With the Federal Reserve gearing up for a potential rate-cutting cycle, the economy could see a dramatic transition in the coming months. While a market downturn remains a possibility, many of these beaten-down stocks are unlikely to plummet further from their current depressed levels. These once-in-a-decade stocks seem primed for a swift rebound once rates come down and normalcy returns.

Patience is a virtue in the stock market, and well-established companies rarely disappoint in the long run. I believe the current market turbulence presents an ideal moment to pounce on these once-in-a-decade stocks. After all, the time to be greedy is when others are fearful.

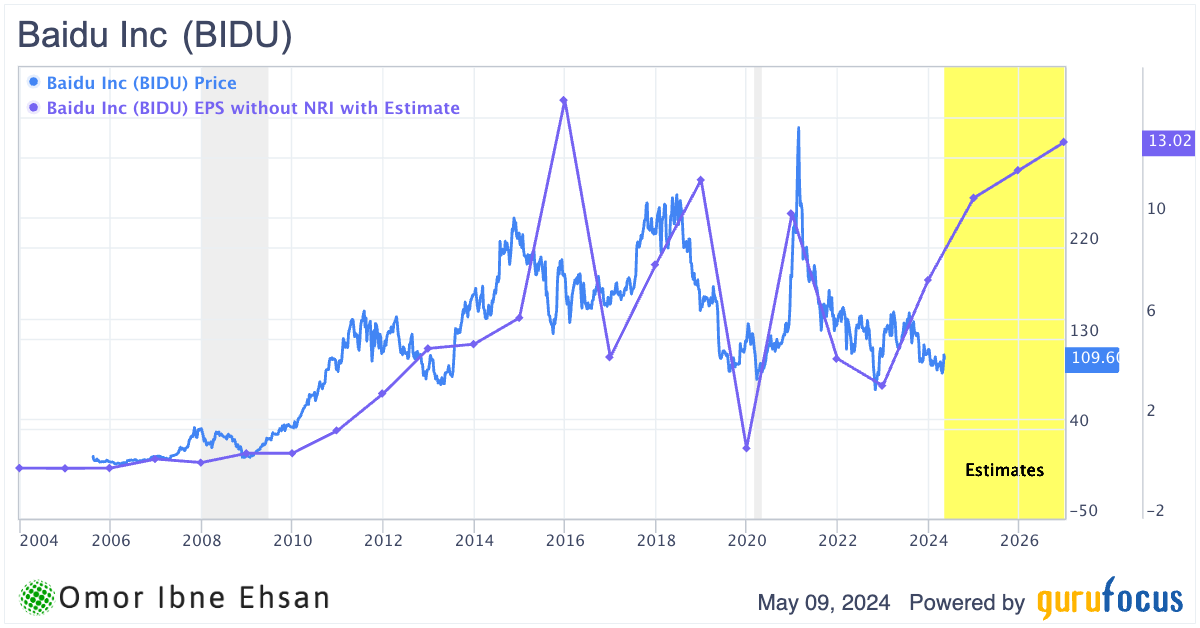

Baidu (BIDU)

Baidu (NASDAQ:BIDU) is known as the Google of China, and for good reason. The company has amassed a massive captive user base on which it can capitalize. Boasting an impressive 60% market share across all platforms in China and an even more dominant 76% share in the mobile user segment, Baidu’s reach is undeniable. Moreover, it is one of the few companies with a working maps feature in China, as foreign tech giants like Google don’t have access to the country’s unique map offset algorithm.

However, my bullish stance on Baidu stock extends far beyond these competitive advantages. With most Chinese tech companies going for a fire sale, there is a compelling opportunity to scoop up potential comeback stocks at bargain prices. Baidu is a powerhouse in cutting-edge technologies. The company’s AI chatbot, Ernie, already has a staggering 200 million users, while Baidu Wangpan, its cloud service offering, mirrors Google’s offerings.

While Baidu’s growth may not be impressive in the short term due to challenges in China’s economy, I do not perceive any long-term weaknesses. Analysts anticipate Baidu’s growth to accelerate in the years ahead, with revenue projected to grow 8% in 2025, 6% in 2026, 15% in 2027, 12% in 2028, and a stellar 42% in 2029. The consensus EPS is forecasted to rise from $11 in 2025 to $25 in 2029. For a tech stock of this caliber, you’re paying just 11 times earnings and two times sales.

Click to Enlarge

That to me looks like one of the best once-in-a-decade stocks to buy.

Newell Brands (NWL)

Newell Brands (NASDAQ:NWL) is not a tech stock like BIDU. Most investors would be bearish on the stock right now due to its disastrous price performance. However, this is precisely what makes it a contender as one of the comeback stocks. NWL stock is up just around 35% from its Great Recession trough levels and is down far below its COVID trough. This is due to the company’s lack of cash flow and high debt levels.

