republic Services (RSG)

I believe Republic Services (NYSE:RSG) is one of the most stable and consistent stocks you can own, and for a pretty self-explanatory reason. Trash collection is usually not significantly affected by economic downturns or recessions. Moreover, Republic Services benefits from the ever-increasing number of U.S. households, which is only going to rise further based on recent migration trends.

In my view, RSG stock is a solid recession-resistant holding, and it also offers a small 1.16% dividend yield.

Click to Enlarge

Analysts expect mid-single-digit revenue growth and low double-digit EPS expansion in the coming years. I think that’s sufficient to justify the stock’s current premium valuation.

Additionally, Republic Services is making strides in sustainability, hitting its emissions reduction target two years ahead of schedule. However, BMO Capital Markets recently downgraded the stock to “market perform”, so analysts have differing opinions.

Regardless, I expect it to weather a recession well.

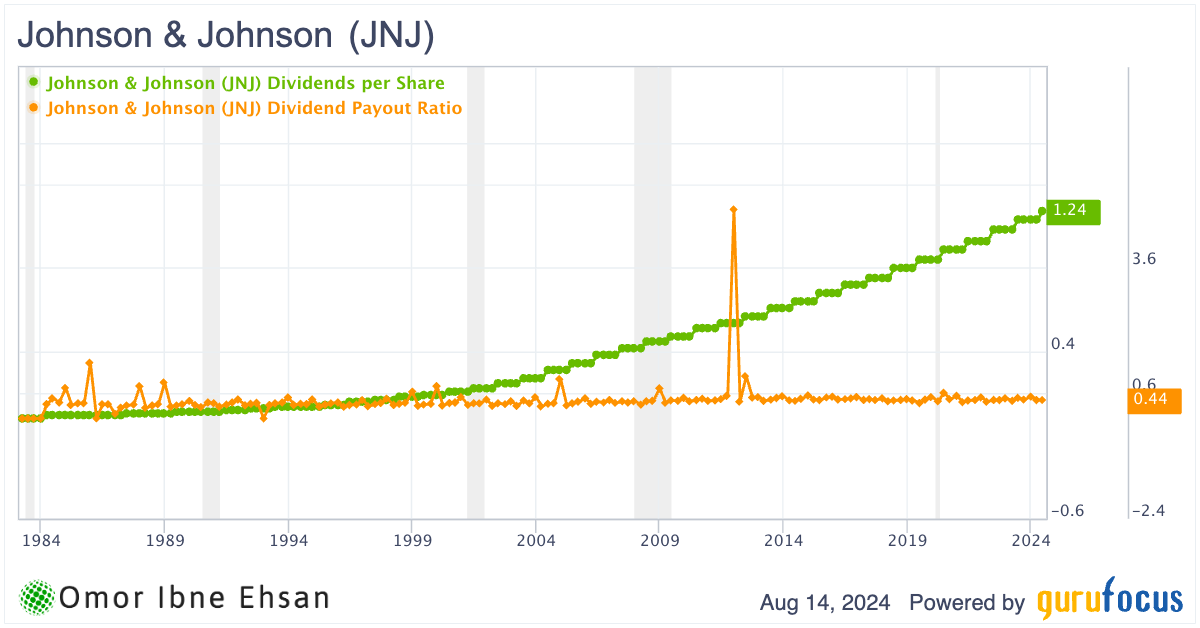

Johnson & Johnson (JNJ)

Johnson & Johnson (NYSE:JNJ) is a healthcare behemoth with its fingers in everything from pharmaceuticals to medical devices. The company just reported solid Q2 of fiscal year 2024 results, with worldwide sales growing 6.6% operationally to $22.4 billion. “Innovative Medicine” segment sales surged 7.8% due to brands like Darzalex and Tremfya.

Yet, it’s not all sunshine and rainbows. JNJ faces some headwinds, like the upcoming biosimilar competition for immunology blockbuster Stelara in Europe. Also, the company can’t seem to shake its talc litigation woes, though it looks close to getting enough claimant support for a $6.5 billion settlement.

Still, analysts remain bullish overall, with a consensus price target of $172, implying a 9% upside. Cantor Fitzgerald is particularly optimistic, recently reiterating an “overweight” rating and a $215 target. I tend to agree that J&J’s diversified business and 3.1% dividend yield make it a safer harbor in this stormy market.

Click to Enlarge

It may not be the most exciting stock, but you could do a lot worse than this reliable healthcare giant as recession fears swirl.

