Nothing epitomizes the discount warehouse industry quite like Costco Wholesale Corporation (NASDAQ:COST). What Alphabet Inc (NASDAQ:GOOG, NASDAQ:GOOGL) is to the internet, COST is to retail. They’re both also represented in pop culture. Google was heavily featured in the 2013 film, “The Internship.” The Jessica Simpson comedy “Employee of the Month” obviously was lampooning the warehouse giant. But despite similar mainstream appeal, only Costco stock is in danger of being labeled a laggard in 2016.

That conundrum is causing investors on Wall Street to scratch their heads. Late last week, Costco stock delivered unexpectedly for its fourth quarter of fiscal year 2016 earnings report.

Rather than slipping due to its credit card switch to Visa Inc (NYSE:V) from long-term partner American Express Company (NYSE:AXP), COST stock instead posted earnings of $1.77 per share. That was 4 cents above consensus, and more significantly, it proved to naysayers that the company knows what it’s doing. As a result, Costco stock jumped over 3% following earnings.

The Good News for Costco Stock Was Short-lived

Unfortunately, that bit of good news was immediately overshadowed by longer range concerns. Although COST stock has demonstrated strong earnings growth in the past, recent figures places that confidence in doubt.

The benefits awarded to customers through the Visa shift will pressure margins. More importantly, the specter of a membership fee hike looms large for Costco stock. As InvestorPlace contributor Dana Blankenhorn points out, the retailer is highly dependent on those fees.

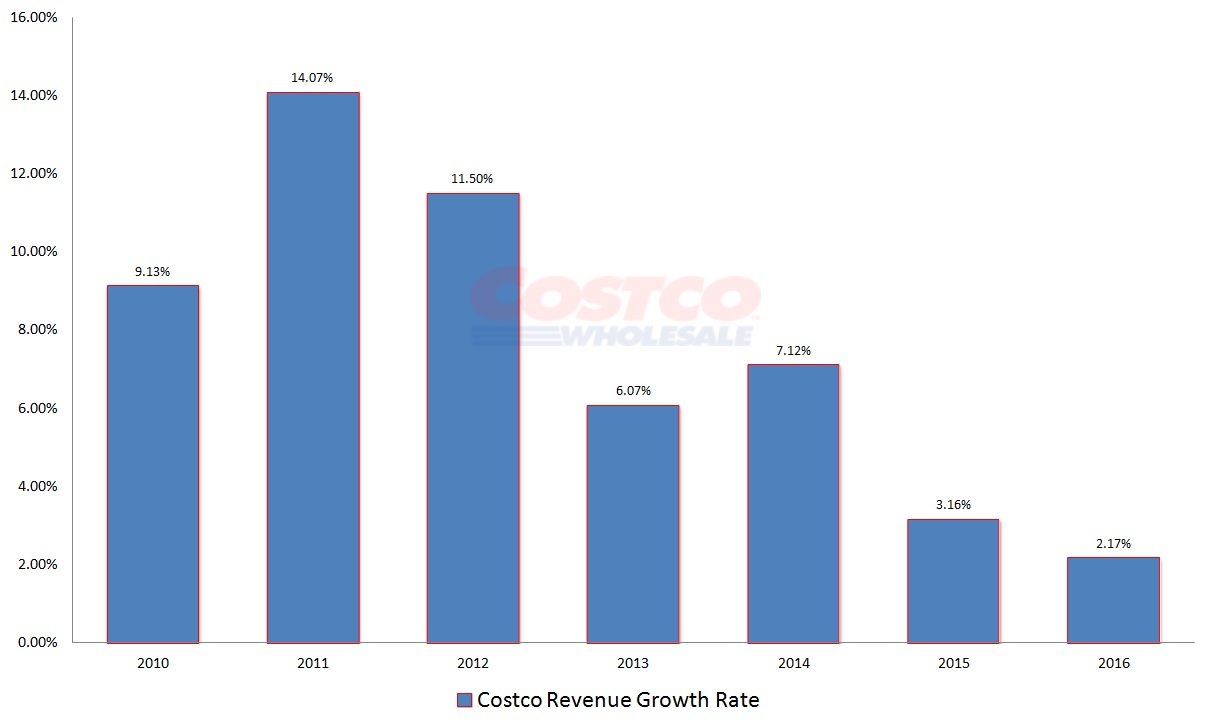

Click to Enlarge

Should membership costs rise, this presents a few substantial problems for COST stock. Number one, the top-line is just as stale as the bottom. With FY 2014 being the sole exception, revenue growth declined consecutively over the past six years. That ties in with the days inventory rate that has been creeping up over the same time frame.

Those figures will only worsen if either membership or sales performance continues to drag. Finally, food price deflation has been a problem for traditional grocers, and will surely pressure Costco stock.

Because COST is also in the “oil business” so to speak, the broader commodity downturn has been a double whammy. But the greater — and more troubling — argument is why commodities are hurting. In short, there’s a demand crunch. Wages are flat. The economic recovery is unbalanced. Hence, fewer dollars are chasing after more goods. Naturally, the dollar should get stronger in this circumstance — and it’s doing just that!

The Many Challenges Facing COST

The issue, then, is that it’s not Costco stock: it’s the economy. But don’t be tempted to view COST as a great buying opportunity like Jim Cramer is saying. COST stock is around 11% below this year’s high. This isn’t exactly a compelling discount. Even if the play was to recover the amount lost, there are safer ways to make low, double-digit returns. I would reiterate that the food industry is in trouble. Therefore, if I’m going to take a fairly hefty risk, I’d like more than a 1% dividend yield.

This is why you should take the “resilience against Amazon.com, Inc. (NASDAQ:AMZN)” argument with a grain of salt. Of course, COST executives will downplay Amazon’s negative impact towards competitiveness. But if the economy is challenged — and deflation of any sort usually means that it is — retail isn’t the best option. Furthermore, the high-volume nature that Costco stock depends upon is particularly sensitive to macro-consumer shifts.

If I was heavily vested in COST stock, I’d especially be worried about Wal-Mart Stores, Inc. (NYSE:WMT). The warehouse doesn’t always have the best deals, either from a price or quality perspective. That provides a stronghold for Wal-Mart to exploit should consumer income not adequately grow. Also, there’s the question of price selection. A family may be in need of ketchup, but ten gallons worth? That’d only fly if you belong to “The Duggars.”

The Bottom Line for Costco Stock

With all things considered, it’s not terribly surprising that Costco stock is down almost 7% year-to-date. Neither is the fact that shares have struggled to build off the positive earnings surprise. The quarterly results were a nice bonus. But the real focus should be on repeated failures by COST stock to secure the $170 level.

Costco is an incredible company that will continue to be a retail giant, good economy or bad. However, the risk is no longer worth the reward. More likely, COST stock will gain a few points, and chug along slowly. Until the fundamental clouds give way, Costco stock just doesn’t generate enough excitement for investors.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.