Interestingly, the high debt burden is actually the root cause of the lack of cash flow. To put it in perspective, Newell Brands paid $298 million in cash interest expenses, which was a significant portion of the company’s $930 million operating cash flow for all of 2023. Why am I bullish on this? Rate cuts. Once interest rate cuts kick in full swing, we should see the cash flow turn positive very quickly and then expand. Analysts expect EPS to jump from 60 cents in 2024 to $1.1 in 2028. I believe that Newell Brands can beat these estimates and make a swift comeback from these levels.

Moreover, I think that selling at these levels does not make sense, even for bears. Most of the bearishness is already priced in, so there is a good chance the stock will bounce higher from here.

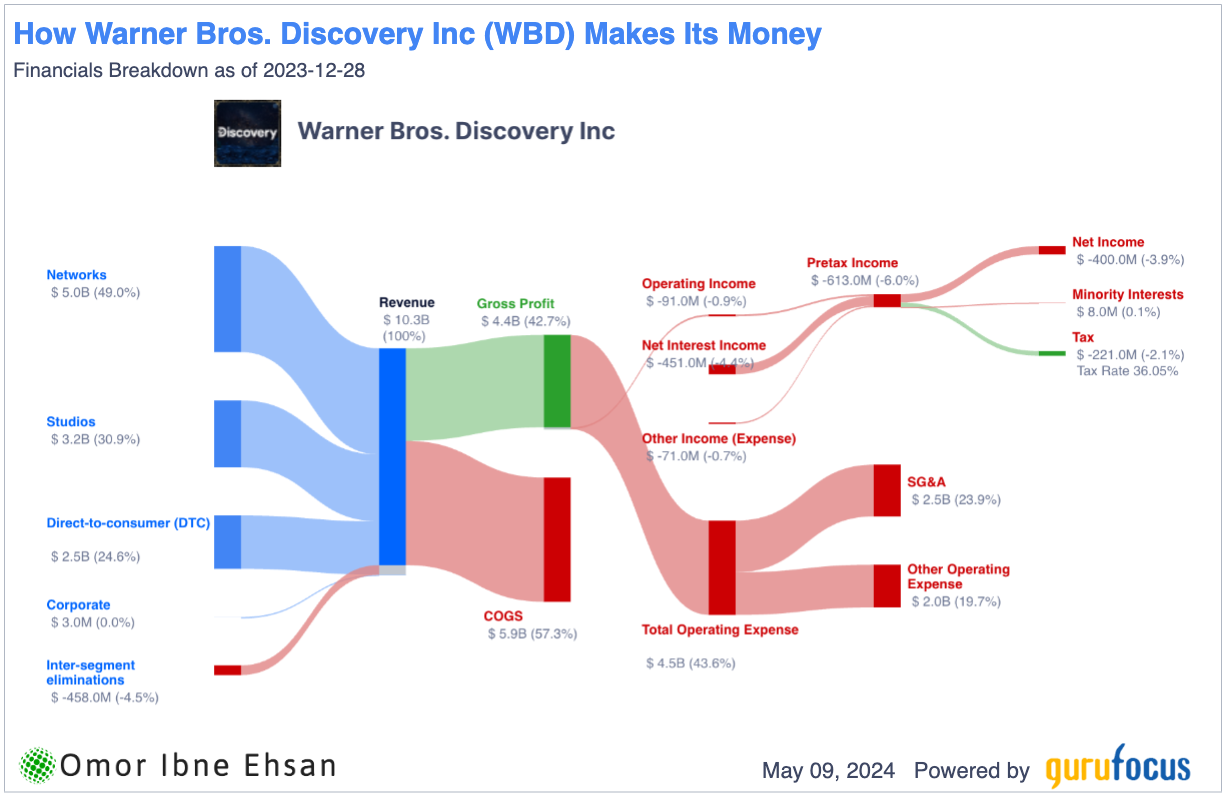

Warner Bros. Discovery (WBD)

Unlike Newell Brands, the situation with Warner Bros Discovery (NASDAQ:WBD) is not so clear-cut. Some companies in the market have become quite politicized in recent years, which can take a toll on the stock regardless of which side you’re on. It’s not just a matter of “go woke, go broke,” as even Tesla, often perceived as leaning more toward the right, has been struggling. Any sort of politicization of a company has very negative consequences. I believe Wall Street would pay a higher premium if buying these stocks wasn’t seen as a statement.

