After suffering years of futility, things may be turning around for FireEye Inc (NASDAQ:FEYE). Year-to-date, FireEye stock has jumped over 32%, well exceeding several analysts’ expectations. Although the year is young, FEYE appears to be delivering on its potential from 2017, when it returned nearly 22%.

Of course, I don’t want to get ahead of myself. This was a company that once flirted with a market value of $100 per share. However, that initial fantasy soon after its initial public offering was a short-lived one. Since then, FEYE has been known more for its disappointments than its successes.

That few believe in FireEye stock isn’t helping matters. Despite the cybersecurity firm’s outperformance this year, covering analysts have only marginally lifted their assessment. Among 29 experts, only 11 view it as a buying opportunity. Virtually everyone else is on the sidelines, with a single person espousing the bearish argument.

For what it’s worth, you can include me among the believers. Two months ago, I reaffirmed my bullishness.

So many companies and institutions, notably Target Corporation (NYSE:TGT), Home Depot Inc (NYSE:HD) and especially Equifax Inc. (NYSE:EFX), suffered serious data breaches. The cybersecurity industry has only one place to go: up. This is great news for FEYE, despite its troubles.

The only major concern I had was nearer term. I spotted what I believed was a bearish head-and-shoulders pattern forming between spring 2017 until February of this year. I’m glad to say I was wrong about that. FireEye stock blasted through key resistance levels and looks quite strong.

I have no reservations now. FEYE is for real. Here are three more reasons why I’m doubling down.

FireEye Enjoys an Incredibly Relevant Industry

Moving forward, perhaps the best industry you can start a business in is internet technology. But if that’s not your cup of tea, an extremely close second is cybersecurity.

All you have to do is open up a newspaper. Every year, major institutions suffer security and data breaches that cost billions in damages and lost productivity. Even more costly is reputation damage; again, just consider the Equifax fiasco.

And obviously, the problem will worsen, but you may not fully appreciate the magnitude. Cybersecurity experts predict that by the year 2021, cybercrime will cost the world $6 trillion in damages annually; that’s double the figure from 2015! To put that into perspective, that’s roughly the annual GDP

of Germany and Great Britain combined.

More significantly, cybercrime exponentially exceeds the number of legitimate IT jobs. Quite literally, no shortage of cybersecurity-related employment opportunities exist. Crime may not pay, but it certainly keeps the unemployment line empty.

The takeaway for FEYE and FireEye stock is simple: competition doesn’t matter. The cybersecurity industry is more than big enough to reward current players, and actually encourages additional participants.

FEYE Has Surprisingly Solid Financials

A major criticism that pops up about FEYE is its financials. FireEye has lost boatloads of money over the past several years. Furthermore, it’s tacked on a significant debt load relative to its cash position.

I admit that the financials leave a lot to be desired. But keep in mind that we have a highly probable story line for FEYE. We shouldn’t overly concern ourselves with where the company currently is; rather, we should focus where the company will be.

This is a lot easier and lot less speculative for a company like FireEye. Again, it needs improvement in key areas, such as in the earnings department.

But negative earnings for FEYE can’t be compared to negative earnings of a brick-and-mortar retailer getting clobbered by Amazon.com, Inc. (NASDAQ:AMZN). So long as FireEye’s keeping the lights on, its industry tailwinds should drive it forward.

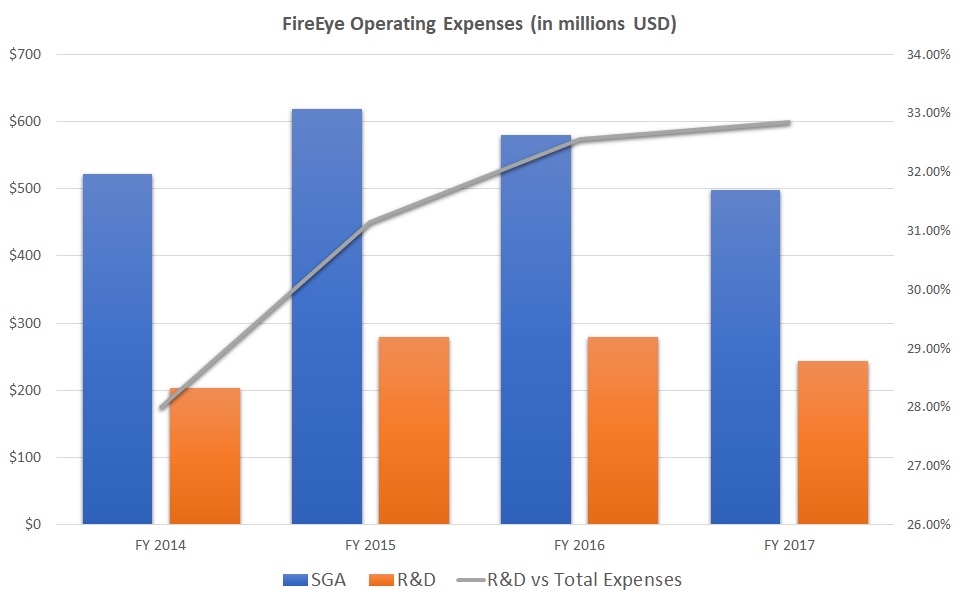

But what I appreciate about this cybersecurity firm is that it’s positioning itself for success. Note that FEYE’s research and development expenses relative to total operating expenses have steadily increased over the past few years. That tells me that while it’s maintaining fiscal discipline, it’s investing in areas that matter most.

Click to Enlarge

Contrarian Opportunity for FireEye Stock

Many investors avoid FEYE stock because among its main competition, it’s one of the more volatile names. Plus, with the commonly cited weaknesses in its current financials, conservative traders go for the sure thing. However, this trend sets up a possible contrarian opportunity.

Take a look at rivals Palo Alto Networks Inc (NYSE:PANW) and Fortinet Inc (NASDAQ:FTNT). Both have experienced a brilliant start to the year, up 31.4% and 31.8%, respectively. Virtually nothing separates these two and FEYE. So why give the edge to FireEye stock?

Quite simply, Palo Alto and Fortinet are examples of strong companies getting stronger. In other words, their growth potential is limited due to the “expectation phenomenon.” If everyone bets on the winning horse, the reward necessarily must be limited due to the reduced risk.

That’s not the case with FEYE. Most folks view it as a speculative gamble. Psychologically, with a share price in the teens (versus the competition), that perception is further solidified. But that’s to FireEye’s, and hopefully your benefit. No one expects it to do much, so if it does, it’s off to the races.

More importantly, I believe the bears are overstating the company’s weaknesses. If you look at the details, FEYE is making the right decisions, and the results are just paying off.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.