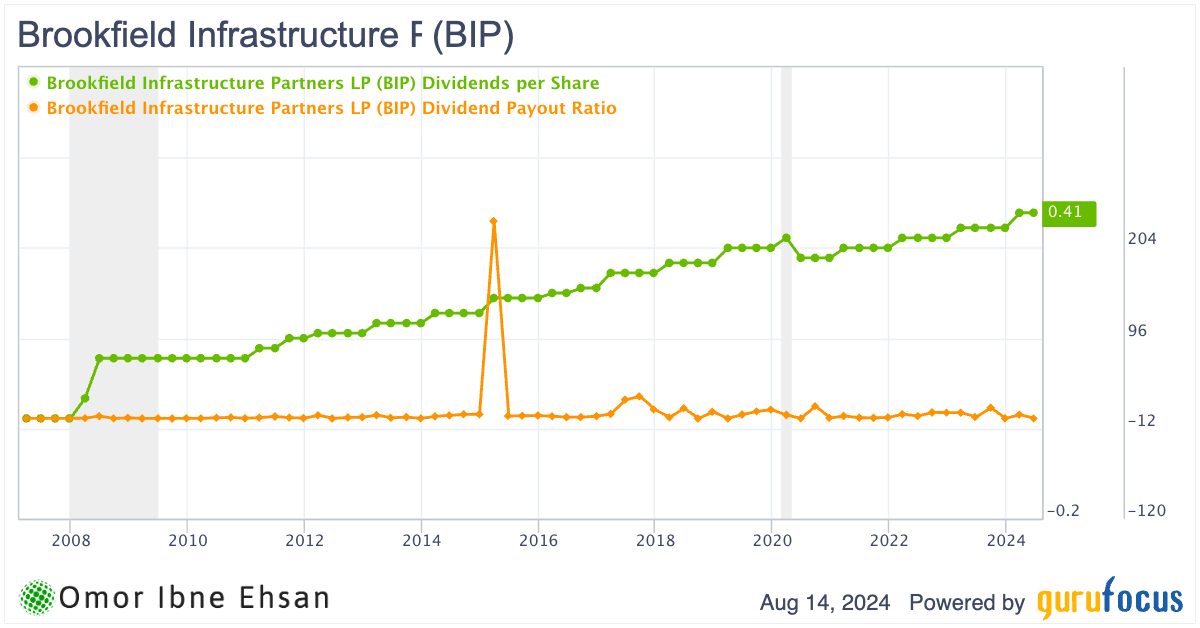

Brookfield Infrastructure Partners (BIP)

Brookfield Infrastructure (NYSE:BIP) has been one of the steadiest stocks recently, and the company can continue building on that record to weather a potential recession well. As an infrastructure company, it is benefiting from significant government subsidies. And even though it’s based in Canada, it has access to a wealth of infrastructure businesses in the U.S. and abroad. I see significant room for growth going forward that a recession is unlikely to derail.

In Q2 FY24, Brookfield Infrastructure reported a 10% year-over-year (YOY) increase in funds from operations (FFO) to $608 million. The utilities, transport, midstream and data segments all contributed to this growth. Most analysts remain bullish, with an average price target of $38.50, representing a 27.4% upside.

The surge in artificial intelligence (AI) adoption is generating substantial capital deployment opportunities across BIP’s data, electric utility and natural gas sectors. Couple that with the stock’s solid 5.4% dividend yield, and you have a recession-resistant stock worth holding onto tightly in 2024.

