Times are rough pretty much everywhere, but that might spell a golden opportunity for discount stores. Although the current administration loves to trumpet the 5% unemployment rate as direct evidence that the U.S. economy is on the rise, the rubber hasn’t quite met the road.

Recent earnings performances for bellwether stocks have been mixed, with several companies missing on revenue estimates. In addition, massive layoffs have been announced, contradicting positive sentiment. Logically, more people are now price sensitive, and that plays right into the hands of discount stores.

Make no mistake — the economy is far from robust. The long-term reduction in unemployment conveniently sidesteps the fact that labor participation is down. True, a contributing factor is “baby boomers” retiring. Consequently, that’s a bullish argument in and of itself for discount stores. But beyond that, 19 states — including California, Illinois and Ohio — have unemployment rates that are higher than the national average. Combined, these states contribute approximately 40% of the national gross domestic product. Ignoring the challenges they face would be a terrible mistake.

But ignoring them is exactly what the U.S. Federal Reserve appears to be doing. Despite clear indications that actual consumer spending is decreasing — a sharp plunge in March auto sales being the loudest example — the Fed chose to dance around the issue. In a statement released a few weeks ago, the central bank characterized the slide in spending as “moderated” growth. Further, they bizarrely affirmed that “consumer sentiment remains high.”

Try telling that to grocery giant The Kroger Co (KR). Its annual sales growth rate for fiscal year 2016 was 1.3%, the lowest since FY 2010. Coincidentally, KR stock is down 16% year-to-date. Being a secular business, KR should be able to regain traction. However, it’s fairly obvious that they are losing market share to discount stores. And if the economy continues to trudge along at a tepid rate, traditional retailers may lose more volume to bargain specialists.

That’s not great news for most stocks. However, for discount stores, the garbage economy is a Godsend. Here are three bargain retailers that are light on the wallet and heavy on returns.

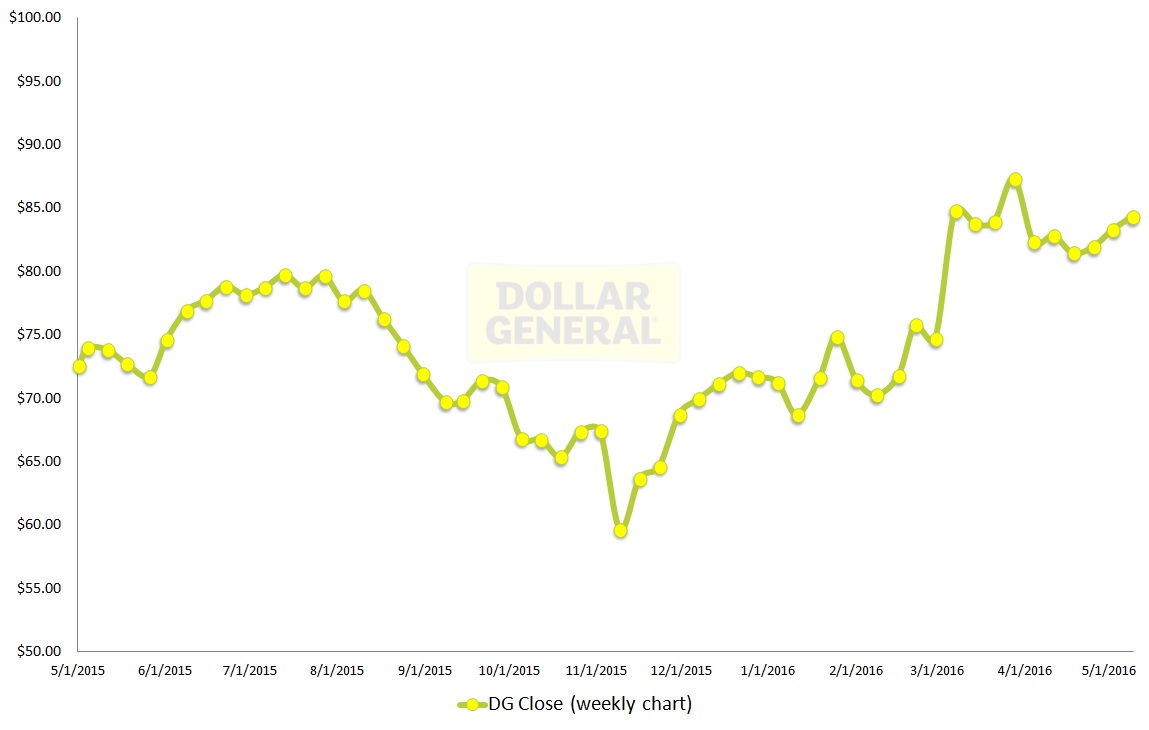

Discount Stores That Feed on Economic Garbage: Dollar General Corp. (DG)

Click to Enlarge

As far as publicly traded discount stores are concerned, Dollar General Corp. (DG) is the undisputed king. In both top-line sales as well as market capitalization, DG bests its nearest rival.

