Even before it went public, Blue Apron Holdings Inc (NYSE:APRN) had been under pressure. First, it had to lower its IPO price range from $15 to $17 down to the $10 to $11 range. Then on Jun. 29, 2017, APRN stock priced at the lower end of that range at $10 as its rough ride was still just getting started.

On Jun. 30, the stock closed about flat on its first day of public trading, despite running to $11 earlier in the session. That would be its best day, as APRN stock went on a steady decline lower. This April, it finally bottomed below $2 per share, at $1.72. To say investors are frustrated would be an understatement, given APRN stock fell more than 80% from its IPO price within 10 months.

So what now?

Evaluating Blue Apron Holdings Inc

Even before it went public, there were big-time concerns about how high the company’s marketing expenses ran. Little return on investment from its big advertising spend and a lack of profitability really hurt APRN stock. Negative cash flow and free-cash flow didn’t help matters.

Competition was and still is another huge factor. Whole Foods being purchased by Amazon.com, Inc. (NASDAQ:AMZN) happened right around APRN’s IPO and put a huge red flag on the name.

Amazon has the funds, scale, and most importantly, the patient investor base to squeeze out competition in meal delivery markets. Walmart Inc (NYSE:WMT), Weight Watchers International, Inc. (NYSE:WTW) and others getting into the market isn’t helping either.

Privately held HelloFresh did $1 billion in sales for 2017, up more than 50% from its 2016 results. In 2018, the company is aiming for break-even operations. Profitability and the $1-billion sales mark have eluded Blue Apron so far and should this year and next as well.

A new CFO will help, which APRN announced on May 17 by hiring Tim Bensley. With experience at PepsiCo, Inc.

(NYSE:PEP) and a number of other outfits, this should be viewed as a very solid move. It should at least help tighten up Blue Apron’s spending and boost its margins.

Last quarter showed some light at the end of the tunnel. An EBITDA of -$17.2 million came in nearly twice as good as investors were expecting, while revenue per user jumped to $250 from $236. These were small victories, but victories nonetheless. A pilot program with Costco Wholesale Corporation (NASDAQ:COST) should help, too.

Valuing APRN Stock

Let’s be honest here. There’s a lot to be desired with APRN stock. While it’s no longer down 83% from its IPO price, it’s hard to be too excited about it trading for just $3. Some investors surely have to be wondering, though, is the worst already priced in?

Trading at less than one times sales, APRN isn’t wildly expensive. Plus, with a number of other companies expanding into food delivery and meal kits — notably Kroger Co (NYSE:KR) buying Home Chef for upward of $700 million a few weeks ago — there’s reason that APRN stock could be an acquisition target despite its less-than-stellar results so far.

Despite its mediocrity, it does have a large customer base of roughly 750,000 customers and a well-known brand name. But we can’t buy a name on the singular hope that it will be acquired. Furthermore, its fundamentals don’t necessarily make APRN stock a screaming buy either (although admittedly Blue Apron is improving).

So what does the stock price suggest?

Trading APRN Stock

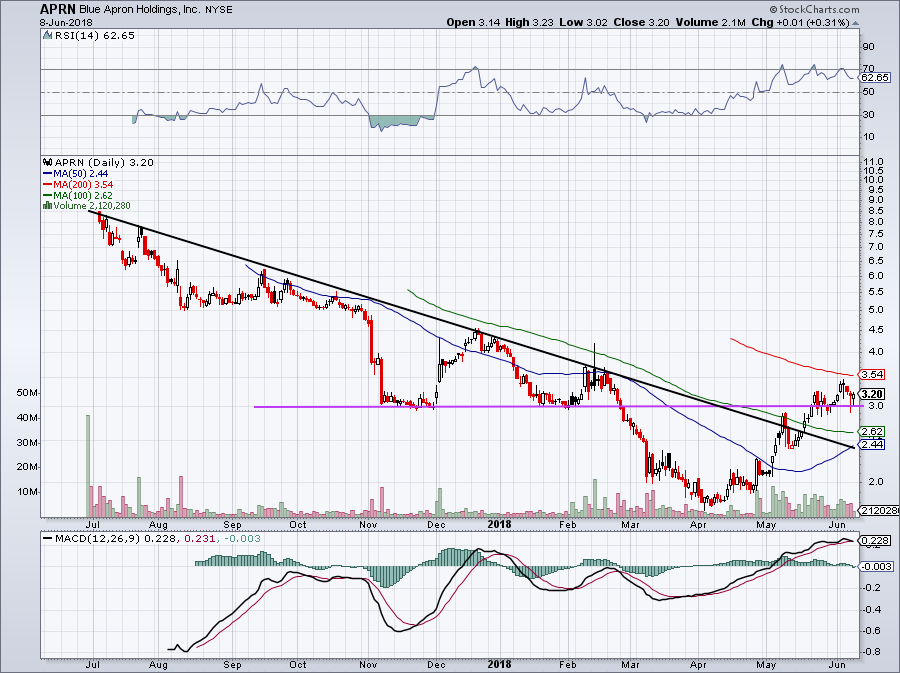

Click to Enlarge

As for APRN stock, its price action is encouraging. In early May, APRN broke over downtrend resistance (black line). The significance of this resistance shouldn’t be overlooked as it’s been in place since the IPO.

Getting over $3 was also a significant move. With that in mind, the next obstacle will be to get above its 200-day moving average. Should it do so and gain some momentum, APRN stock has the potential to outperform.

Bulls have a few ways to play this. Investors can buy APRN stock with a stop below $3. Investors who want a better risk/reward can wait to buy on a deeper pullback into the $2.50 level; although it’s possible Blue Apron doesn’t decline that far.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell did not hold a position in any of the aforementioned securities.