Click to Enlarge

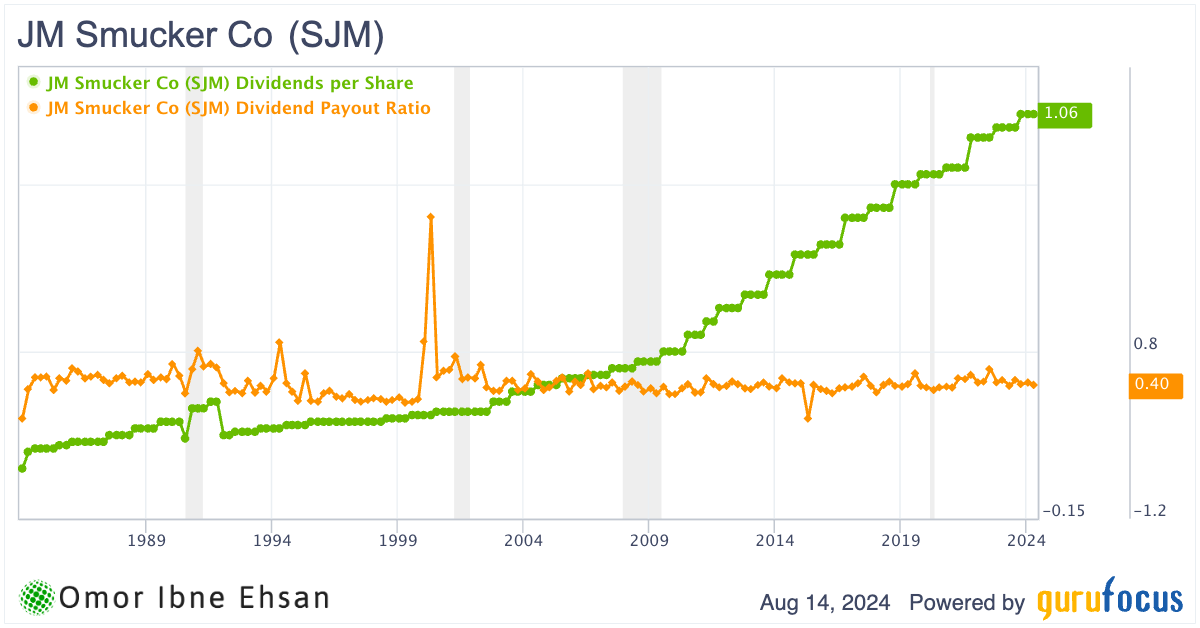

J M Smucker (SJM)

J M Smucker (NYSE:SJM) manufactures food products with very sticky demand like snacks, peanut butter and pet food. These categories are unlikely to see much of a pullback even in a recession, as they make up a small portion of consumer spending and bring joy to kids and pets. J M Smucker’s stock has already taken a 27% hit since the start of 2023. So, I think much of the downside risk is priced in at this point.

The company delivered solid Q4 FY24 results, with net sales of $2.2 billion and adjusted EPS of $2.66, up 1% YOY. For FY25, management is guiding for both positive volume and pricing growth, a rarity in the current packaged food landscape, according to Barclays analyst Andrew Lazar. Also, J M Smucker is investing heavily in its fast-growing Uncrustables brand to drive household penetration.

Click to Enlarge

As a cash cow with an attractive 3.7% dividend yield, I view SJM as a resilient pick to depend upon to weather a potential economic storm.

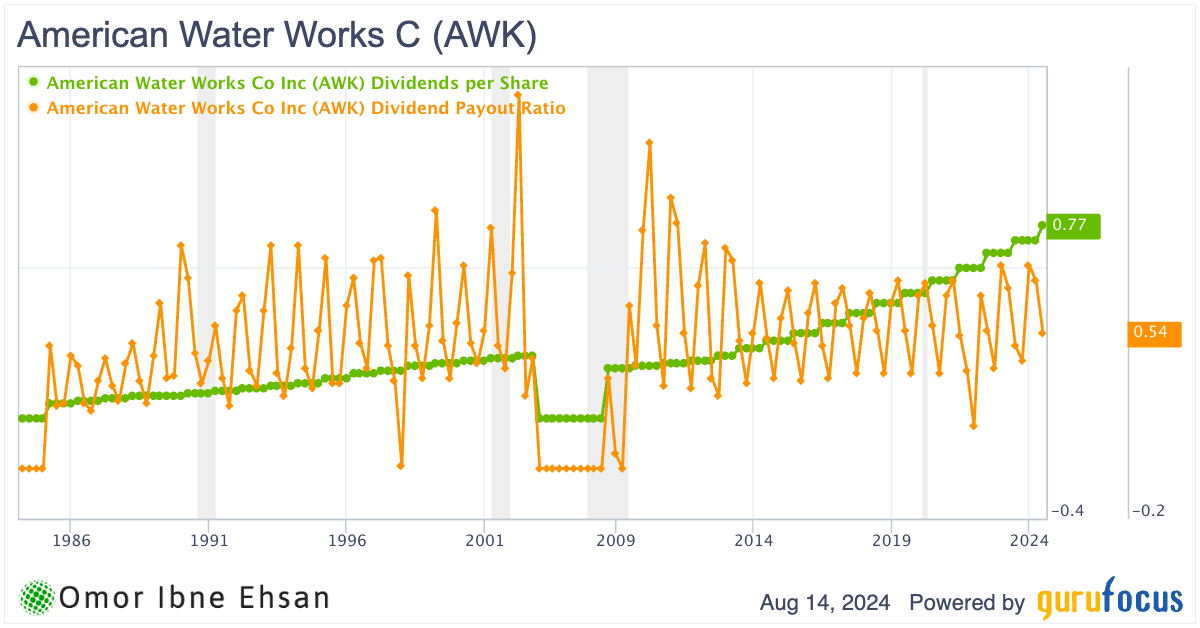

American Water Works (AWK)