On top of that, DG is not strictly a “dollar” store. Several products exceed a buck, which means that the retailer carries brand-name products at a cheaper price. That puts it into direct competition with big-box retailers like Wal-Mart Stores, Inc. (WMT).

However, the fundamentals make DG a compelling investment idea. Both operating and net margins are highly ranked relative to other discount stores. This has helped fuel double-digit percentage growth in earnings before interest, taxes, depreciation and amortization and earnings per share over the last three years.

Furthermore, annual revenue growth for DG has been fairly stable since FY 2013, in contrast to the sharp fluctuations seen in KR sales.

Technically, as well, there’s a lot to like. DG stock is up 15% YTD, nearly 10 times higher than the equities benchmark SPDR S&P 500 ETF Trust (SPY). A majority of the bullish sentiment occurred over the trailing three months, when DG gaped up thanks to a fourth quarter

Currently, DG is supported by its rising 50-day moving average, which has shifted positively since mid-December of last year.

So long as Dollar General continues to deliver the bargains, DG stock should win out in the markets.

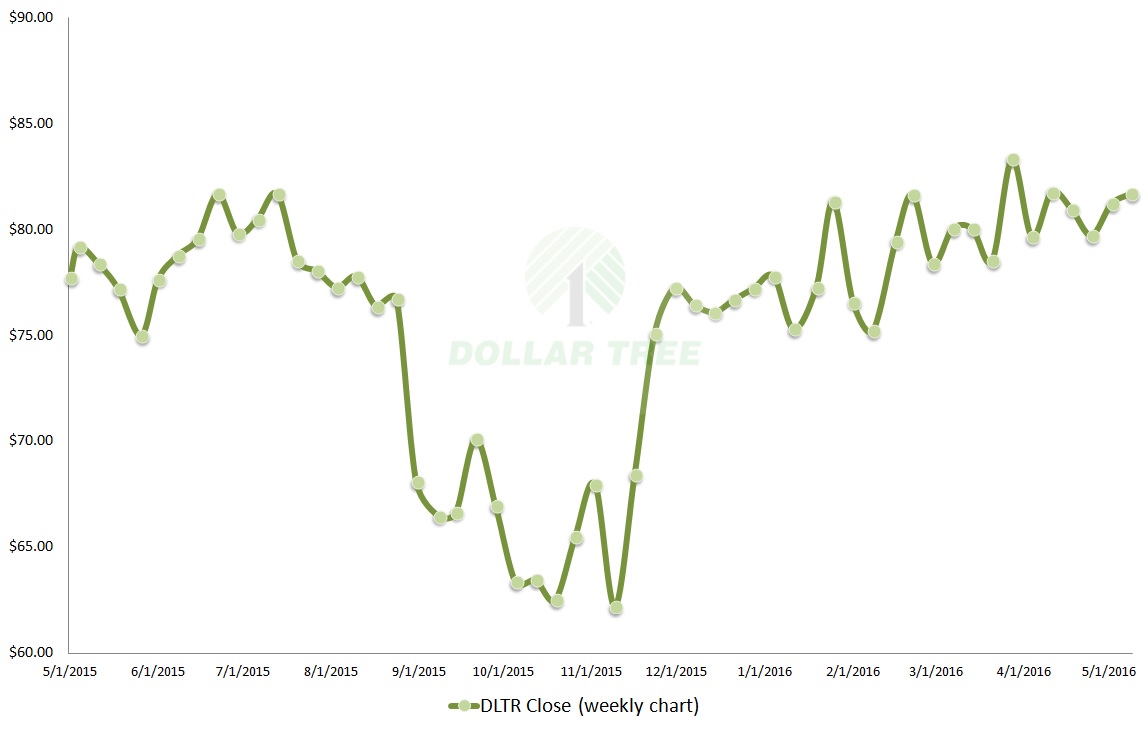

Discount Stores That Feed on Economic Garbage: Dollar Tree, Inc. (DLTR)

Click to Enlarge

After Dollar Tree, Inc. (DLTR) announced that it was going to take over Family Dollar Stores, Inc. — essentially, the lightweight of publicly traded discount stores — there was plenty of skepticism.

Why would DLTR bother with paying a rich premium for an operation that could turn out to be more of a liability than asset? Off the top, DLTR could use their expertise to revitalize Family Dollar and later sell it for a pretty penny. In the meantime, DLTR wields hefty coverage among discount stores, and that could be a key advantage moving forward.

With the completed acquisition, annual revenue for DLTR is nearly $15.5 billion, or within 25% of Dollar General’s sales results for FY 2016. The issue, of course, is efficiency.

