[[Editor’s Note: This article was updated on Dec. 16, 2019, to correct the net income losses for Shopify.]]

Shopify (NYSE:SHOP) stock trades at such a lofty valuation it seems priced for perfection. Any misstep by management or the company will likely pop the stock’s ballon.

Some issues we see with Shopify stock are its decelerating revenue growth, continuing losses, and the outlandish valuation even if its growth and losses improve.

Decelerating Growth and Continuing Losses

Shopify reported revenue of $390.6 million for Q3 2019. SHOP made a big point that this was 45% higher than the year-ago quarter.

In reality, this revenue was just 7.9% higher than its prior quarter. More importantly, the year-over-year growth rate has been decelerating.

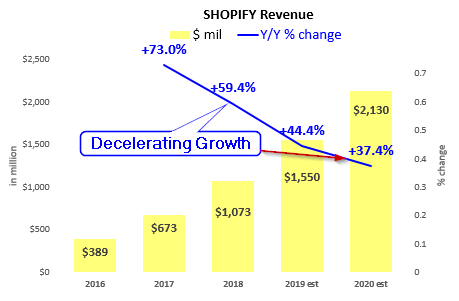

You can see this in the table I have prepared. SHOP’s year-over-year growth has been slowing every quarter.

In fact, using estimates provided by Shopify for Q4 2019 revenue and Street estimates of Shopify’s 2020 revenue, growth over the past four years will be much lower.

The provided chart shows these estimates and the slowing rates.

In 2016, Shopify’s revenue grew 73% year-over-year. But by 2020 estimates are that Shopify will show revenue growth almost half of that amount, at 37.4%.

Click to Enlarge

Although this might be expected since the revenue numbers are increasing, one would think that Shopify would also be showing profits with the higher revenue.

SHOP Stock Losses Are Widening

But that is not happening. Shopify reported a net loss of $72.8 million for Q3.

This is significantly higher than the prior quarter loss of $28.7 million, as well as the prior year quarterly loss of $23.2 million

You can see this by comparing the margin on revenue. In Q3 the loss margin was -18.6%, vs. -7.9% in the prior quarter, and -8.6% in the prior-year quarter. As revenue rises, even though it is decelerating, the company’s losses widen.

To be fair, Shopify likes to adjust its earnings, as many fast-growing companies do. They like to erase out things like stock-based compensation. I don’t like to use these measures.

I have written about these kinds of other adjustments

at Shopify and at Square (NYSE:SQ). Essentially, they are designed to make the company appear more profitable than under GAAP rules and other companies.

Priced to Perfection, Shopify Stock Valuation Won’t Last

Here is the harsh reality: Shopify’s market value is $42.6 billion, but it has produced net income losses of $125.6 million in the past nine months.

Shopify stock has a price-to-sales ratio of 27 times 2019 estimate revenue and 20 times 2020 estimated revenue. These ratio numbers are so high they normally are the levels used for price-to-earnings. In effect, if revenue slows down, an acquirer of the company would have to wait 20-plus years before the price they paid would equal the revenue of the company today.

Needless to say, buyers at these levels think that revenue will quadruple or more in the next five years. The problem with that theory is that everything has to go perfectly. If the U.S. hits a recession, or management cannot handle growth at this rate, the valuation will fall.

Most of Shopify’s competitors have price-to-sales ratios that are significantly below Shopify stock. For example, Etsy (NASDAQ:ETSY) trades for just 6 times its 2019 revenue estimates and 4.7 times 2020 estimates. ETSY’s market value is less than $1 billion.

But even Square, which has a similar market cap to Shopify at $28 billion, trades for just 12.6 times 2019 revenue estimates, and 9.9 times 2020 estimates, according to Seeking Alpha.

It is highly likely that Shopify’s valuation cannot stay at these lofty levels.

What Should Investors Do?

At this point, even if you really like the underlying story at Shopify, you should wait until there is a dip in the Shopify stock price. At least you might find a point-of-entry where some sort of margin of safety can be attained.

I don’t think buyers of Shopify stock at these prices today will have a good chance of making a solid return on their investment. Better to wait until there is a more profitable entry point.

As of this writing, Mark Hake, CFA does not hold a position in any of the aforementioned securities. Mark Hake runs the Total Yield Value Guide which you can review here. The Guide focuses on high total yield value stocks. Subscribers a two-week free trial.