In the latest quarterly earnings, Amazon (NASDAQ:AMZN) showed that it has built a subscription juggernaut which keeps on growing. The subscription segment had revenue of $4.34 billion. This was up from $3.1 billion in the year-ago quarter and equals 42% growth after excluding F/X. After a brief dip in the growth rate in the December quarter, the growth in this segment has again picked up. This should help in improving the bullish sentiment towards Amazon stock.

After the robust growth in the latest quarter, the trailing-12-month subscription revenue was equal to $15.5 billion. If Amazon can maintain the current growth rate, we should see this segment grow to $30 billion by the end of 2020, on an annualized basis.

Some of the analysts have pointed to increased competition in streaming as a headwind for Amazon. But Amazon is in a much better position compared to Disney (NYSE:DIS), Apple (NASDAQ:AAPL) and AT&T (NYSE: T) who will be launching their respective streaming services.

No Signs of a Slowdown from Amazon Stock

A lot of attention has been paid to Amazon’s AWS and advertising segment. However, the subscription segment has kept up with these two segments in the latest quarter. AWS had a growth rate of 42% and Others (primarily advertising) segment had a growth of 36%.

Source: Amazon Filings

The recent numbers show that there is still enough room for growth in the subscription segment. Amazon can launch new subscription perks at different price points to increase the per-user revenue.

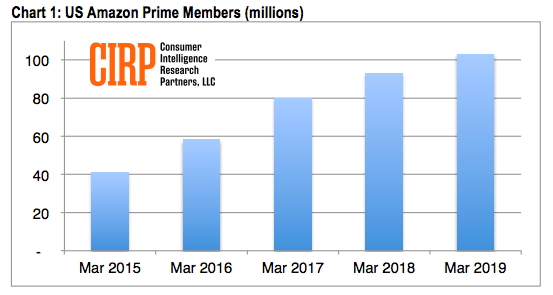

Fig: US Prime membership growth. Source: CIRP

A couple of weeks back, CIRP reported the Prime membership base in U.S. at 103 million. This was equal to 11% YoY growth. According to the U.S. census bureau, there are approximately 125 million households in the US. Hence, Amazon is now reaching over 80% of the households.

This is a big jump from 4 years back when it was at close to 40 million mark. A bigger membership base increases the bullish case for Amazon stock due to better moat for its services.

Future Growth Drivers

Although the Prime membership base is close to saturation level in the U.S., Amazon can still grow this segment through new services. Amazon can already provide one-day delivery to 72% of U.S. population. The massive investment in fulfillment and delivery centers has helped Amazon improve its delivery game. This also opens new doors to try different services in the future and increases the growth runway for Amazon stock.

In the last quarter, there was a complete rollout of “Amazon Day” service for all U.S. Prime members. This service allows a user to get all their delivery on a single day. Hence, there are lower instances of packages getting stolen, providing better convenience to customers.

Amazon is setting the expectations of customers when it comes to delivery services. It would be difficult for other big retailers other than Walmart (NYSE:WMT) to match the investments made by Amazon in delivery. One-day delivery by Amazon will also reduce the attraction of order pickups in store. This has been used by Walmart and Target (NYSE:TGT) to woo customers by leveraging their massive store base, which Amazon does not have.

Besides delivery, Amazon is also investing heavily in video. It has mentioned that the content expense in the first quarter was $1.7 billion. This is much higher than Apple, which had announced an investment of $1 billion to launch its own video services. By next year, the content budget of Amazon can easily exceed $10 billion. Because of its other profitable businesses, Amazon can continue to invest at this rate over the next few years. It would be difficult for other big streaming giants to match that for a long duration.

Improvement in its original programming library will not only help Prime membership but also provide a halo effect to other services.

Impact on Margin for AMZN

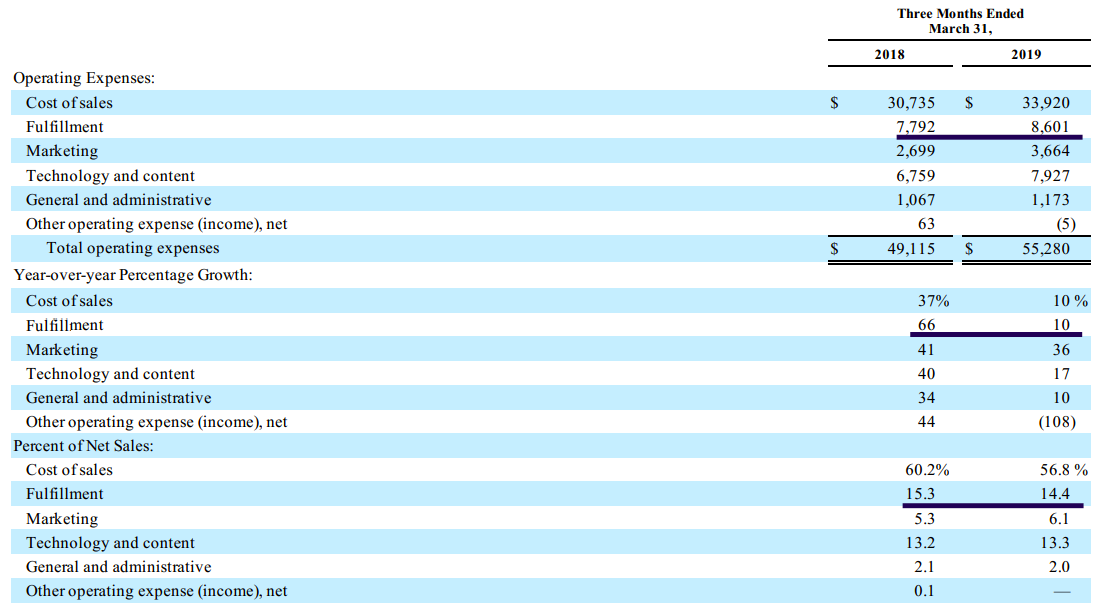

Most of the operating profits for Amazon come from AWS and advertising business. The subscription segment requires heavy investment in its fulfillment, shipping and content business. But Amazon can reduce the growth in these expenses to push the margins higher. We saw this in the latest quarter when the fulfillment expense grew only 10% on a YoY basis. In the year-ago quarter, the growth was 66%.

Source: Amazon Filings

The fulfillment cost in the recent quarter was $8.6 billion, or 14.4% of the net sales. This was 15.3% in the year-ago quarter. This 90-basis-point reduction in fulfillment expenses has certainly helped in improving the operating expenses. Once Amazon reaches saturation in terms of fulfillment centers, we could see further slowdown or reduction in fulfillment expenses.

The recent operating margin came at 7.4%, up from 3.78% in the year-ago quarter. The decrease in shipping and fulfillment expense as a percentage of net sales provides a big upside for Amazon stock.

Investor Takeaway

Amazon has been able to increase its subscription segment revenues at 42% on a year-over-year basis. At the same time, the fulfillment expense as a percent of net sales has fallen from 15.3% to 14.4%. Future growth in subscription revenue should help the company build a strong moat. This will help in reducing the pricing pressure on online goods sold through its retail platform.

Better management of fulfillment and shipping expense will help in improving the growth trajectory of the operating margin. This should help the company in posting good EPS growth and improve the bullish momentum for Amazon stock.

As of this writing, Rohit Chhatwal did not hold a position in any of the aforementioned securities.