American Water Works (NYSE:AWK) is the largest publicly traded water and wastewater utility company in the U.S., providing water services to approximately 14 million people across 24 states. The name is pretty self-explanatory. I see American Water Works as a recession-resistant holding that could help your portfolio weather any upcoming market volatility.

Since the start of 2022, American Water Works’ stock has been on a downtrend, falling 35% before rebounding in April this year. Over the past six months, the stock has recovered by an impressive 17.4%. I believe the current risk-reward setup is solid, especially with a potential recession looming on the horizon. If the market recovers, there’s significant upside potential for American Water Works. On the flip side, the downside risk may be quite limited at this point.

One thing I love about this company is its strong track record of dividend growth.

Click to Enlarge

As of August 14, 2024, American Water Works yields an attractive 2.16%. That’s a nice bonus on top of the stock’s defensive characteristics.

In Q2 FY24, American Water Works’ Regulated Businesses segment reported net income of $274 million, slightly down from $278 million in the same period last year. However, the company affirmed its 2024 earnings per share guidance range of $5.20 to $5.30 and its long-term EPS and dividend growth rate targets of 7-9%.

So, if you’re looking for a recession-resistant stock to anchor your portfolio, consider adding some American Water Works to your holdings.

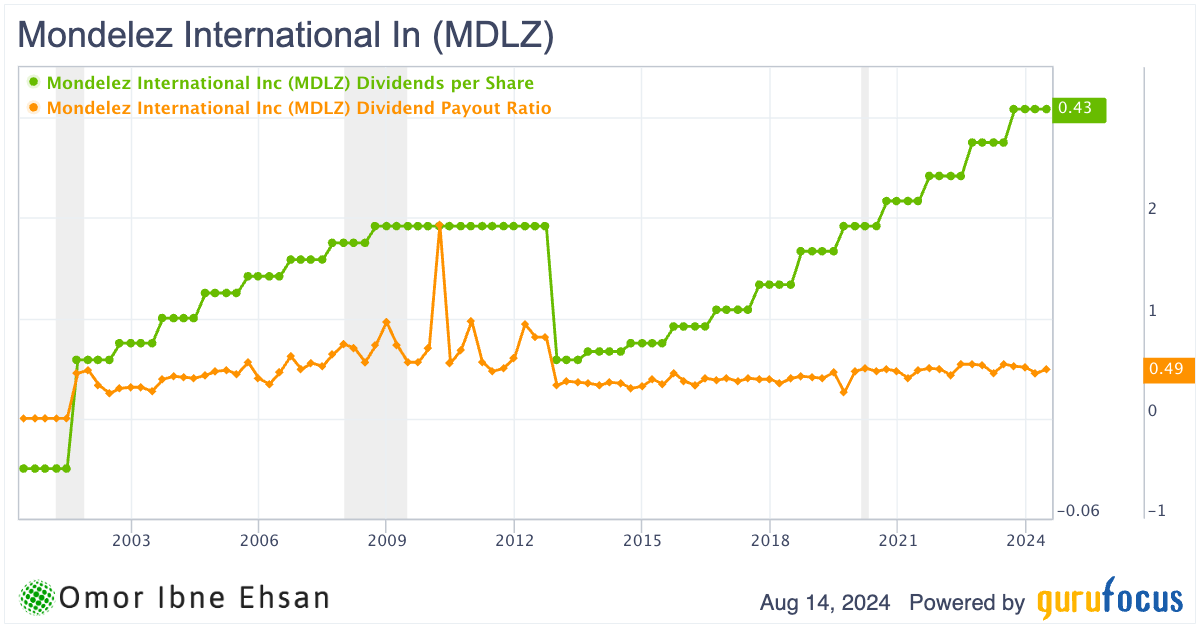

Mondelez International (MDLZ)

Mondelez International (NASDAQ:MDLZ) manufactures and markets snack food and beverage products worldwide. The company recently reported solid second-quarter 2024 results, with organic net revenue growing 2.5% despite a challenging economic environment. Adjusted EPS increased an impressive 25% on a constant currency basis, driven by strong operating gains and cost discipline.

