There’s no denying it: Twilio (NYSE:TWLO) is one of the top performers of this year. Not only that, Twilio stock has pulled a Houdini act, rising from the doldrums that started in 2016. For some time, it looked like shares were doomed for complete annihilation. But since January 2018 year, TWLO stock has rocketed up almost 500%.

![]() From a financial growth perspective, it appears that the bullishness in TWLO stock is justified. In the company’s early stages, its revenue trajectory was rather modest. But beginning in the first quarter of 2016, year-over-year sales growth shot up to high double-digit levels. Remarkably, the cloud-communications firm has maintained this frenetic pace.

From a financial growth perspective, it appears that the bullishness in TWLO stock is justified. In the company’s early stages, its revenue trajectory was rather modest. But beginning in the first quarter of 2016, year-over-year sales growth shot up to high double-digit levels. Remarkably, the cloud-communications firm has maintained this frenetic pace.

As prime evidence, Q1 2019’s sales totaled $233 million, representing an 81% year-over-year lift. In Q3 and Q4 of 2018, sales growth YOY measured 68% and 77%, respectively. That’s quite impressive for Twilio stock because the law of small numbers dictates that as revenues expand nominally, growth should tick down.

Fundamentally as well, the bulls seemingly have justification in their optimism. Of course, TWLO stock is an investment in the rapidly rising world of cloud computing. Not only is this a likely relevant sector for years to come, we’re near the infancy stage of a massive paradigm-shift.

Well-known organizations like Amazon (NASDAQ:AMZN), Microsoft (NASDAQ:MSFT), and Alphabet (NASDAQ:GOOGL

) have cemented their presence in the cloud’s front-face components of data storage and infrastructure-as-a-service. Twilio aims to lever the same dominant impact in the communications arena of the cloud.

Taken as a whole, these arguments bolster the case for Twilio stock. But with shares having gone up so rapidly, what’s the best approach?

Great Time to Sell Twilio Stock

Like probably the vast majority of InvestorPlace readers, I don’t like buying into extreme strength. Even armed with the best thesis, I always feel as if I’m going to end up holding the bag. Again, with TWLO stock having skyrocketed last year, and in the year-to-date, I’m naturally cautious.

But I’m not cautious at all about how I would approach Twilio stock if I was a shareholder: I’d sell this puppy into strength, with perhaps the aim of picking some up on discount.

For full disclosure, I warned readers about potential fundamental problems with TWLO. Basically, I argued that management’s strong ambitions didn’t align with their financial stability. Sure, sales are growing in a huge way, but let’s face it: nominally, they’re not that impressive. Plus, Twilio would need to make costly investments to stay on top of their highly competitive industry.

So far, though, Twilio stock has kept chugging away.

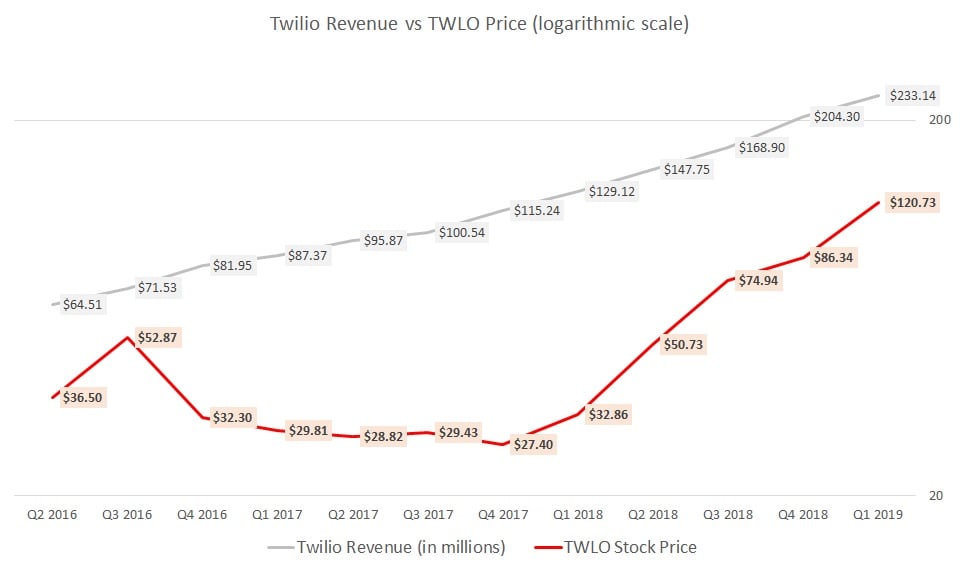

But at some point, shares will correct. In the chart below, I compare Twilio’s revenue with the TWLO stock price on the same logarithmic scale. I used such a scale because it gives us a better picture of the magnitude growth of the target metrics.

Click to Enlarge

You can see that revenue has consistently marched forward, almost in perfect linear fashion. On the other hand, the Twilio stock price is very much non-linear. Between Q4 2016 through Q1 2018, shares were grossly undervalued. But by the last reporting quarter, I would say that shares approached fair value, if not overvalued.

So, I see two nearer-term risks. If you load up the boat now, you’re definitely not buying at a great price. At best, you’ll probably experience modest growth.

The other risk is that Twilio’s future quarterly revenues may disappoint. With investors accustomed to outrageous growth, TWLO stock could drop in a hurry.

Markets Offer Clues on TWLO Stock

In the first three months of this year, Twilio stock gained a whopping 48%. But since the end of March, TWLO has only moved up a comparatively pedestrian 12%.

I don’t find this surprising one bit. Shares are merely experiencing the market’s gravitational law: what goes up must come down (or at least incur a correction).

And I believe that this current pensiveness points to my earlier argument that TWLO stock is stretched right now. Back in Q4 2017, each dollar of Twilio’s equity price “bought” $4.21 million of revenue. Now, this ratio has dropped to $1.65 million.

In other words, you’re not getting anywhere close to the fundamental value that Twilio stock once delivered. Since we’re still talking about a relatively speculative tech firm, it’s best to wait if you’re a prospective buyer. If you’re already a shareholder, what are you waiting for? Sell it now!

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.