If you are looking for millionaire-maker stocks to turn a $50,000 portfolio into $1 million in just a decade, I would like to remind you of several things. First, your portfolio would need to compound at around 35% annually. Even if most stocks in your portfolio outperform the broader market going forward and meet expectations, this is very ambitious. Even Warren Buffett’s returns have been around 20% since he started, and these returns have been more in line with the market in the past decade.

In addition, $50k is a pretty large sum for the average Joe. If you want to 20x that in a decade with no additional contributions along the way, the only stocks that could realistically do that are penny stocks. I do not recommend putting this much money into penny stocks.

However, this doesn’t mean that you’re out of luck. You can still buy some quality companies at premium valuations. And, as long as Wall Street holds up the premium valuation, they could return solid returns over the next decade. Turning $50k to $1 million is possible if you periodically put more money into these millionaire-maker stocks and the stars align for them.

Trade Desk (TTD)

The Trade Desk (NASDAQ:TTD) is a leading advertising technology company that enables advertisers to efficiently target audiences across various digital platforms. In the first quarter, the company posted revenue up 28% year-over-year (YOY) to $491.25 million, beating estimates by $10.76 million. This outperformance is caused by the ongoing shift towards programmatic advertising and the growing adoption of connected TV (CTV).

As more viewers cut the cord and embrace streaming platforms, ad dollars are following suit. The company’s partnerships with major players like Disney (NYSE:DIS), NBCU, and Roku (NASDAQ:ROKU) further solidify its position in the CTV space. Additionally, the increasing adoption of UID 2.0 is helping Trade Desk gain market share from walled gardens like Google and Facebook.

With analysts projecting annual EPS growth of around 25% and sales growth of approximately 20% in the coming years, Trade Desk has the potential to deliver substantial returns for long-term investors. If the stock can maintain its premium valuation, it could very well turn a $50,000 investment into $1 million by 2034.

ServiceNow (NOW)

ServiceNow (NYSE:NOW) provides cloud-based software that helps companies manage digital workflows. The company is riding major tailwinds as enterprises race to automate processes and integrate artificial intelligence (AI) across their operations. In Q1, ServiceNow delivered outstanding results, with subscription revenue growing 24.5%. And, its closely watched current RPO metrics beat guidance.

The company’s Generative AI offerings like NowAssist are already the fastest-selling product in company history.

While the stock trades at a premium 55 times forward earnings multiple, this valuation could stick around if ServiceNow sustains its current momentum. With a rock-solid 98%+ renewal rate and projected 20%+ revenue and EPS growth for years to come, ServiceNow appears well-positioned to do just that.

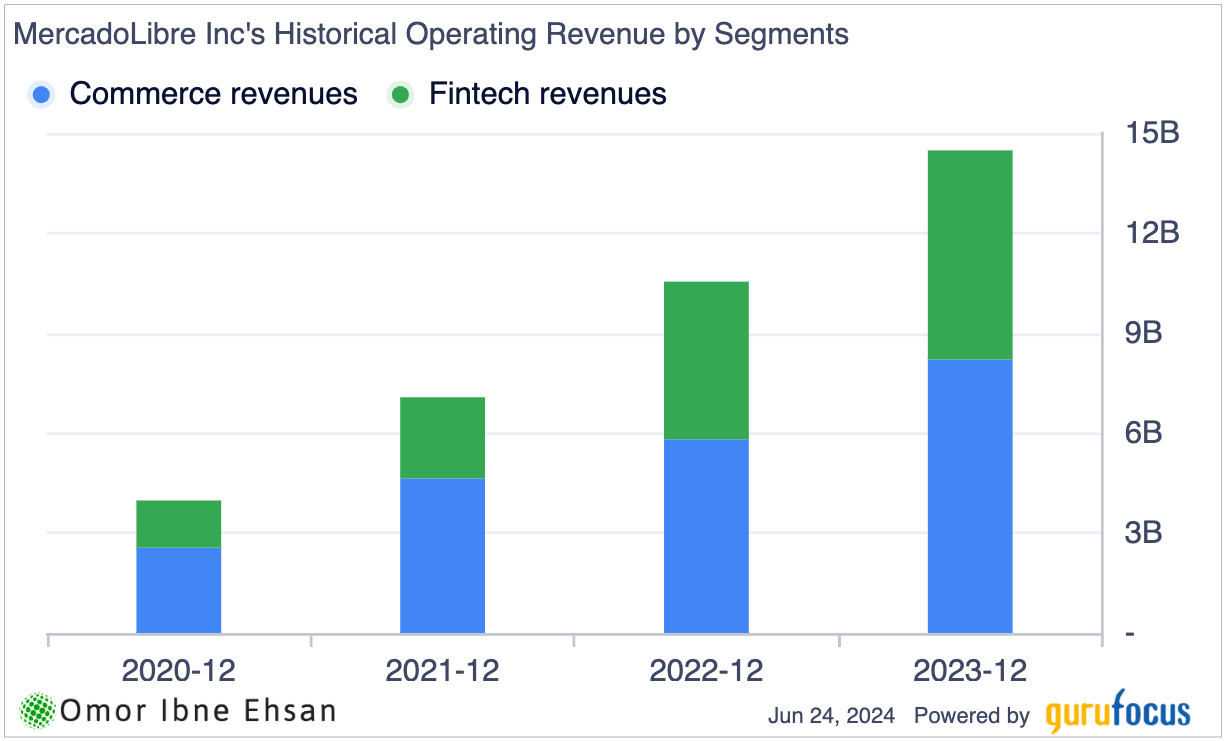

MercadoLibre (MELI)