I believe Mondelez International represents a fairly safe stock to continue holding, even if a recession hits. Companies with beloved snack brands like Oreo, Ritz, Cadbury and Toblerone tend to have loyal customers who keep buying their favorites in good times and bad. That’s the reason MDLZ stock has been on a consistent upward climb for the past 15 years.

Click to Enlarge

With a 2.67% dividend yield, Mondelez International should also put cash in your pockets during downturns, though it isn’t really as stable due to the late-2012 cut.

Regardless, analysts are bullish, with Goldman Sachs recently initiating coverage with a “buy” rating. The consensus price target of $79 implies 18% upside from current levels. While no stock is completely recession-proof, I’m confident that Mondelez International’s snacking business will hold up better than most.

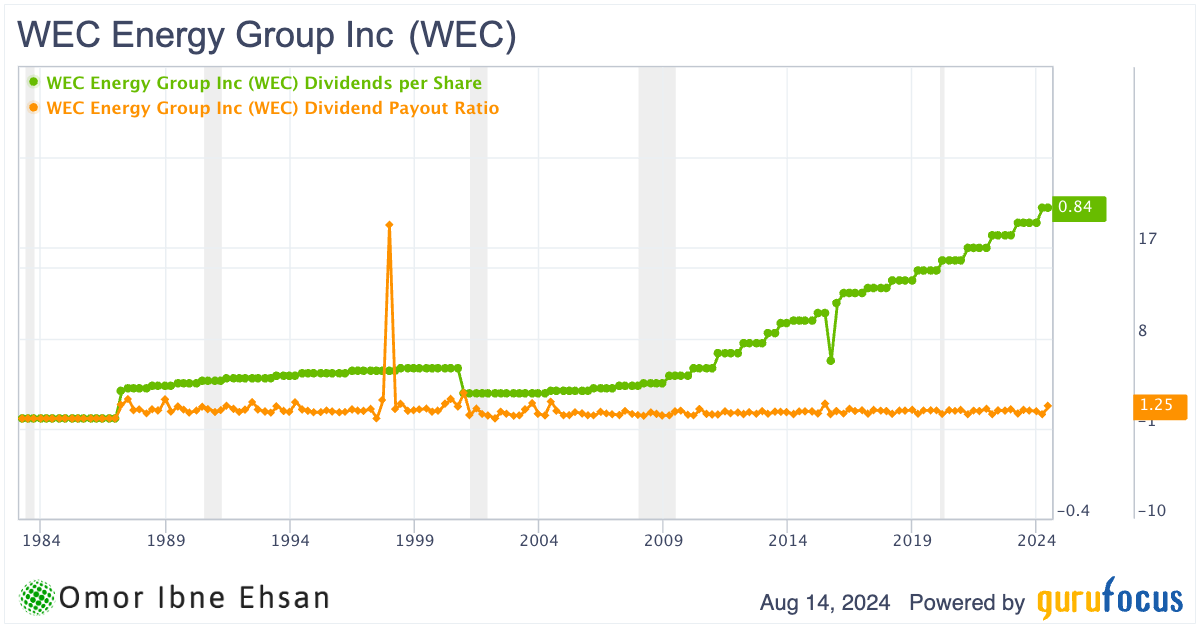

WEC Energy (WEC)

WEC Energy (NYSE:WEC) provides electricity and natural gas to customers in the Midwest. While a recession could impact energy demand and prices, I believe WEC stock should remain relatively resilient.

As a regulated utility, WEC has the ability to adjust rates to maintain stable financials, even during economic downturns. This is why the stock didn’t crater during the Great Recession, Instead, it declined gently. And although WEC shares have dipped slightly since mid-2022, I see limited downside risk going forward, recession or not.

In Q2 FY24, WEC reported earnings of 67 cents per share and reaffirmed its full-year guidance of $4.80-$4.90 EPS. The company is executing its largest-ever five-year $23.7 billion capital plan. Analysts seem cautiously optimistic, with a consensus moderate buy rating. J.P. Morgan’s Jeremy Tonet maintains a “strong ell” rating, though, with an $84 target. That’s really not much downside.

While not flashy, I view WEC as a defensive stalwart that should keep churning out reliable results.

Click to Enlarge

With a 3.7% dividend yield, low-risk projects supporting 6-7% long-term earnings growth and a recession-resistant business model, WEC could be a port in the storm for 2024.

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

On the date of publication, the responsible editor did not have (either directly or indirectly) any positions in the securities mentioned in this article.