Regardless, I see very good long-term returns from the current price. Warner Bros’ problems are not long-term. Moreover, politicization wouldn’t stop the market from closing a big enough gap between a stock’s price and its fundamentals. While Warner Bros is unlikely to have meaningful top-line growth, even with the company paying down debt, we’re looking at a massive earnings expansion. EPS is expected to be 86 cents in 2028 from negative 27 cents in 2024.

Moreover, Max has a lot of potential in the streaming space and could become one of the top three platforms. Warner Bros had around $2.2 billion in interest expenses last year and net interest income in Q4 alone was -$451 million, so I expect a comeback once rate cuts start.

Click to Enlarge

The company has a plan to pay off its $47.3 billion debt, and I think it will be successful. It had an EBITDA (earnings before interest, taxes, depreciation, and amortization) of $7.4 billion last year. It’s another one of the top once-in-a-decade stocks to buy.

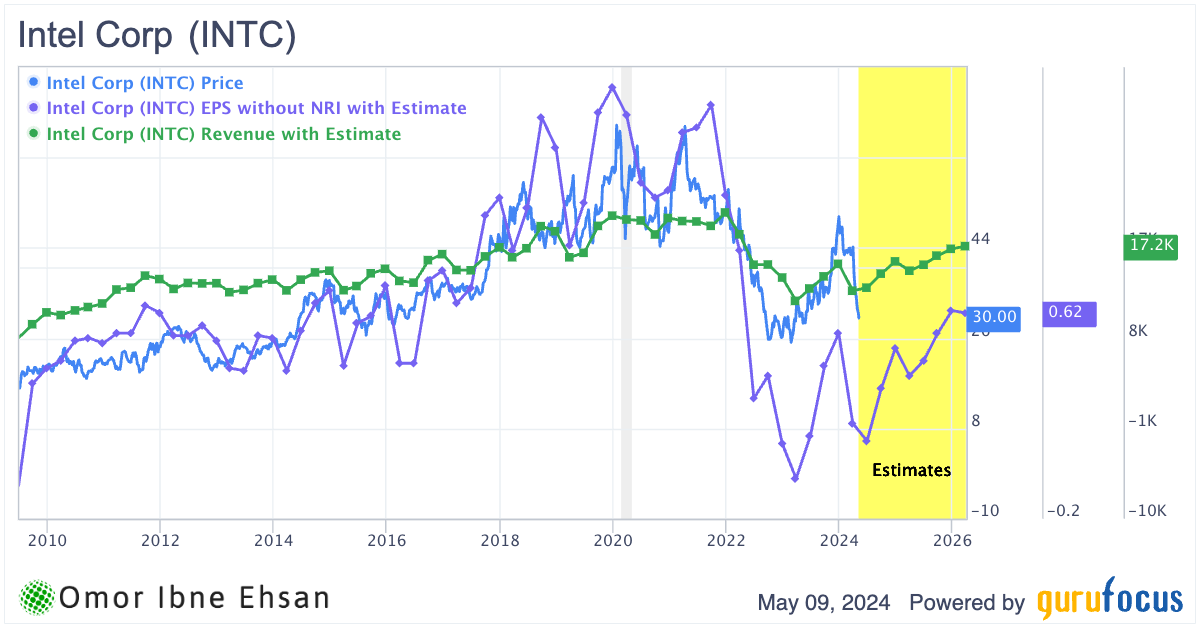

Intel (INTC)

Intel’s (NASDAQ:INTC) rebound has been undone in days, and it will likely take months to recoup the damage. The company’s Q1 earnings beat expectations with $12.7 billion in revenue but still fell short of revenue guidance. The stock is now 37.6% down year-to-date, and looking at the trends makes one feel like they’re back in 2022 again! However, I believe this presents a great buying opportunity since Intel is trading near valuations we’ve seen nearly two years back but with much better fundamentals.

Intel has kickstarted growth again, and it has been narrowing its losses quite fast. The company’s financials will likely reach an inflection point this year. It could then head higher in the coming years with double-digit growth. Intel’s EPS is expected to grow almost 5X in the next four years, along with low double-digit top-line growth on average. You’re paying just 15 times the 2025 estimated EPS for a company that has been acquiring many other high-growth tech names and has been aggressively competing with bigger peers.

Click to Enlarge

While I don’t expect Intel to dethrone AMD (NASDAQ:AMD) or Nvidia (NASDAQ:NVDA) anytime soon, this unfair comparison has caused the market to become too bearish on Intel. In my view, the current selling frenzy has created a compelling entry point for long-term investors.