MercadoLibre (NASDAQ:MELI) operates the leading e-commerce and digital payments platform in Latin America. This company is riding powerful megatrends that could propel the stock much higher over the next decade. MercadoLibre is essentially becoming the Amazon of Latin America. Absolutely, it dominates online retail in a region with a rapidly growing middle class and accelerating internet adoption.

While the fintech segment has hit some speed bumps lately due to macro headwinds like high interest rates and softening consumer demand, MercadoLibre’s core e-commerce business continues to fire on all cylinders with no signs of cracking. For example, Brazil and Mexico posted stellar 30% GMV growth in Q1. Also, the fintech segment has been doing just fine if you zoom out.

Click to Enlarge

Furthermore, despite challenges in Argentina, MercadoLibre still delivered robust top and bottom-line growth in the quarter. Analysts see EPS skyrocketing from $34 in 2024 to $245 by 2033. While a 20x return is a tall order, I wouldn’t be surprised to see MercadoLibre delivering market-crushing gains.

DexCom (DXCM)

DexCom (NASDAQ:DXCM) develops and manufactures continuous glucose monitoring systems for diabetes management. The company is riding several powerful megatrends and tailwinds that could propel its stock to massive gains by 2034.

First and foremost, companies in the diabetes treatment space are seeing their revenues and profits surge. With obesity rates remaining stubbornly high and sedentary lifestyles becoming more prevalent, the unfortunate reality is that diabetes cases will likely continue rising for the foreseeable future. This provides a major tailwind for DexCom.

Also, the company posted stellar growth, with revenue growing 24% year-over-year (YOY) to $921 million. In addition, DexCom handily beat expectations on the bottom line, posting EPS of 32 cents versus the 27 cents consensus estimate.

So, although shares have languished in the near term, DXCM remains a good long-term bet. Plus, its EPS is expected to more than double in the next four years.

Safran (SAFRY)

Safran (OTCMKTS:SAFRY) provides aerospace and defense products and services. The aviation industry has been soaring in recent years, fueled by tax cuts that allowed business jet write-offs. While the pandemic temporarily grounded the sector, it’s now roaring back with a vengeance. I’m not talking about debt-laden airlines, though. I’m referring to the real winners: aviation manufacturing and software giants like Safran.

This French powerhouse is posting stellar results, with Q1 revenue growing 18% to 6.2 billion euros. Double-digit growth across all divisions was driven by a 27% jump in civil aftermarket sales. Despite a soft start to aircraft production, Safran still expects 10-15% growth in LEAP engine deliveries for 2024.

The real kicker? Safran trades at a mere seven times forward earnings with a juicy 1% dividend yield to boot. As air traffic recovers (narrow body at 113% of 2019 levels, wide body at 94%), Safran is perfectly positioned to ride the aviation megatrend to new heights. Analysts see nothing but upside from here.

Click to Enlarge

Meituan (MPNGF)

Meituan (OTCMKTS:MPNGF) operates China’s leading e-commerce platform for services, connecting consumers with local businesses. The company has been among the hardest-hit Chinese stocks in recent years, even with loosening financial policies.

However, Meituan’s latest earnings show signs of a sustained recovery on the horizon. In Q1, revenue surged 75% YOY to 73.3 billion RMB, while adjusted net profit jumped 36.4% to 7.5 billion RMB. User base and merchant base growth accelerated for the fourth straight quarter, both hitting record highs.

In fact, Meituan is well-positioned to capitalize on the megatrend of digitizing local commerce in China. The company is innovating with new models like Branded Satellite Stores and elevating consumer experience with initiatives like Pin Hao Fan. Analysts expect EPS to increase from 46 cents this year to nearly 80 cents in 2025. While multibagger returns by 2034 would require cooperation from the broader Chinese market, Meituan’s stock has already nearly doubled off January lows. If it can sustain high-profit growth, this rebound is just getting started.

Workday (WDAY)

Workday (NASDAQ:WDAY) provides enterprise cloud applications for finance and human resources. This company is well-positioned to benefit from the growing trend of workforce automation, particularly among large enterprises looking to streamline operations.

As more companies embrace digital transformation and seek to optimize their HR and financial processes, demand for Workday’s solutions should remain robust. The company posted 19% subscription revenue growth in Q1.

However, investors must weigh the risks. The rise of AI could be a double-edged sword. While it may drive more companies to adopt Workday’s automation tools, it could also lead to significant headcount reductions that shrink Workday’s addressable market. Additionally, with the stock’s muted performance in recent years, a 20x return by 2034, while not impossible, would require a near-perfect execution. Nevertheless, I still think it is a good candidate since it has strong tailwinds, and analysts expect solid growth going forward.

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.