DLTR saw a 74% decline in net margins once Family Dollar was on their books. This is where the extra coverage comes into play. Thanks to the buyout, DLTR has 13,851 discount stores, as opposed to DG’s 12,489 locations. In addition, DLTR is aggressively expanding into California, where it’s sure to do some damage with both direct and indirect competitors.

For all the naysayers, DLTR stock has done fairly well. Since the buyout announcement, Dollar Tree shares have moved up about 50%. On a YTD basis, DLTR has gained 3%. To be fair, it’s currently stuck in a consolidation pattern. However, a number of traders have a bullish position on DLTR, implying that shares can work themselves out of the sideways pattern.

With the underlying economy providing another tailwind, DLTR looks more and more as if it’s on the right track.

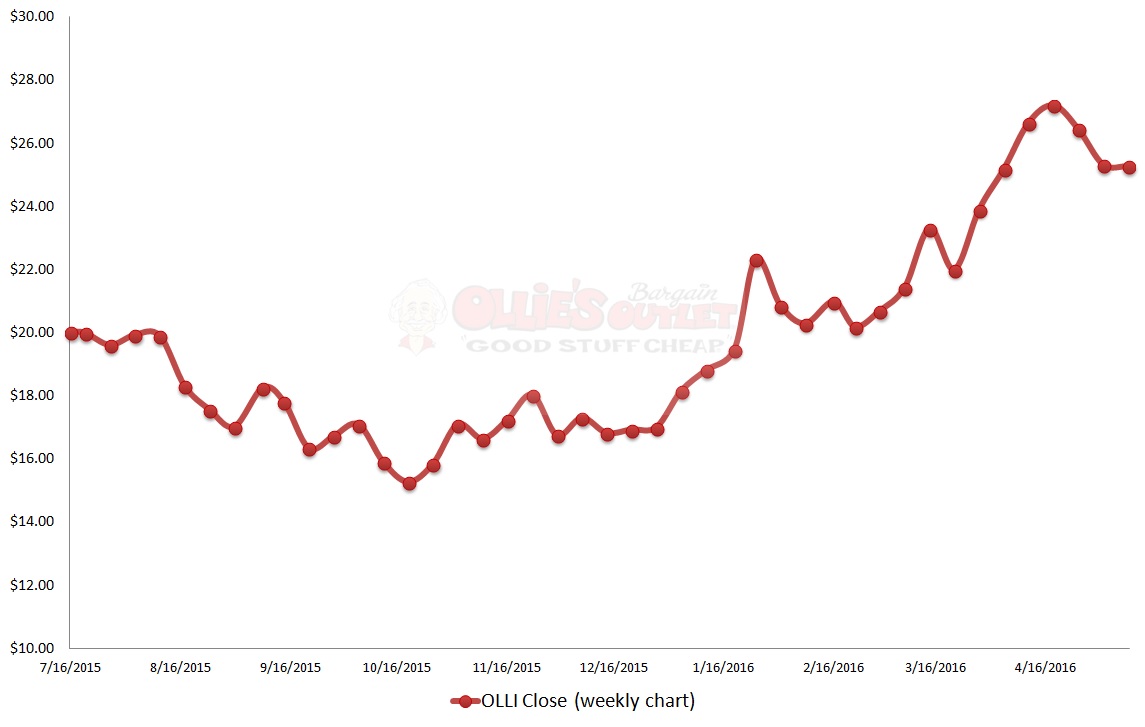

Discount Stores That Feed on Economic Garbage: Ollie’s Bargain Outlet Holdings Inc (OLLI)

Click to Enlarge

The newcomer among discount stores is Ollie’s Bargain Outlet Holdings Inc (OLLI). OLLI has a distinct business model compared to DG and DLTR, specializing in the resale of overstocked or salvaged goods.

Rebranded in March 2015, OLLI operates 208 discount stores across 18 states, with its latest grand opening taking place in Orlando, Florida. Although it doesn’t have the name recognition of DLTR or DG, OLLI has much more to offer in terms of speculative growth potential.

That’s fairly evident when you look at Ollie’s financials. Quarter-over-quarter sales growth averages 19%, while net income for the most recent quarter jumped by 34% against the year-ago level, which was supported by double-digit operating margins.

OLLI currently runs operations exclusively on the eastern half of the U.S. Should they decide to expand westward, we can reasonably expect a significant boost in these numbers. The argument is more compelling considering the price-sensitive nature of the consumer market.

Technically, it has been nothing but love for OLLI stock. The company handily beats out the other discount stores with a YTD performance of 45%. Notably, OLLI was one of the few stocks in the financial markets that had an exceptionally strong January, gaining close to 30%. Other than a correction in February, the overall trend has been very bullish for OLLI.

With the economy the way that it is, there may be no better time than now to consider bargain retailers like OLLI.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.