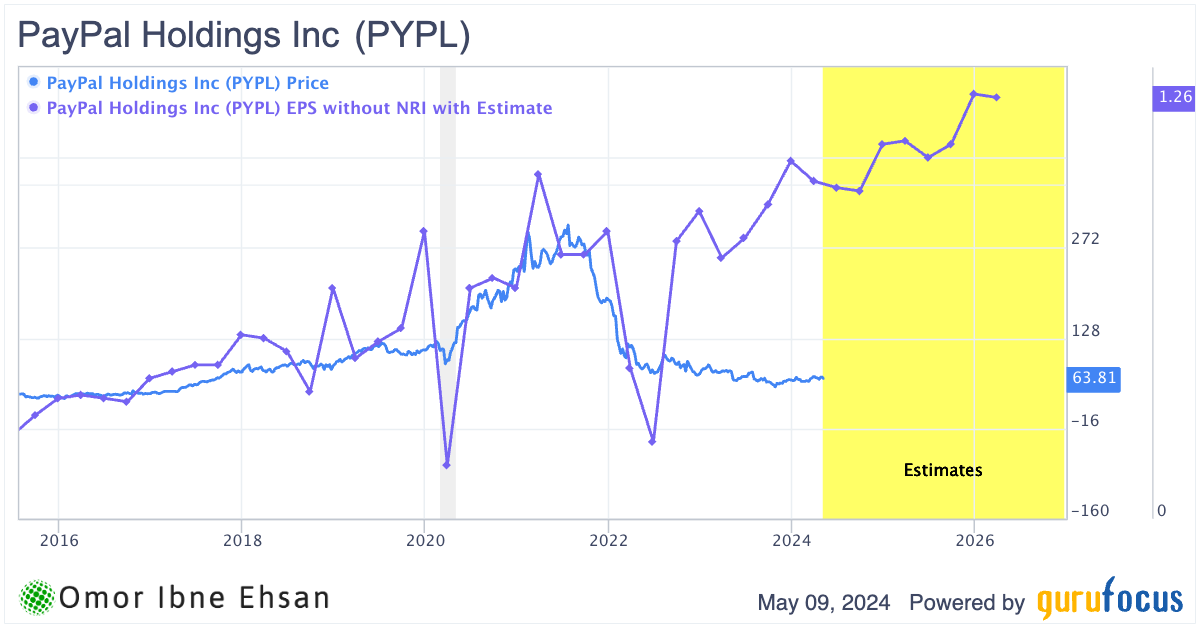

PayPal (PYPL)

Speaking of once-in-a-decade stocks, PayPal (NASDAQ:PYPL) is one of the top candidates. This company has been doing almost everything in its power to be loved by Mr. Market again. Sadly, nothing has worked so far. PayPal has continued to trade essentially sideways since the selloffs and is trading 48% lower than its pre-pandemic prices. That is despite its top and bottom line being much better than before, with growth numbers staying robust.

This has happened because PayPal has had a user accounts growth figure in the negatives for the past few quarters. However, too much weight is being put on this one metric. If you look at the broader picture, PayPal has continued to squeeze out more and more revenue from its existing “power” users. Analysts expect this growth to continue many years into the future.

Click to Enlarge

In fact, active user growth has finally inflected on a quarterly basis. In Q1, active users grew by 2 million, and it could be a sign of more to come.

Starbucks (SBUX)

Starbucks’ (NASDAQ:SBUX) plunge is relatively small compared to many of the stocks in this list, but I think it is one of the once-in-a-decade buying opportunities. The coffee chain failed to meet expectations, with same-store sales falling for the first time since 2020.

CEO Laxman Narasimhan attributed the poor quarterly performance to customers being more cautious about their spending due to inflation. He also noted that the recent quarterly results did not reflect the potential of the brand. Long wait times and product availability also seem to be putting customers off, with over 60% of the company’s morning trade coming from reward members who use the Starbucks app.

To put the miss in perspective, EPS missed estimates by 15.2%, and revenue missed by a staggering 6.5%, with revenue declining by 1.8% YOY. Despite these misses, I’m still confident Starbucks can bounce back. Rate cuts could take a lot of the pressure off earnings in the coming quarters. Plus, EPS growth of around 15% annually is expected starting next year. In my view, a lot of the bearishness is priced in right now, and I do not think this is a long-term laggard.

Alibaba (BABA)

This stock is definitely a long-term laggard. Most Chinese stocks are at a huge discount right now, including Alibaba (NYSE:BABA). However, the Chinese market has finally started to recover meaningfully, and these tailwinds will likely lift China’s tech sector up as well.

The growth ahead isn’t stellar, but Alibaba could outperform once China’s economy restarts growth with fresh stimulus and rate cuts from the CCP. Moreover, analysts remain optimistic about Alibaba’s stock. J.P. Morgan set a price target of $105. I believe current prices would be nothing short of a bargain ten years from now. Definitely one of the best once-in-a-decade buying opportunities.

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.